Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Affiliated Managers Group Inc. (NYSE:AMG) is scheduled to report fourth-quarter and 2017 results before the opening bell on Jan 29. Its quarterly earnings and revenues are projected to grow year over year.

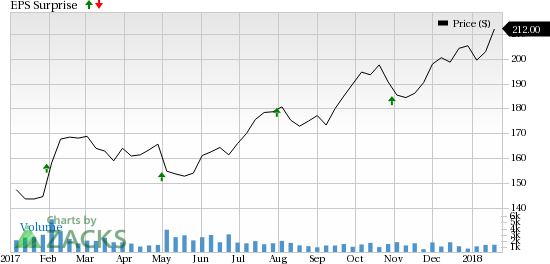

Last quarter, the company’s earnings outpaced the Zacks Consensus Estimate driven by higher revenues and a slight fall in expenses. Also, assets under management (AUM) growth remained strong.

Moreover, the company boasts an impressive earning surprise history. Its earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average beat being 2.1%.

Affiliated Managers Group, Inc. Price and EPS Surprise

Affiliated Managers Group, Inc. Price and EPS Surprise | Affiliated Managers Group, Inc. Quote

Also, activities of the company in the third quarter encouraged analysts to revise estimates upward. As a result, the Zacks Consensus Estimate for earnings of $4.53 has increased nearly 1% over the last 30 days. The figure reflects year-over-year improvement of 19.2%.

For the quarter to be reported, the Zacks Consensus Estimate for sales is $604.2 million. This indicates growth of 9.8% year over year.

A Likely Positive Surprise?

According to our quantitative model, chances of Affiliated Managers beating the Zacks Consensus Estimate are high this time around. This is because it has the right combination of the two key ingredients — a positive Earnings ESP and a Zacks Rank #3 (Hold) or better — for increasing the odds of an earnings beat.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks ESP: The Earnings ESP for Affiliated Managers is +0.24%.

Zacks Rank: Affiliated Managers has a Zacks Rank #2 (Buy), which further increases the predictive power of ESP.

Factors to Influence Q4 Results

Affiliated Managers holds an almost unbeaten track record of buying equity interests in asset management companies with strong performance-oriented products. The past equity investments are expected to continue boosting the company’s top line, driven by the excellent long-term performance of its affiliates.

The company expects performance fees in the quarter to be in the range of 70 cents to $1.20 per share.

Management expects the ratio of adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) to average AUM to be in the 16-18 basis points range for the to-be-reported quarter. Further, other economic items are projected to be around $1 million per quarter.

On the cost front, management projects total interest expenses of around $19.5 million in the fourth quarter, down sequentially. Amortization expenses are projected to be $42 million, almost in line on a sequential basis.

Moreover, for 2017, management expects economic earnings per share to be in the range of $13.75 to $15.75. This is based on assumptions of market performance till Jan 27, 2017, 2% quarterly market growth beginning second-quarter 2017, performance fee contribution of 13% and share repurchase plan.

Other Stocks That Warrant a Look

Here are a few other finance stocks you may want to consider, as our model shows that these have the right combination of elements to post an earnings beat this time around.

T. Rowe Price Group (NASDAQ:TROW) has an Earnings ESP of +1.67% and carries a Zacks Rank #2. It is scheduled to report results on Jan 30.

Apollo Global Management, LLC (NYSE:APO) is slated to report results on Feb 1. It has an Earnings ESP of +4.30% and carries a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Eaton Vance Corp. (NYSE:EV) has an Earnings ESP of +0.64% and a Zacks Rank #1. The company is expected to release its results on Feb 28.

Today's Stocks from Zacks' Hottest Strategies

It's hard to believe, even for us at Zacks. But while the market gained +18.8% from 2016 - Q1 2017, our top stock-picking screens have returned +157.0%, +128.0%, +97.8%, +94.7%, and +90.2% respectively.

And this outperformance has not just been a recent phenomenon. Over the years it has been remarkably consistent. From 2000 - Q1 2017, the composite yearly average gain for these strategies has beaten the market more than 11X over. Maybe even more remarkable is the fact that we're willing to share their latest stocks with you without cost or obligation.

See Them Free>>

Palantir remains highly valued with a 460x P/E ratio and a 42.5x P/B ratio, far above its peers. The stock's beta of 2.81 signals high volatility, meaning sharp moves in both...

The S&P 500 had started to clear resistance, posting new all-time highs before sellers struck with a vengeance. The selling was bad, similar to that seen in December, which...

Myself and others have highlighted how European Equities have been breaking out to new all-time highs on the back of bullish factors such as cheap valuations, monetary tailwinds,...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.