Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Value investing is easily one of the most popular ways to find great stocks in any market environment. After all, who wouldn’t want to find stocks that are either flying under the radar and are compelling buys, or offer up tantalizing discounts when compared to fair value?

One way to find these companies is by looking at several key metrics and financial ratios, many of which are crucial in the value stock selection process. Let’s put Taylor Morrison Home Corporation (NYSE:TMHC) stock into this equation and find out if it is a good choice for value-oriented investors right now, or if investors subscribing to this methodology should look elsewhere for top picks:

PE Ratio

A key metric that value investors always look at is the Price to Earnings Ratio, or PE for short. This shows us how much investors are willing to pay for each dollar of earnings in a given stock, and is easily one of the most popular financial ratios in the world. The best use of the PE ratio is to compare the stock’s current PE ratio with: a) where this ratio has been in the past; b) how it compares to the average for the industry/sector; and c) how it compares to the market as a whole.

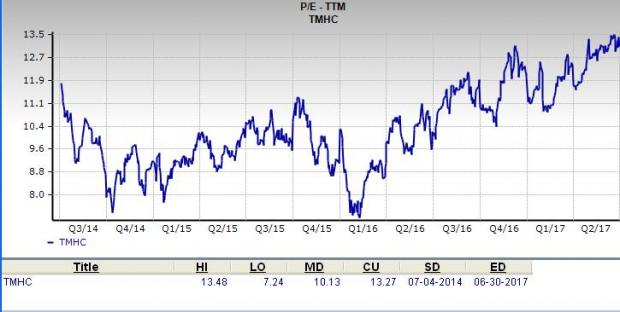

On this front, Taylor Morrisonhas a trailing twelve months PE ratio of 13.27, as you can see in the chart below:

This level actually compares pretty favorably with the market at large, as the PE for the S&P 500 compares in at about 20.18. If we focus on the stock’s long-term PE trend, the current level puts Taylor Morrison’s current PE ratio above its midpoint over the past five years, with the number having risen rapidly over the past few months.

Further, the stock’s PE also compares favorably with the Zacks classified Building Products - Home Builders sector’s trailing twelve months PE ratio, which stands at 14.27. At the very least, this indicates that the stock is relatively undervalued right now, compared to its peers.

We should also point out that Taylor Morrisonhas a forward PE ratio (price relative to this year’s earnings) of just 12.53, so it is fair to say that a slightly more value-oriented path may be ahead for Taylor Morrisonstock in the near term too.

P/S Ratio

Another key metric to note is the Price/Sales ratio. This approach compares a given stock’s price to its total sales, where a lower reading is generally considered better. Some people like this metric more than other value-focused ones because it looks at sales, something that is far harder to manipulate with accounting tricks than earnings.

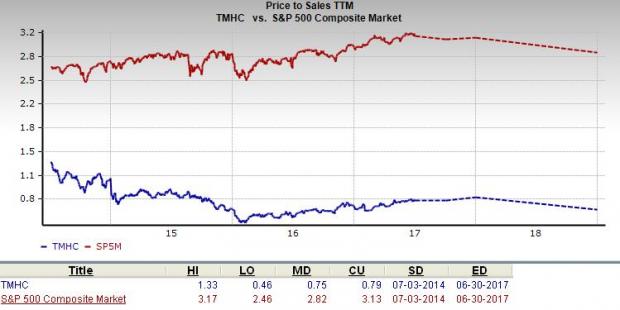

Right now, Taylor Morrison has a P/S ratio of about 0.79. This is significantly lower than the S&P 500 average, which comes in at 3.13 right now. Also, as we can see in the chart below, this is well below the highs for this stock in particular over the past few years.

If anything, TMHC is in the median end of its range in the time period from a P/S metric, suggesting that the company’s stock price has already appreciated to some degree, relative to its sales.

