Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Democrats are not slowing down. The social spending bill follows the infrastructure package. Will gold benefit? Or, will it get into deep water?

Will the American spending spree ever end?

On Monday last week (Nov. 15), President Joe Biden signed a $1-trillion infrastructure package, and just a few days later, his social spending bill worth another $1.75 trillion passed the U.S. House of Representatives. Apparently, $1 trillion was not enough! Apparently, we don’t already have too much money chasing too few goods. No, the economy needs even more money!

Yes, I can almost hear the lament of American families: “We need more money, we already bought everything possible, we already own three cars and a lot of other useless crap, but we need more! Please, the almighty government, give us some bucks, let your funds revive our land.” Luckily, the gracious Uncle Sam listened to the prayers of its poor citizens.

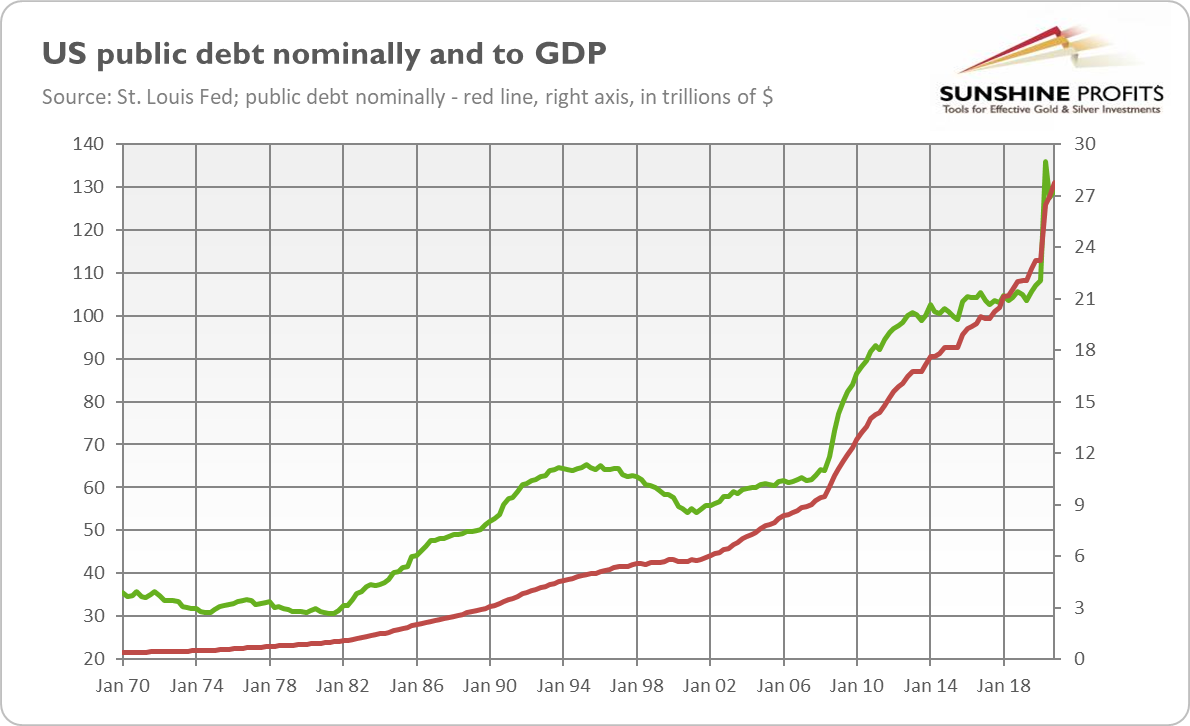

Given the above, one could think that the U.S. economy is not already heavily indebted. Well, it’s the exact opposite. As the chart below shows, the American public debt is more than $27 trillion and 125% of GDP, but who cares except for a few boring economists?

