Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Micron Technology, Inc. (NASDAQ:MU) started fiscal 2018 on a strong note, reporting outstanding results for the first quarter. The memory-chip maker’s quarterly earnings and revenues not only marked significant year-over-year growth but also came ahead of its guidance range and the Zacks Consensus Estimate.

Apart from this, the company’s gross margin, operating income and free cash flow reached a record level during the fiscal first quarter. President and CEO of Micron — Sanjay Mehrotra — noted that the overwhelming quarterly results were mainly “driven by double-digit sequential revenue growth in mobile, server and SSD applications, with expanded gross margins and improved profitability.”

Micron’s shares rallied approximately 5.4% in the extended trading hours yesterday. Notably, the stock has appreciated 110.3% in the year-to-date (YTD) period, significantly outperforming the S&P 500 return of just 20.6%.

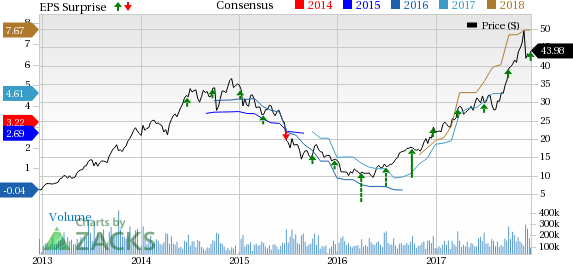

Micron Technology, Inc. Price, Consensus and EPS Surprise

Micron Technology, Inc. Price, Consensus and EPS Surprise | Micron Technology, Inc. Quote

Balance Sheet and Cash Flow

The company exited the fiscal first quarter with cash and short-term investments of $6.174 billion compared with $5.428 billion at the end of fourth-quarter fiscal 2018. Receivables were $3.876 billion compared with $3.759 billion recorded in the previous quarter. Micron’s long-term debt decreased to $7.644 billion from $9.872 billion in the previous quarter.

The company generated operating cash flow of $3.6 billion and free cash flow of $1.7 billion during the reported quarter. Capital expenditure was $1.9 billion in the fiscal first quarter.

Outlook

The company provided outlook for second-quarter fiscal 2018. For the quarter, Micron expects revenues in the range of $6.8-$7.2 billion. The Zacks Consensus Estimate is pegged at $6.08 billion.

Non-GAAP gross margin is projected to be between 54% and 58%. Operating expenses on non-GAAP basis are likely to be in the range of $625-$675 million and operating income is anticipated to come in the band of $3.25-$3.45 billion.

The company expects non-GAAP earnings per share in the range of $2.51-$2.65 per share. The Zacks Consensus Estimate is pegged at $1.95.

Furthermore, Micron has capital expenditure plans worth $7.5 billion for fiscal 2018. During the fourth-quarter fiscal 2017 earnings conference call, Maddock had noted that CapEx “will be focused on technology transition and product enablement.” He had also mentioned that the company has no plans for wafer capacity additions in fiscal 2018.

Our Take

Micron’s impressive fiscal first-quarter results and an upbeat second-quarter outlook downplay all speculations that memory-chip makers’ super cycle is nearing its end. The mess started on Nov 27, after analyst Shawn Kim of Morgan Stanley (NYSE:MS) noted that NAND flash memory-chip prices are at peak levels, but may start declining from the beginning of 2018 due to a supply glut.

This created panic among investors who preferred to pull out their investments from this space, leading to a massive sell-off seen in memory chip makers’ shares.

However, Micron’s fiscal second-quarter outlook reflects that the entire industry will continue its outperformance as long as demand for memory chips remains ahead of supply.

Currently, Micron carries a Zacks Rank #2 (Buy).

Some other top-ranked semiconductor stocks are NVIDIA Corporation (NASDAQ:NVDA) , Intel Corporation (NASDAQ:INTC) , and STMicroelectronics N.V. (NYSE:STM) , all sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

NVIDIA, Intel and STMicroelectronics have long term-expected EPS growth rates of 10.3%, 8.4% and 5%, respectively.

5 Medical Stocks to Buy Now

Zacks names 5 companies poised to ride a medical breakthrough that is targeting cures for leukemia, AIDS, muscular dystrophy, hemophilia, and other conditions.

New products in this field are already generating substantial revenue and even more wondrous treatments are in the pipeline. Early investors could realize exceptional profits.

Click here to see the 5 stocks >>

The markets have been sluggish this week as investors hope for a jolt later in the week when AI juggernaut NVIDIA Corporation (NASDAQ:NVDA) reports fourth quarter and year-end...

On Friday, a wave of selling pressure swept across the US equity markets, leaving a trail of losses. The S&P 500 closed down 1.7%, the DOW slid 1.69%, and the NASDAQ tumbled a...

Palantir remains highly valued with a 460x P/E ratio and a 42.5x P/B ratio, far above its peers. The stock's beta of 2.81 signals high volatility, meaning sharp moves in both...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.