Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

NetApp Inc. (NASDAQ:NTAP) reported fiscal second-quarter 2018 non-GAAP earnings of 81 cents per share, beating the Zacks Consensus Estimate of 69 cents per share. The figure surged 35% on a year-over-year basis and was also within the guided range.

Revenues of $1.42 billion increased 6% from the year-ago quarter, surpassing the Zacks Consensus Estimate of $1.38 billion. The figure met management’s expectation.

The impressive second-quarter results were driven by the company’s successful ongoing transition from underperforming segments to growth oriented sectors like all-flash arrays and hybrid cloud and Data Fabric strategies.

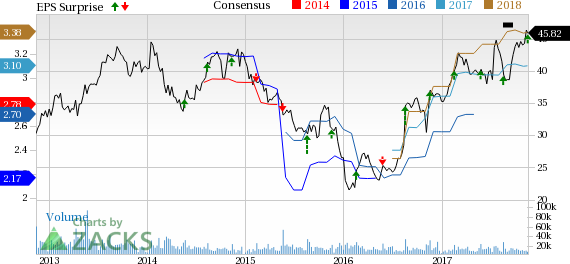

NetApp stock has gained 29.9% year to date, substantially outperforming the 21.9% rally of the industry it belongs to.

Segment Details

Product revenues (56.8% of total revenues) increased 14% year over year to $807 million. This was the fourth consecutive quarter of product revenue growth, which per the company was mainly driven by its “successful pivot to the growth areas of the market.”

Strategic solutions comprised 69% of net product revenues. It increased 23% on a year-over-year basis. Mature solutions revenues declined 3.1% from the year-ago quarter.

Software Maintenance revenues of $375 million (26.4% of total revenue) decreased 3.4% from the year-ago quarter. Revenues from Hardware Maintenance & Other Services (16.8% of total revenue) declined 8% year over year to $240 million.

Management was particularly optimistic about its expanded partnership with Microsoft (NASDAQ:MSFT) Azure for the development of the industry’s first cloud-based enterprise Network File System (NFS) to be delivered via Azure.

The company is positive about making the most of the exponential rate of data growth with its cloud-integrated all-flash solutions that fits well with hybrid cloud infrastructure. During the second quarter, the company’s all-flash array business surged 60% on a year-over-year basis. Its annualized net revenue run rate was $1.7 billion.

The company’s expertise in the flash array market is aiding its popularity in storage area network (SAN) and converged infrastructure markets. Management noted that the company is winning market share against competitors like HP, International Business Machines (NYSE:IBM) and EMC (NYSE:EMC). The company’s newly launched hyper-converged infrastructure is also expected to be a positive for the top line in the long run.

NetApp, Inc. Price, Consensus and EPS Surprise

NetApp, Inc. Price, Consensus and EPS Surprise | NetApp, Inc. Quote

Margin Details

Non-GAAP gross margin was 64.3%, which was better than the guided range of 63–63.5%. Also, it expanded 160 basis points (bps) from the year-ago quarter on the back of higher product gross margin of 51.8%.

Software maintenance gross margin remained flat year over year. Hardware maintenance and other services gross margin increased 200 bps on a year-over-year basis.

Non-GAAP operating margin expanded 310 bps on a year-over-year basis to 19.1%.

Balance Sheet

NetApp exited the quarter with $6 billion in cash and short-term investments. The company generated cash from operations of $314 million during the quarter compared with $250 million in the previous quarter. Further, the company repurchased shares worth $150 million and paid $54 million as dividends in the reported quarter.

Guidance

For third-quarter fiscal 2018, NetApp expects non-GAAP earnings per share in the range of 86-94 cents. The Zacks Consensus Estimate for the current quarter is pegged at 84 cents.

Net revenues are anticipated to be in the range of $1.43-$1.58 billion, which at the mid-point implies 6.8% growth from the year-ago quarter. The Zacks Consensus Estimate is currently pegged at $1.43 billion.

NetApp expects gross margin in the range of 62.5-63.5% and operating margin of approximately 20%.

Management remains hopeful that the performance of the sales team, its differentiated product portfolio and strong distribution channels will keep demand and adoption of the products strong going ahead.

Zacks Rank & Key Pick

NetApp has a Zacks Rank #2 (Buy).

A top-ranked stock in the broader technology sector is NVIDIA Corporation (NASDAQ:NVDA) , sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings growth rate for NVIDIA is projected to be 11.2%.

Zacks’ Best Private Investment Ideas

While we are happy to share many articles like this on the website, our best recommendations and most in-depth research are not available to the public.

Starting today, for the next month, you can follow all Zacks' private buys and sells in real time. Our experts cover all kinds of trades… from value to momentum . . . from stocks under $10 to ETF and option moves . . . from stocks that corporate insiders are buying up to companies that are about to report positive earnings surprises. You can even look inside exclusive portfolios that are normally closed to new investors.

Click here for Zacks' private trades >>

Investors are on edge about what tariff policy means for markets Coming off a strong Q4 earnings season, fresh February corporate sales figures can help assess the macro...

Broadcom stock is in a dynamic rebound phase. Markets seem optimistic ahead of the earnings release. Let's take a deep dive into what to expect from the report. Get the...

Consumers are feeling the pinch from inflation every time they go to the grocery store. Money is a zero-sum game; as disposable income and buying power erodes, consumers are...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.