Although retail e-commerce is the segment that most of us are interested in, it is in fact just a part of the overall e-commerce market. Retailers and service providers generate just 4.7% and 3.0%, respectively of their revenues online, a slightly higher percentage than they did in the prior year. The U.S. Census Bureau categorizes these two segments as business-to-consumer.

According to the U.S. Census Bureau, the manufacturing sector is the largest contributor to e-commerce sales (49.3% of their total shipments), followed by merchant wholesalers (24.3% of their total sales). These two segments make up the business-to-business category.

This places the business-to-business category at 90% of total e-commerce sales, with the balance coming from the business-to-consumer category. The latest numbers from the Bureau suggest that the fastest-growing segments were retail and wholesale. [All the above data from the U.S. Census Bureau relate to 2011, as published in May 2013.]

The industry is evolving very rapidly, so data collection and evaluation are particularly difficult. Consequently, one has to rely largely on surveys by both government and private agencies.

In this section, we will discuss segments of the e-commerce market than do not relate directly to the retail of goods, and discuss instead travel, payments, security and advertising.

Travel

The U.S. Commerce Department expects international travel to the U.S. to continue increasing over the next few years. Visitor volume is currently expected to increase 3.7-4.2% a year from 2013 to 2017 leading to a 26% increase in the number of users by 2018. Visitors from the Caribbean are expected to be the slowest-growing (1%). The Middle East, Asia and South America are expected to grow 67%, 60% and 52%, respectively.

The fastest growth is expected to come from China (229%), Saudi Arabia (191%), Russian Federation (79%), Brazil (66%), Argentina (65%) and Columbia (54%).

The Travel and Tourism industry remains one of the country’s strongest industries, although the second quarter (latest available data) saw a deceleration in its growth rate. According to the BEA, lower air passenger travel as well as reduced automotive rental and leasing affected the industry during the quarter. As a result, the industry grew 2.5% in the quarter, same as the real GDP growth of 2.5% (in the first quarter it grew 7.3% compared to GDP growth of 1.1%).

The top travel booking sites are Booking.com, Expedia.com, Hotels.com, Priceline.com, Kayak.com (acquired by Priceline), Travelocity.com, Orbitz.com and Hotwire.com. Since Booking.com and Kayak are part of Priceline (PCLN) and both Hotels.com and Hotwire.com part of Expedia (EXPE), this narrows down the top companies in the segment to Priceline, Expedia, Orbitz Worldwide (OWW - Snapshot Report) and Travelocity. However, there are several others worth considering that include Ctrip International (CTRP), MakeMyTrip (MMYT - Snapshot Report), TripAdvisor (TRIP - Snapshot Report), which was spun off from Expedia, and Qunar , which recently had its IPO.

The global travel market grew 4% in 2012 and is expected to grow another 2-3% this year. The Asia/Pacific region is expected to see the strongest growth (up 6%), followed by Europe and South America (mainly Brazil) at 2% each. North America (mainly U.S. is expected to be flat this year [World Travel Monitor 2012].

According to the June 2013 TravelClick North American Hospitality Review (NAHR), both occupancy and average daily rates (ADRs) in North America are seeing steady growth this year. Occupancy rates grew much more than ADRs most categories, indicating that demand is coming at the cost of prices. Individual occupancy was higher than group occupancy with individual leisure occupancy being stronger than business occupancy. In the second quarter of 2013, total travel occupancy grew 5.3% from last year with ADR growth at 3.5%.

Group travel is expected to be flattish in the September quarter, although individual travel (both in terms of occupancy and ADRs) is expected to accelerate.

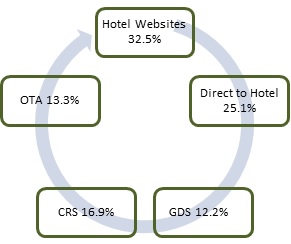

Online travel agents (OTAs) are growing the fastest this year: up 11.7% in the second quarter, according to the TravelClick North American Distribution Review (NADR). The hotels’ own websites were up 8.1%, with direct walk-ins and calls to the hotel growing 4.4%. The global distribution system, used by travel agents and CRS (calls to a hotel's toll-free number) were also up 5.7% and 3.7%, respectively, reversing a negative trend.

Share of room nights based on actual reservations-

Reservations

Smartphones are playing a key role in travel purchases, especially for last minute purchases. eMarketer expects smartphone travel researchers in the U.S. to grow to 50 million or 40% of all digital travel researchers this year, with total U.S. mobile travel sales touching $13.6 billion.

