The J.M. Smucker Company (NYSE:SJM) , a leading manufacturer of food products, posted fourth-quarter fiscal 2017 results wherein both earnings and revenues beat estimates. Notably, the company posted negative surprises in the past three straight quarters.

Adjusted earnings for the fourth quarter came in at $1.80 per share, which were way ahead of the Zacks Consensus Estimate of $1.73 by 4%. Earnings however fell 19% year over year due to lower revenues and decline in gross profits.

Revenue and Margin Details

Net sales in the quarter declined 1% year over year to $1.784 billion. The fall was due to lower net price realization mostly in the U.S. Retail Pet Foods segment and unfavorable volume/mix in the U.S. Retail Coffee segment, partially offset by higher net pricing on coffee and fruit spreads. Net sales however beat the Zacks Consensus Estimate of $1.775 billion by 5.1%.

Adjusted gross profit dropped 2% due to lower volume/mix, while adjusted operating profit increased 2% driven by lower selling, distribution, and administrative expenses.

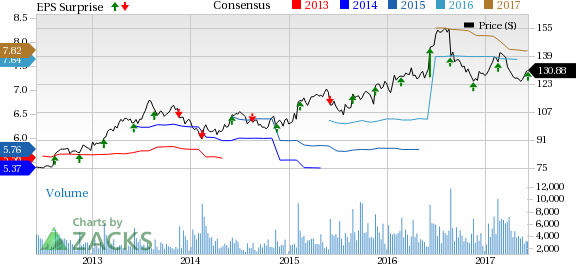

The weakness in sales and earnings is well reflected in the company’s share price movement. Smucker’s shares have decreased 6.4% in the past three months, underperforming the Zacks categorized Food–Miscellaneous/Diversified industry’s 2.1% growth.

Segment Performance

U.S. Retail Coffee Market: The company's biggest segment, U.S. Retail Coffee Market, reported a 1% decline in sales to $505.9 million. This was primarily due to 5% lower volume/mix driven by lower volume for the Folgers brand, partially offset by gains for the Dunkin' Donuts and Café Bustelo brands. The lower volume/mix was mostly offset by higher net price realization.

Segment profit declined 14% to $149.9 million, due to the negative impact of volume/mix, lower net pricing, increased marketing expense and higher commodity costs.

U.S. Retail Consumer Foods: This segment’s sales were almost in line with the prior-year quarter. Higher net price realization, driven by the Smucker's and Jif brands, was offset by lower volume/mix, primarily attributed to the Crisco and truRoots brands.

Segment profit grew 19% to $108.7 million, reflecting higher net pricing and lower manufacturing overhead costs, as well as incremental synergy realization. These factors were partially offset by an increase in marketing expense.

U.S. Retail Pet Foods: Segment net sales were $534.5 million in the quarter, which represented a 5% year-over-year decline, due to lower net price realization. Volume/mix also reduced net sales by 1% as gains for the Nature's Recipe and Milk-Bone brands were more than offset by declines across the rest of the portfolio, most notably 9Lives and Meow Mix cat food.

Segment profit declined 15% to $48.4 million due to decline in sales and increased distribution expense, partially offset by lower input costs.

International and Foodservice: Net sales in the International and Foodservice segment increased 4% from the prior-year quarter to $269.6 million, as lower net price realization and currency headwinds was somewhat offset by favorable volume/mix. Segment profit also grew 26% to $48.4 million driven by favorable volume/mix.

J.M. Smucker Company (The) Price, Consensus and EPS Surprise

J.M. Smucker Company (The) Price, Consensus and EPS Surprise | J.M. Smucker Company (The) Quote

Fiscal 2017 Results

In fiscal 2017, adjusted earnings came in at $7.72 per share, which were way ahead of the Zacks Consensus Estimate of $7.63 by 1.2%. Earnings also exceeded management’s expectations of $7.60−$7.70 per share. Earnings however declined 0.9% year over year.

Net sales, excluding currency and divestiture of U.S. canned milk business, declined 3% year over year to $7.396 billion in fiscal 2017. The decline was in line with the management’s guidance. Net sales however beat the Zacks Consensus Estimate of $7.379 billion by 0.2%.

Financials

J.M. Smucker ended the quarter with cash and cash equivalents of $166.8 million, long-term debt of $4.45 billion and total shareholders’ equity of $6.85 billion.

Fiscal 2018 Outlook

J.M. Smucker envisions fiscal 2018 earnings in the range of $7.85−$8.05 per share, compared with $7.72 per share in fiscal 2017. Further, management expects net sales to increase 1% from the prior year driven by higher net price realization.

Management expects capital expenditure of about $310 million in the fiscal year, wherein it anticipates generating free cash flow of about $775 million.

The company also raised its cost savings target by $100 million, which will result in total annual cost reductions of $450 million for its synergy and cost management programs, when fully realized by fiscal 2020.

Zacks Rank & Key Picks

J.M. Smucker currently carries a Zacks Rank #3 (Hold).

Investors interested in food stocks in the industry include SunOpta, Inc. (NASDAQ:STKL) , Aramark (NYSE:ARMK) and McCormick & Co., Inc. (NYSE:MKC) .

SunOpta has long-term earnings growth rate of 15.00% and sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Aramark and McCormick, both carrying a Zacks Rank #2 (Buy), have growth rates of 12.80% and 8.83%, respectively.

3 Top Picks to Ride the Hottest Tech Trend

Zacks just released a Special Report to guide you through a space that has already begun to transform our entire economy...

Last year, it was generating $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce ""the world's first trillionaires,"" but that should still leave plenty of money for those who make the right trades early. Download Report with 3 Top Tech Stocks >>

J.M. Smucker Company (The) (SJM): Free Stock Analysis Report

SunOpta, Inc. (STKL): Free Stock Analysis Report

McCormick & Company, Incorporated (MKC): Free Stock Analysis Report

Aramark (ARMK): Free Stock Analysis Report

Original post

Zacks Investment Research