Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Shares of J. C. Penney Company, Inc. (NYSE:JCP) , which have tanked 66.7% in a year, wider than the industry’s slump of 39.9%, took a sharp U-turn and rallied 15.3% on Nov 10. This upside was witnessed after the company impressed investors with third-quarter fiscal 2017 results.

The company’s bottom line came in above the Zacks Consensus Estimate after missing it in the preceding quarter, while the top line surpassed the same for the second time in row. However, the big take away from this quarter was rise in comparable-store sales (comps) that marked the best quarterly performance since fiscal 2016.

Let’s Unveil the Picture

J. C. Penney posted adjusted loss per share of 33 cents, narrower than the Zacks Consensus Estimate of a loss of 43 cents. In the prior-year quarter, the company had reported loss of 21 cents. Also, the company delivered net loss of 41 cents on a GAAP basis, wider than the loss of 22 cents a year- ago.

The company’s total net sales of $2,807 million surpassed the Zacks Consensus Estimate of $2,759 million but slipped 1.8% year over year after witnessing a gain of 1.5% preceding quarter. The year-over-year decline in sales was primarily due to store closures. So far in the year, the company had shut down 139 stores.

However, comps inched up 1.7% compared with a decline of 0.8% in the prior-year quarter. During the quarter, home, Sephora, footwear and handbags were the best performing divisions that outweighed the company’s total comps.

Gross profit in the quarter decreased 10.1% to $955 million, while gross margin contracted 320 basis points (bps) to 34%. Adjusted EBITDA declined to $108 million from $174 million in the prior-year quarter, while adjusted EBITDA margin decreased 230 bps to 3.8%.

Financial Details

J. C. Penney ended the quarter with cash and cash equivalents of $185 million, long-term debt of $4,039 million and shareholders’ equity of $1,078 million. Merchandise inventory levels decreased 8.8% to $3,365 million.

In the reported quarter, the company also generated negative free cash flow of $327 million. Further, it incurred capital expenditures of $95 million down from $122 million in the year-earlier quarter.

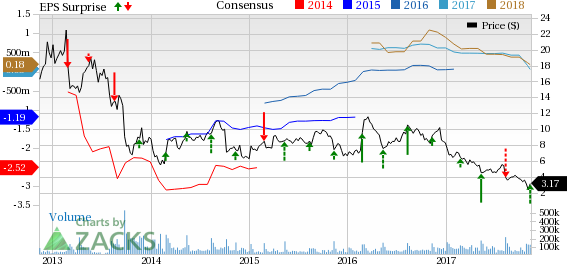

J.C. Penney Company, Inc. Holding Company Price, Consensus and EPS Surprise

J.C. Penney Company, Inc. Holding Company Price, Consensus and EPS Surprise | J.C. Penney Company, Inc. Holding Company Quote

2017 Outlook

For fiscal 2017, the comps are projected in the range of down 1% to flat. Cost of goods sold is now forecast to increase by 100-120 bps year over year. The company expects adjusted earnings per share in the band of 2-8 cents. The stock has seen the Zacks Consensus Estimate for fiscal 2017 being pegged at 6 cents.

J. C. Penney carries a Zacks Rank #3 (Hold).

Interested in the Retail Space? Check These

Some better-ranked stocks worth considering from the retail space are American Eagle Outfitters, Inc. (NYSE:AEO) , Boot Barn Holdings, Inc. (NYSE:BOOT) and Shoe Carnival (LON:CCL), Inc. (NASDAQ:SCVL) , each carrying a Zacks Rank #2 (Buy). You can seethe complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

American Eagle Outfitters delivered an average positive earnings surprise of 3.4% in the trailing four quarters and has a long-term earnings growth rate of 8.7%.

Boot Barn Holdings has an impressive long-term earnings growth rate of 15.7%.

Shoe Carnival delivered an average positive earnings surprise of 20% in the trailing four quarters and has a long-term earnings growth rate of 12%.

Will You Make a Fortune on the Shift to Electric Cars?

Here's another stock idea to consider. Much like petroleum 150 years ago, lithium power may soon shake the world, creating millionaires and reshaping geo-politics. Soon electric vehicles (EVs) may be cheaper than gas guzzlers. Some are already reaching 265 miles on a single charge.

With battery prices plummeting and charging stations set to multiply, one company stands out as the #1 stock to buy according to Zacks research.

It's not the one you think.

• Trump’s trade war, inflation data, and last batch of earnings will be in focus this week. • DoorDash’s imminent inclusion in the S&P 500 is likely to trigger a wave of...

The big US stocks dominating markets and investors’ portfolios just finished another earnings season. They reported spectacular collective results including record sales, profits,...

“Quality” stocks with strong fundamentals tend to be rewarding places to stash hard-earned money. Since 2009, investing in a basket of quality stocks over a standard index has...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.