Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Breaking News

It has been about a month since the last earnings report for Hill-Rom Holdings, Inc. (NYSE:HRC) . Shares have lost about 7.6% in that time frame, underperforming the market.

Will the recent negative trend continue leading up to its next earnings release, or is HRC due for a breakout? Before we dive into how investors and analysts have reacted as of late, let's take a quick look at its most recent earnings report in order to get a better handle on the important drivers.

Recent Earnings

Hill-Rom Holdings reported first-quarter fiscal 2018 adjusted earnings per share (EPS) of 92 cents, reflecting a 21.7% increase from the year-ago quarter. Adjusted earnings surpassed the Zacks Consensus Estimate by 15% and were well above the company’s projected range of 77-79 cents.

The strong bottom-line performance was backed by solid core revenue growth, continued margin expansion, strategic investments to drive growth and a 6-cent benefit related to U.S. tax reform. This marked the 10th consecutive quarter of double-digit earnings growth for the company.

Revenue Details

Revenues in the first quarter increased 4.6% year over year to $669.7 million (up 3% at CER). The top line also exceeded the Zacks Consensus Estimate of $659 million on momentum in core business, Mortara acquisition and value added from new products.

Geographically, U.S. revenues grew 2% to $453 million while revenues outside the United States increased 13% (up 7% at CER) to $217 million. Core revenue growth was 2% at CER.

Segmental Performance

In the first quarter, Patient Support Systems revenues dropped 0.2% year over year (down 1.9% at CER) to $334.4 million. The segment’s domestic revenues declined 2%. However, after adjusting for divestitures, U.S. core revenues increased nominally from the prior year.

Revenues at the Front Line Care segment, which includes Welch Allyn, Respiratory Care and Mortara, increased 11.3% to $224.6 million (up 9.8% at CER). Apart from gains from Mortara, the performance was driven by contributions from new products, strong growth of thermometry and blood pressure monitoring devices plus double-digit growth at respiratory care business.

The Surgical Solutions segment revenues increased 10.3% (up 5.8% at CER) to $110.7 million on 10% international growth, driven by strong momentum in the Middle East and Europe. U.S. revenues increased 2% despite the negative hurricane impact. The growth was backed by record placement of Integrated Table Motion and contribution from products like the iLED7 and the new TS 3000 Mobile Operating Table.

Margins

Reported gross margin in the fiscal first quarter was 47.7%, up 20 bps year over year. Despite 4.6% increase in cost of revenue, the company witnessed gross margin expansion on account of a 4.6% increase in revenues. Adjusted gross margin grew 20 bps to 47.7% on the back of the company’s consistent initiative with portfolio diversification, benefits from cost and sourcing efficiencies, product launches and gains from Mortara. Adjusted operating margin improved 10 bps to 14.7%.

Outlook

In view of a promising first quarter performance, Hill-Rom has raised its fiscal 2018 guidance and has also provided the second quarter estimates.

For the full year, the company continues to expect revenue growth of 3-4% on a reported basis (up 2% to 3% at CER). Excluding foreign currency, Mortara, divestitures and other non-strategic assets, the company continues to expect core revenue growth of 3%. Hill-Rom expects adjusted earnings per share in the range of $4.57-$4.65. The Zacks Consensus Estimate for fiscal 2018 earnings is pegged at $4.38 on revenues of $2.84 billion.

For the second quarter, Hill-Rom expects revenue growth of around 4% on a reported basis (or approximately 2% at CER). Core revenues are expected to increase 2% year over year. The company expects adjusted earnings per share of $1-$1.02. The Zacks Consensus Estimate for second-quarter earnings stands at $1 on revenues of $704.1 million.

How Have Estimates Been Moving Since Then?

It turns out, fresh estimates flatlined during the past month. There has been one revision higher for the current quarter compared to one lower.

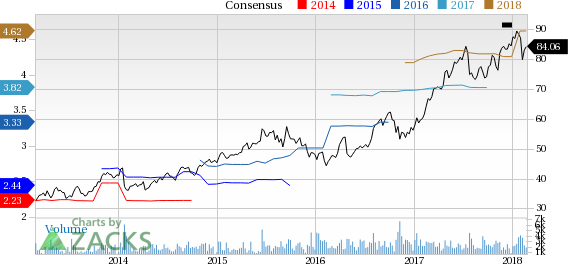

Hill-Rom Holdings, Inc. Price and Consensus

Hill-Rom Holdings, Inc. Price and Consensus | Hill-Rom Holdings, Inc. Quote

VGM Scores

At this time, HRC has a nice Growth Score of B, though it is lagging a bit on the momentum front with a C. However, the stock was allocated a grade of B on the value side, putting it in the second quintile for this investment strategy.

Overall, the stock has an aggregate VGM Score of B. If you aren't focused on one strategy, this score is the one you should be interested in.

Zacks' style scores indicate that the company's stock is more suitable for value and growth investors than momentum investors.

Outlook

HRC has a Zacks Rank #2 (Buy). We expect an above average return from the stock in the next few months.

Palantir remains highly valued with a 460x P/E ratio and a 42.5x P/B ratio, far above its peers. The stock's beta of 2.81 signals high volatility, meaning sharp moves in both...

The S&P 500 had started to clear resistance, posting new all-time highs before sellers struck with a vengeance. The selling was bad, similar to that seen in December, which...

Myself and others have highlighted how European Equities have been breaking out to new all-time highs on the back of bullish factors such as cheap valuations, monetary tailwinds,...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.