Broad Value Outlook

In aggregate, Taylor Morrisoncurrently has a Zacks Value Style Score of ‘A’, putting it into the top 20% of all stocks we cover from this look. This makes Taylor Morrisona solid choice for value investors, and some of its other key metrics make this pretty clear too.

For example, the P/CF ratio (a great indicator of value) comes in at 6.55, which is far lower than the industry average of 8.88. Clearly, TMHC is a solid choice on the value front from multiple angles.

What About the Stock Overall?

Though Taylor Morrisonmight be a good choice for value investors, there are plenty of other factors to consider before investing in this name. In particular, it is worth noting that the company has a Growth grade of ‘A’ and a Momentum score of ‘A’. This gives TMHC a Zacks VGM score—or its overarching fundamental grade—of ‘A’. (You can read more about the Zacks Style Scores here >>)

Meanwhile, the company’s recent earnings estimates have been mixed at best. The current quarter has seen two estimates go higher in the past sixty days compared to two lower, while the full year estimate has seen three up in the same time period.

This has had a significant impact on the consensus estimate as the current quarter consensus estimate has decreased by 5% in the past two months, while the full year estimate has inched upper by 1%. You can see the consensus estimate trend and recent price action for the stock in the chart below:

Taylor Morrison Home Corporation Price and Consensus

Taylor Morrison Home Corporation Price and Consensus | Taylor Morrison Home Corporation Quote

This positive trend signifies bullish analyst sentiment, and its Zacks Rank #2 (Buy) indicates robust fundamentals and expectations of outperformance in the near term.

Bottom Line

Taylor Morrisonis an inspired choice for value investors, as it is hard to beat its incredible lineup of statistics on this front. Furthermore, a strong industry rank (among Top 14% of more than 250 industries) and a Zacks Rank #2 instill our confidence on the stock.

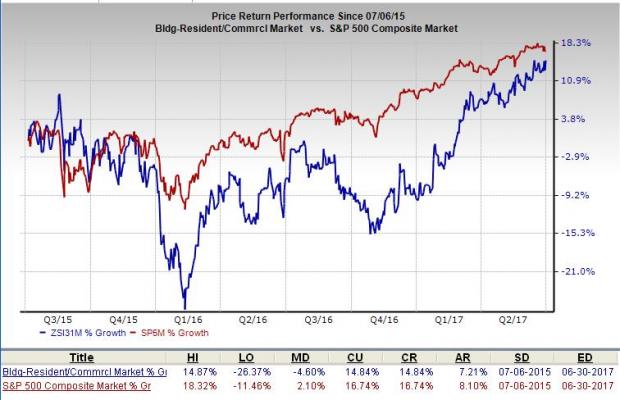

On the flipside, over the past two years, the Zacks Building Products - Home Builders industry has clearly underperformed the broader market, as you can see below:

Despite an unsatisfactory past industry performance, a good industry and Zacks rank signal that the stock is likely to benefit from favorable broader factors in the immediate future. Add to this robust value metrics, and we believe that we have a strong value contender in Taylor Morrison.

5 Trades Could Profit ""Big-League"" from Trump Policies

If the stocks above spark your interest, wait until you look into companies primed to make substantial gains from Washington's changing course.

Today Zacks reveals 5 tickers that could benefit from new trends like streamlined drug approvals, tariffs, lower taxes, higher interest rates, and spending surges in defense and infrastructure. See these buy recommendations now >>

The markets have been sluggish this week as investors hope for a jolt later in the week when AI juggernaut NVIDIA Corporation (NASDAQ:NVDA) reports fourth quarter and year-end...

On Friday, a wave of selling pressure swept across the US equity markets, leaving a trail of losses. The S&P 500 closed down 1.7%, the DOW slid 1.69%, and the NASDAQ tumbled a...

Palantir remains highly valued with a 460x P/E ratio and a 42.5x P/B ratio, far above its peers. The stock's beta of 2.81 signals high volatility, meaning sharp moves in both...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.