Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

A successful investor understands the importance of retaining well-performing stocks in the portfolio at the right time. Indicators of a stock’s bullish run include a rise in share price and strong fundamentals. Though there may be some concerns regarding the stock but they are all short-lived.

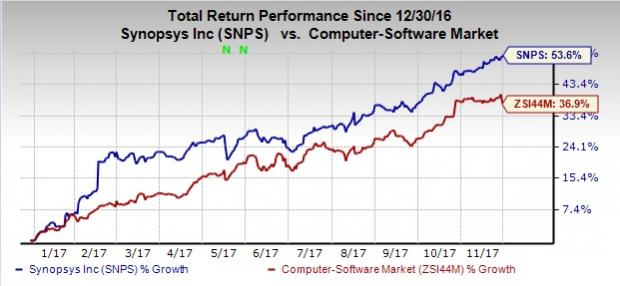

Synopsys Inc. (NASDAQ:SNPS) is one such technology stock that has been on healthy growth trajectory, of late. It has rallied 53.6% year to date, outperforming 36.9% growth recorded by the industry it belongs to.

Let’s now delve deeper and take a look at some of the aspects aiding the company’s performance.

Upbeat Q4 Reults

Continuing its earnings streak for the seventh consecutive quarter, Synopsys, delivered stellar fourth-quarter fiscal 2017 results, wherein the top and bottom line both came ahead of the respective Zacks Consensus Estimate. The results also marked year-over-year improvement.

The company reported non-GAAP earnings per share of 69 cents, which came in 10.4% higher than the year-ago quarter’s adjusted earnings of 77 cents. The Zacks Consensus Estimate for the quarter is pegged at 57 cents.

The company’s fourth-quarter revenues jumped 9.9% year over year to $696.6 million and came ahead of the previously guided range of $642-$657 million. Reported revenues also surpassed the Zacks Consensus Estimate of $653 million.

On a year-over-year basis, revenues were positively impacted by higher adoption of Synopsys’ products, along with strength in IP and hardware products. Notably, per the company “Our three-year backlog grew approximately $150 million to $3.7 billion, reflecting very good business growth and the timing of large contract renewals.”

Encouraging Guidance

The company initiated positive guidance for the fiscal first quarter. The company expects revenues in the range of $740-$765 million (mid-point $752.5 million). The Zacks Consensus Estimate for revenues was pegged at $669.1 million. Management expects non-GAAP earnings per share in the range of 98 cents and $1.02 per share. The Zacks Consensus Estimate is pegged at 85 cents.

Positive Earnings Surprise History

Synopsys has an impressive earnings surprise history. The company outpaced the Zacks Consensus Estimate in three of the trailing four quarters, recording a positive average earnings surprise of 10.9%.

Further, it has a long-term expected EPS growth rate of 9.1%.

Valuation

Moreover, from a valuation perspective, the stock looks very attractive as it currently trades significantly lower than the industry average based on a forward earnings estimate, which signifies a huge upward potential. Synopsys currently trades at a forward P/E of 24.18x as against the industry group average of 56.00x

Other Growth Drivers

Synopsys recently announced the acquisition of Black Duck Software, a leader in automated solutions for securing and managing open source software. The addition of Black Duck's Software Composition Analysis solution will enhance Synopsys' product offering and will expand customer reach consequently boosting the top line.

The company is a vendor of electronic design automation (“EDA”) software to the semiconductor and electronics industries. We believe the company’s recent product launches, acquisitions and deal wins will boost results, going ahead. Furthermore, unique intellectual properties and global support provided by the company are likely to drive near-term performance. Additionally, the acquisition of Cigital and Codiscope will enable it to offer a comprehensive software security signoff solution to customers.

Risk Remains

However, competition from Cadence Design Systems Inc. and Mentor Graphics Corp., a challenging technology spending environment and uncertainty regarding the exact time of realizing acquisition synergies keep us on the sidelines.

Other Key Picks

Currently, Synopsys carries a Zacks Rank #3 (Hold)

Few better-ranked stocks in the broader technology space are NVIDIA Corporation (NASDAQ:NVDA) , Intel Corporation (NASDAQ:INTC) and DXC Technology Company. (NYSE:DXC) , each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term expected EPS growth rates for NVIDIA, Intel and DXC are 11.2%, 8.4% and 10.5%, respectively.

5 Medical Stocks to Buy Now

Zacks names 5 companies poised to ride a medical breakthrough that is targeting cures for leukemia, AIDS, muscular dystrophy, hemophilia, and other conditions.

New products in this field are already generating substantial revenue and even more wondrous treatments are in the pipeline. Early investors could realize exceptional profits.

Click here to see the 5 stocks >>

The fortune of Nvidia (NASDAQ:NVDA) is closely tied to Big Tech hyperscalers. Although the AI/GPU designer didn’t name its largest clients in the latest 10-K filing on Wednesday,...

Home improvement retailers Lowe’s (NYSE:LOW) and Home Depot (NYSE:HD) turned a corner, and their Q4 2024 earnings reports confirmed it. The corner is a return to comparable store...

One of our old flames, a former Contrarian Income Portfolio holding, has pulled back sharply in recent weeks. Time to buy the dip in this 4.3% dividend? Let’s discuss. Kinder...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.