Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

We issued an updated research report on Wells Fargo & Company (NYSE:WFC) on Nov 20. The San Francisco-based company has traditionally followed organic and inorganic growth strategies. However, it is struggling with legal issues and escalating costs.

Troubles mounted for Wells Fargo following the revelation of opening of millions of unauthorized accounts in 2016. ‘Cross-selling’, which has been the company’s core strength in recent years, drew regulators’ attention after it was discovered that numerous employees of the bank had unlawfully enrolled consumers in products and services without any consent.

This was followed by the disclosure of issues in the bank’s auto insurance business and online bill pay services. Though Wells Fargo is taking necessary steps to address the issue, it undoubtedly puts the company’s financials under pressure for the near term.

In the past few quarters, the company has been witnessing higher non-interest expenses. Wells Fargo is focused on expense management with the target of reducing $4 billion in costs by 2019. However, the company’s bottom line will continue to be hurt in the near term by legal expenses related to the sales scam and other litigation issues.

Though the company has an impressive capital deployment plan with a decent dividend payout ratio, its debt/equity ratio compares unfavorably with that of the industry. Moreover, the company’s volatile performance in the past few quarters indicates that its capital deployment activities might not be sustainable, which will disappoint shareholders.

However, easing margin pressure and substantial deposits provide some respite to the company. At the same time, Wells Fargo’s financials exhibit improving credit metrics.

Nevertheless, analysts have a negative outlook on the stock. As a result, in the past 30 days, the Zacks Consensus Estimate for 2017 earnings has declined marginally to $3.97 per share from $4.00. The estimate for 2018 earnings has been stable at $4.32.

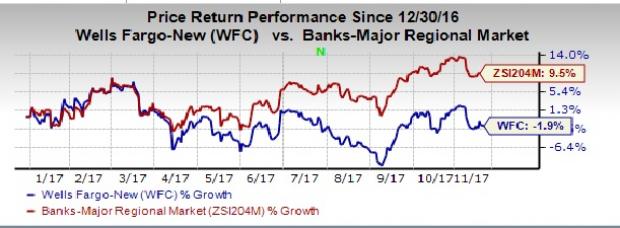

Wells Fargo currently carries a Zacks Rank #4 (Sell). Notably, the stock has lost 1.9% since the beginning of 2017.

Walgreens Boots Alliance Inc. (NASDAQ:WBA) is on the brink of a significant transformation as it nears a deal with Sycamore Partners to become a private entity. The transaction,...

Using the Elliott Wave Principle (EWP), we have been successfully tracking the most likely path forward for the S&P 500 (SPX) over several months. Although there are many ways...

When looking for dividend stocks, high dividend yields are one important factor to consider. Even if a company’s dividend yield isn’t nearing double-digit percentages, finding...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.