Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

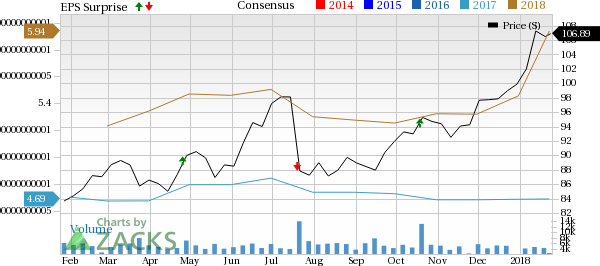

Driven by top-line strength, Northern Trust Corporation’s (NASDAQ:NTRS) fourth-quarter 2017 adjusted earnings per share of $1.51 compared favorably with $1.11 recorded in the year-ago quarter. Results include tax benefits and other one-time items. The Zacks Consensus Estimate was $1.30.

Higher revenues and credit provisions were positives. In addition, the quarter witnessed a rise in assets under custody, as well as assets under management. Moreover, credit metrics marked a significant improvement. However, escalating operating expenses remained a major drag.

Net income came in at $356.6 million compared with $266.5 million recorded in the prior-year quarter.

For full-year 2017, net income was $1.2 billion or $4.92 per share compared with $1.03 billion or $4.32 per share in the previous year. The Zacks Consensus Estimate was $4.69.

Margins & Revenues Improve, Costs Escalate

For full-year 2017, revenues on a fully taxable equivalent basis, were $5.42 billion, up 9% from $4.99 billion in 2016. Additionally, the figure surpassed the Zacks Consensus Estimate of $5.38 billion.

Total revenues of $1.44 billion surpassed the Zacks Consensus Estimate of $1.41 billion. Results also improved 16% year over year.

On a fully-taxable equivalent basis, net interest income of $396 million was up 20% year over year. This was driven by elevated levels of average earning assets and higher net interest margin.

Net interest margin (NIM) was 1.39%, up 19 basis points from the prior-year quarter. The increase chiefly reflected higher short-term interest rates and reduced premium amortization. The positives were partially mitigated by an unfavorable balance-sheet mix shift.

Non-interest income advanced 14% from the year-ago quarter to $1.04 billion. Rise in trust, investment and other servicing fees, along with foreign exchange trading income, other operating income, security commissions and trading income, were the primary reasons for this upswing. These were partially offset by lower treasury management fees and investment security losses.

Non-interest expenses flared up 15% year over year to $1 billion in the quarter. The rise was mainly driven by an elevation in mostly all components of expenses.

Improvement in Assets Under Management and Custody

As of Dec 31, 2017, Northern Trust’s total assets under custody increased 20% year over year to $8.08 trillion, while total assets under management rose 23% to $1.16 trillion.

Credit Quality Improved

Total allowance for credit losses came in at $153.8 million, down 20% year over year. Net charge-offs were $6.6 million, down 39% from the year-ago quarter figure. Also, credit provision was $13 million in the quarter compared with $22 million reported in the prior-year quarter.

Further, non-performing assets decreased 6.1% year over year to $155.3 million as of Dec 31, 2017.

Strong Capital Position

Under the Advanced Approach, as of Dec 31, 2017, Tier 1 capital ratio, total capital ratio and Tier 1 leverage ratio came in at 14.8%, 16.7% and 7.8% compared with 13.7%, 15.1% and 8%, respectively, in the prior-year quarter. All ratios exceeded the regulatory requirements.

Capital Deployment Update

During 2017, Northern Trust repurchased 5.8 million shares for $523.1 million at an average price of $90.25 per share. Notably, during the reported quarter, the company repurchased 1.81 million shares for $170.6 million at an average price of $94.11 per share. This includes shares related to share-based compensation.

Our Viewpoint

Results of Northern Trust display a decent performance in the reported quarter. We remain optimistic by the continued growth in assets under custody, revenues and an improving credit quality, to some extent. Furthermore, positive impact of rising rates was visible. Though escalating expenses might pose a threat to the company’s profitability, benefits of tax reform are anticipated to act as a tailwind.

Northern Trust Corporation Price, Consensus and EPS Surprise | Northern Trust Corporation Quote

Currently, Northern Trust carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Performance of Other Major Banks

Driven by top-line strength, Regions Financial Corporation (NYSE:RF) recorded an impressive earnings surprise of 3.8% in fourth-quarter 2017. Reported earnings of 27 cents per share outpaced the Zacks Consensus Estimate of 26 cents. Moreover, results compared favorably with the prior-year quarter’s earnings of 23 cents. Results included certain one-time items of 7 cents per share.

Riding on higher revenues, PNC Financial (NYSE:PNC) reported a positive earnings surprise of 4.1% in fourth-quarter 2017. Adjusted earnings per share of $2.29 beat the Zacks Consensus Estimate of $2.20. Moreover, the bottom line reflected a 16.2% increase from the prior-year quarter.

Comerica Inc. (NYSE:CMA) pulled off a positive earnings surprise of 5.8% in the fourth quarter. Adjusted earnings per share of $1.28 surpassed the Zacks Consensus Estimate of $1.21. Also, the bottom line compares favorably with the prior-year quarter figure of 99 cents. Results reflected an increase in revenues supported by easing margin pressure and higher fee income. Strong capital position and improving credit quality were the positives. Nevertheless, higher expenses and fall in loans balance remained major headwinds.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaires," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Palantir remains highly valued with a 460x P/E ratio and a 42.5x P/B ratio, far above its peers. The stock's beta of 2.81 signals high volatility, meaning sharp moves in both...

The S&P 500 had started to clear resistance, posting new all-time highs before sellers struck with a vengeance. The selling was bad, similar to that seen in December, which...

Myself and others have highlighted how European Equities have been breaking out to new all-time highs on the back of bullish factors such as cheap valuations, monetary tailwinds,...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.