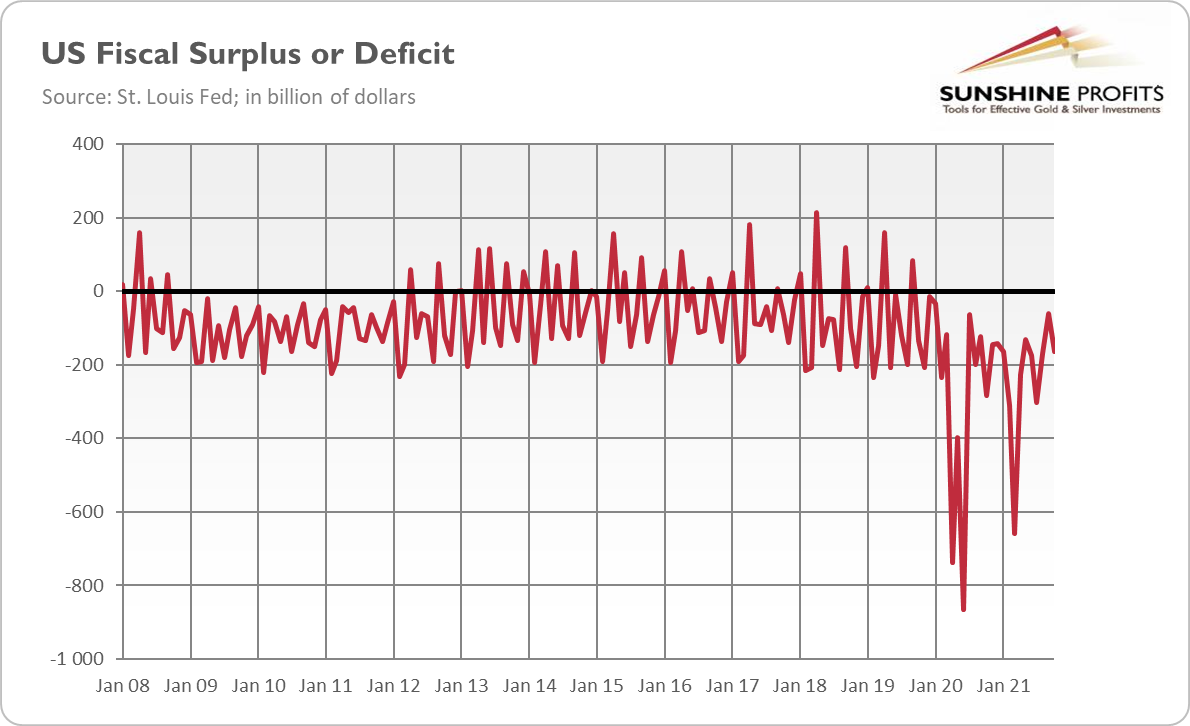

Of course, neither the infrastructure nor the spending bill will increase the fiscal deficits and overall indebtedness to a similar extent as the pandemic spending packages. These funds will be spread over years. Additionally, the fiscal deficit should narrow in FY 2022 as pandemic relief spending phases out (this is already happening, as the chart below shows), while the economic recovery combined with inflation tax bracket creep increases tax revenues.

However, both of Biden’s bills will increase indebtedness, lowering the financial resilience of the U.S. economy. What’s more, the overall debt is much larger than the public debt I focused on here. Other categories of debt are also rising. For instance, total household debt has jumped 6.2% in the third quarter of 2021 year-over-year, to a new record of $15.2 trillion.

What does the fiscal offensive imply for the precious metal market?

In the short run, not much. Fiscal hawks like me will complain, but gold is a tough metal that does not cry. Both of Biden’s pieces of legislation have been widely accepted, so their impact has already been incorporated into prices. Actually, the actual bills could be even seen as conservative – compared with Biden’s initial radical proposals.

In the long run, fiscal exuberance should be supportive of gold prices. The ever-rising public debt should zombify the economy and erode the confidence in the U.S. dollar, which could benefit the yellow metal. However, the empire collapses slowly, and there is still a long way before people cease to choose the greenback as their most beloved currency (there is simply no alternative!).

So, it seems that, in the foreseeable future, gold’s path will still be dependent mainly on inflation worries and expectations of the Fed’s action. Most recently, gold prices have stabilized somewhat after the recent rally, as the chart below shows.

Normal profit-taking took place, but gold found itself under pressure also because of the hawkish speech by Fed Governor Christopher Waller. He described inflation as a heavy snowfall that would stay on the ground for a while, rather than a one-inch dusting:

Consider a snowfall, which we know will eventually melt. Snow is a transitory shock. If the snowfall is one inch and is expected to melt away the next day, it may be optimal to do nothing and wait for it to melt. But if the snowfall is 6 to 12 inches and expected to be on the ground for a week, you may want to act sooner and shovel the sidewalks and plow the streets. To me, the inflation data are starting to look a lot more like a big snowfall that will stay on the ground for a while, and that development is affecting my expectations of the level of monetary accommodation that is needed going forward.

So, brace yourselves, a janitor is coming with a big shovel to clean the snow! Just imagine Powell with a long-eared cap, gloves and galoshes giving a press conference! At least the central bankers would finally do something productive! Or, maybe shoveling is not coming! Although the Fed may turn a bit more hawkish if inflation stays with us for longer than expected previously, it should remain behind the curve, while the real interest rates should stay ultra-low. The December FOMC meeting will provide us with more clues, so stay tuned.

The silver market is forecast to record a fifth straight market deficit in 2025, with demand once again outstripping supply, and the majority of the existing above ground silver...

Trumping Brent Oil Futures. Oil got Trumped and dumped. While many people feared that President Trump aggressive trade negotiations would raise the price of oil, so far oil has...

Upon analysis of the wobbly moves since Tuesday, when the natural gas futures tested the two-year high at $4.55, Thursday might be a cozy one, as the inventory announcements after...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.