The top site for travel content is TripAdvisor, visited by 60% of Americans when choosing a hotel.

Google’s (GOOG) YouTube is now growing in popularity and is the second in line, according to MMGY Global's 2013 Portrait of American Travelers study.

Another report by PhocusWright mentioned that when online penetration of the travel market reached 35% in any country, growth rates were likely to slow down to single-digits. The research firm mentioned that only the U.S., U.K. and Scandinavia had reached this level of penetration and most other markets across Europe, Asia and Latin America would continue to show good growth rates.

Payment Systems With practically all market research indicating solid growth in e-commerce sales over the next few years, online players are vying with each other to come out with convenient and secure payment solutions. There are a host of payment systems in the market, but the greatest progress has been made on near field communication (NFC), quick response (QR) code, Soundwave and Bluetooth low energy (BLE).

The latest to enter the fray is

Amazon (AMZN) with its "Login and Pay with Amazon" system. Recognizing the most-used mobile and computing platforms, the system works on any desktop or tablets/smartphones running Android or iOS operating systems. Amazon’s payment system is likely to be popular with retailers given its huge customer base. For Amazon, it will also facilitate further data collection and position it strongly versus

eBay’s (EBAY) Paypal and Google’s Digital Wallet.

By far the most successful mobile payment system is Paypal, which has come a long way from a mere online payment service. Last year, the company inked a deal with

Discover Network (DFS), the fourth largest credit card company, bringing its seven million plus retailers onto the Paypal network. Paypal has also signed up a large number of traditional retailers such as

The Home Depot (

HD) and

Office Depot (OD). The company is now selling its marketing services as a bundled solution to retailers and the success of this strategy is evident in Paypal’s growth numbers.

The new digital wallet from Google enables in-app purchase and mobile payments in addition to PoS purchases and money transfer. Other than the credit and debit card information, users can now store loyalty cards, discount coupons and offers that they can apply during purchase. More importantly, Google has found a way to reduce its dependence on NFC technology. A non-NFC-enabled phone can now use the Wallet to transfer funds from any of the accounts saved in it.

Google now requires app developers for the Android platform to compulsorily use its payment service instead of a competing service from eBay or others. Despite the strong growth in Android devices, Google Play (its app store) has not done that well, partly because of the many steps to conversion that turns customers away. The simplification of the checkout process should help sales on Google Play.

Apple (AAPL) has removed NFC compatibility from its devices and also introduced iBeacon, which is a BLE technology. The technology tracks the approximate location of a person, the time spent at different stores and even the location within the store. It has the potential to push highly relevant offers and promos at opportune moments.

Apple has accumulated a large number of patents for payment processing and it’s very likely that that iBeacon will be rolled into its very own iWallet. Payments on its platform are currently handled by its Passbook system. Apple is one of the largest online retailers although it also sells through traditional retail outlets, so a payment platform from Apple may be expected to catch on very fast.

The FIS Mobile Wallet from

Fidelity National Information Services Inc. (FIS) is basically a bar code reader that feeds information related to the purchase into the user’s smartphone and uses it as a medium to transfer the information to the cloud. Online purchase of merchandise is also possible. The solution provides good security, since the transaction is carried out entirely in the cloud through the retailer’s and banker’s applications and personal information is not shared at the time of purchase.

Visa (

V) has also jumped on the bandwagon, claiming that its V.me is a digital wallet with a difference. Not only can it be used to make mobile contactless payments (bar code, QR code or NFC), but it can also be used for online checkout (it remembers card details from several providers).

Mobile banking is set to grow very strongly over the next few years, according to Juniper Research. The research firm estimates that a billion mobile devices (or 15% of the installed base) will be used for banking transactions by 2017, up from an expected 590 million at the end of this year. Most banks already offer at least one mobile banking offering, with some larger banks offering more than one option. Messaging remains most popular across the world, but apps are likely to remain the preferred channel in most developed markets.

Mobile banking has not picked up sufficiently in either the U.S. or Canada, due to security-related concerns. However, an analysis by Deloitte shows that mobile banking could become the most-preferred banking method by 2020. The study estimates that 20-25 million Generation-Y consumers will become new banking customers by 2015.

