Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Campbell Soup Company (NYSE:CPB) is slated to release first-quarter fiscal 2018 results on Nov 21. The question lingering in investors’ minds is, whether this convenience foods behemoth will be able to come up with a positive earnings surprise in the quarter to be reported.

The company missed the Zacks Consensus Estimate in the last two quarters. It delivered an average negative earnings surprise of 1.2% in the trailing four quarters.

Estimates Trend

The Zacks Consensus Estimate for the fiscal first quarter is pegged at 97 cents compared with $1 in the year-ago period. Estimates have been stable in the last 30 days. Further, analysts polled by Zacks expect revenues of roughly $2.2 billion, down 1% from the prior-year quarter.

Factors at Play

Campbell Soup has been struggling to revive its top line, which hasn’t witnessed year-over-year growth for quite some time. Moreover, it has missed the Zacks consensus mark for three straight quarters now. Known for its canned foods, much of the sales debacle could be attributable to consumers’ changing eating patterns and their evolving preferences for healthy, fresh and organic food products. Nevertheless, the company’s Campbell Fresh (C-Fresh) division recovered slightly in the fourth quarter of fiscal 2017, after it was marred by lingering constraints related to the Bolthouse Farms Protein PLUS drinks recall in June 2016.

These factors have also weighed upon the company’s shares that lost 21.9% so far this year, wider than the industry's decline of 9.5%.

Further, the company anticipates the operating environment to remain challenging in fiscal 2018, wherein it expects to witness cost inflation. The company’s earlier guidance indicates that the first-half results will remain significantly soft.

Additionally, stiff competition in the food industry and rising commodity prices might dent the company’s performance in the near term.

Nevertheless, Campbell Soup is on track with its four core plans including focus on real food philosophy and transparency, undertaking robust digital endeavors, portfolio diversification and concentrating on growing its snacks brands. Meanwhile, the company is progressing well with its cost savings plan, which evidently helped it achieve gross margin, EBIT and earnings growth in fiscal 2017.

So let’s wait and see whether these obstacles are offset by the company’s robust brand portfolio, solid cost-savings and four core plans.

What the Zacks Model Unveils?

Our proven model does not show that Campbell Soup is likely to beat earnings estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

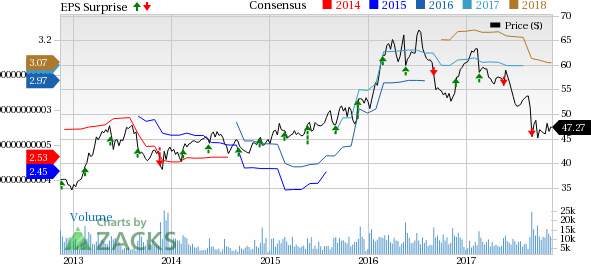

Campbell Soup Company Price, Consensus and EPS Surprise

Campbell Soup Company Price, Consensus and EPS Surprise | Campbell Soup Company Quote

While Campbell Soup has an Earnings ESP of +0.70%, its Zacks Rank #4 (Sell) makes surprise prediction difficult.

As it is, we caution against stocks with a Zacks Rank #4 or 5 (Strong Sell) going into the earnings announcement, especially when the company is seeing negative estimate revisions.

Stocks With Favorable Combination

Here are some companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

The J. M. Smucker Company (NYSE:SJM) has an Earnings ESP of +0.62% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Ollie's Bargain Outlet Holdings, Inc. (NASDAQ:OLLI) has an Earnings ESP of +1.82% and a Zacks Rank #3.

Mondelez International, Inc. (NASDAQ:MDLZ) has an Earnings ESP of +0.04% and a Zacks Rank #3.

Today's Stocks from Zacks' Hottest Strategies

It's hard to believe, even for us at Zacks. But while the market gained +18.8% from 2016 - Q1 2017, our top stock-picking screens have returned +157.0%, +128.0%, +97.8%, +94.7%, and +90.2% respectively.

And this outperformance has not just been a recent phenomenon. Over the years it has been remarkably consistent. From 2000 - Q1 2017, the composite yearly average gain for these strategies has beaten the market more than 11X over. Maybe even more remarkable is the fact that we're willing to share their latest stocks with you without cost or obligation.

See Them Free>>

The big US stocks dominating markets and investors’ portfolios just finished another earnings season. They reported spectacular collective results including record sales, profits,...

“Quality” stocks with strong fundamentals tend to be rewarding places to stash hard-earned money. Since 2009, investing in a basket of quality stocks over a standard index has...

Palantir Technologies (NASDAQ:PLTR) continues to sell off. On March 6, PLTR stock fell over 10% on nearly double the daily volume, bringing its 30-day decline to over 27%. A drop...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.