A banking.com study shows that 48% of "Generation Y" (gen Y) consumers are already using online banking services. Moreover, their preference for online banking is so high that around 30% said they would consider switching financial institutions if they did not provide the service. Both online and mobile banking by gen Y consumers largely consists of checking account balances and transferring funds, although they also like to pay bills on the platform.

It is believed that high smartphone penetration, higher income within this group and greater digital sophistication will drive increased demand for mobile banking services. Since mobile banking is expected to be the most cost efficient for banks, investment in technology to improve and expand mobile banking services is likely to increase.

Security With online transactions expected to boom over the next few years, the topmost concern remains security. While banks will spend significantly on secure payment systems, hackers are expected to have a field day, largely targeting the flood of customers going online. Last year saw a huge increase in security breaches, something that may be expected to continue.

Recent research from McAfee revealed certain important facts: first, that mobile malware was primarily spreading through apps; second, 75% of infected apps came from Google Play; third, the chances of downloading malware or suspicious URLs was 1 in 6; fourth, 40% of malware families disrupt the system in more than one way, which is an indication of the increasing sophistication of hackers; and fifth, 23% of mobile spyware can result in data loss.

What is even more alarming is that even “secure” payment platforms like digital wallets using NFC technology can now be infected by worms within close range of devices (“bump and infect”). An infected device can give out personal information during the payment process that can be used to steal from the wallet.

Mobile security offerings currently come from AirWatch, Apple, Avast, Check Point,

Cisco (CSCO),

IBM (

IBM),

Juniper (

JNPR), Kaspersky, McAfee,

Microsoft (

MSFT), MobileIron,

Blackberry (BBRY),

Symantec (

SYMC) and Trend Micro, among others.

Alternative payment systems will continue to gain popularity. While some of these payment systems, such as PayPal, have been around for a while, other systems, such as Google’s digital wallet, V.me and the FIS Mobile Wallet are still in the making. Alternative payment systems never really gained momentum in the past because of the low volume of transactions. However, as online transactions continue to increase, many more such systems could suddenly become more available.

We expect mobile security to become a major focus area for technology companies, since this is the stumbling block to payments through the mobile platform (currently just 2% of U.S. online spending).

Digital Advertising The U.S. digital advertising market has seen some very strong growth in the past few years, despite the recession that impacted the entire economy. eMarketer estimates that the market will grow 14.9% in 2013, compared to the 15.0% growth in 2012.

Growth rates are expected to continue declining: 12.6% in 2014, 10.3% in 2015, 9.2% in 2016 and 7.1% in 2017. Retail, financial services, consumer packaged goods (CPG) and travel in that order, are expected to drive this growth. The slight upward revision is attributed to previous estimates is driven by strength on the mobile platform, which will grow 95.0% in 2013, 53.8% in 2014, 41.8% in 2015, 33.1% in 2016 and 26.0% in 2017. Spending on mobile ads is expected to increase as a percentage of total spending on digital as well as total media ads in each of the years.

The current strength in online advertising is coming primarily from the growing popularity of the display format. Of all the forms of online advertising, display (including video, banner ads, rich media and sponsorships) is expected to see the strongest growth over the next few years. The underlying drivers of growth of the display format are the continued increase in the number of users, greater propensity of users to consume online, a growing inventory of advertisements that serve to lower advertisement prices and the need to create brand awareness online.

Google’s YouTube leads in the video segment. The increasing propensity to use programmatic buying techniques (automating the inventory buying process) is hurting

Yahoo’s (

YHOO) premium placements. Yahoo is currently focusing on the content side of things in order to boost ad revenue.

Facebook (FB) on the other hand has more relevant personal data, which advertisers like. Facebook’s main problem is the decline in teen usage and low conversion for advertisers.

While digital advertising spend has been moving to non-search portals, such as Facebook, search is likely to remain relevant and important. Google is the leader here and is using its other technologies (maps, voice, devices) to make its services more invaluable to users. Its Enhanced Campaigns strategy that seeks to integrate ad campaigns across platforms is also bearing fruit, as it is proving more profitable for advertisers.

Search advertising results are measurable, and therefore more predictable, than other media. This also makes the market more resilient in recessionary conditions, since advertisers are more confident about the results of their spending.

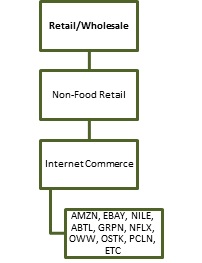

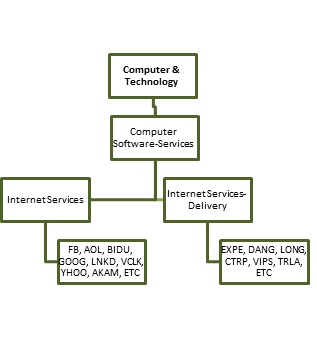

Since e-commerce entails the buying and selling of goods or services over electronic systems, it includes companies that are totally dependent on these sales, those that are gradually moving to it, as well as those that want to use it partially. Therefore, the biggest sellers or the ones growing the strongest are not necessarily those that are solely dependent on the Internet. The following diagrams seek to explain the position of companies primarily dependent on the Internet for the distribution of their goods and services in the context of the Zacks Industry Rank.

Two (Retail/Wholesale and Computer & Technology) of the 16 broad Zacks sectors are related to the e-commerce industry as depicted below.

Retail

Computer

We rank the 264 industries across the 16 Zacks sectors based on the earnings outlook and fundamental strength of the constituent companies in each industry. The outlook for industries positioned at #88 or lower is 'Positive,' between #89 and #176 is 'Neutral' and #177 and higher is 'Negative.'

Therefore, Internet Commerce and Internet Services – Delivery being in the 32nd and 95th positions, respectively are in positive territory, with Internet Services (166th position) being neutral.

So it is not surprising that the average rank of stocks in the Internet Commerce industry is 2.65, for Internet Services – Delivery, it is 2.94, while for Internet Services it is 3.06. [Note: Zacks Rank #1 denotes Strong Buy, #2 is Buy, #3 means Hold, #4 Sell and #5 Strong Sell].

Earnings Trends The broader Retail/Wholesale sector, of which Internet Commerce is a part, is not expected to do too well in the third quarter, considering the fact that both the estimated revenue and earnings beat ratios are 38.9%. The calculated earnings beat ratio based on companies that have reported thus far is just slightly higher at 40.9%.

Total earnings for the sector are estimated to increase 4.9% in the third quarter on revenue growth of 3.8%, indicating escalating costs and sluggish growth. This contrasts with an earnings growth of 9.3% on a revenue base of 6.9% in the preceding quarter.

The other companies we are discussing in the e-commerce outlook (part 2) fall under the broader Technology sector. Here we estimate a fairly strong earnings beat ratio of 71.2%, partially supported by a revenue beat ratio of 57.7%. While the estimated revenue beat ratio is consistent with the 57.7% in the previous quarter, the estimated earnings beat ratio is lower than the 75.0% calculated for the second quarter. The earnings beat ratio of companies that have reported thus far is 76.5%, better than the estimated numbers.

Total earnings in the sector were up 4.0% year over year compared to a 9.6% decline in the second quarter. Total revenues did slightly better, increasing 2.4% from last year, up from 0.6% in the second quarter.

Earnings estimates for 2013 and 2014 indicate better growth prospects in both years for Retail/Wholesale. Technology is expected to be even stronger.

OPPORTUNITIES While many of the companies discussed are expected to do well this year, there are a few stand-out opportunities.

The first is the emerging Chinese travel company

Ctrip (CTRP), which is seeing tremendous growth fueled by a growing middle class and increased consumerism in China, the shift from traditional to online media for booking travel and increased mobile usage. These trends are spurring strong growth, which has resulted in rising estimates.

The second is

Baidu (BIDU), the dominant search engine company of China. Baidu is the Google of China with tremendous opportunities. The company has been investing in the business to build a position in the mobile and video segments and the company is already seeing growing monetization on mobile. While integration of recent acquisitions and investment considerations could be a slight headwind in the next few quarters, the company is clearly moving in the right direction.

Facebook (FB) is another opportunity worth looking into. The company has seen its ad revenues swell, despite fears of reducing teen engagement and poorer-than-expected conversion for advertisers. Importantly, the company continues to innovate, frequently enhancing and/or making relevant changes to its platform. Therefore, one cant ignore the strong growth numbers and resultant surge in estimates.

WEAKNESSES We do not see a lot of weakness, although many of the companies may not be great opportunities either.

Revenue growth prospects for online travel companies Priceline, Expedia and Orbitz Worldwide are good. International expansion is a key factor driving growth for these companies and collaborative agreements with local players will be the key. Lower-value inventories in international markets are on the rise, so margins could be impacted.

Original post

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.