Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

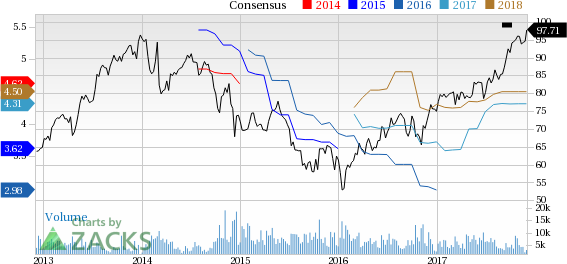

On Nov 30, Dover Corporation (NYSE:DOV) scaled a 52-week high of $98.00 during intraday trading, finally closing lower at $97.71.

Investors are optimistic on this Zacks Rank #3 (Hold) company's efforts to streamline business, solid booking and backlog growth, potential opportunities in the fast-growing digital textile printing market and an improving Energy segment.

The stock surged 31.3% in a year, higher than the S&P 500's growth of 20.2%. Dover has also outperformed the industry's 26.2% gain.

Dover Corporation Price and Consensus | Dover Corporation Quote

Further, Dover's estimate revision trend for the current year is favorable. The Zacks Consensus Estimate for the current year moved up 1% to $4.31, in the last 90 days. Its positive long-term growth rate of 13% holds promise.

Stocks to Consider

Better-ranked stocks in the same sector are Caterpillar Inc. (NYSE:CAT) , Deere & Company (NYSE:DE) and Terex Corporation (NYSE:TEX) . All three stocks flaunt a Zacks Rank #1 (Strong Buy). You can see the complete list of today's Zacks #1 Rank stocks here .

Caterpillar has an expected long-term earnings growth rate of 10.33%. Caterpillar shares have surged 48% in the past year.

Terex has an expected long-term earnings growth rate of 11.25%. Its shares have rallied 58% in a year’s time.

Deere has an expected long-term earnings growth rate of 8.2%. In the past year, its shares have gone up 48%.

5 Medical Stocks to Buy Now

Zacks names 5 companies poised to ride a medical breakthrough that is targeting cures for leukemia, AIDS, muscular dystrophy, hemophilia, and other conditions.

New products in this field are already generating substantial revenue and even more wondrous treatments are in the pipeline. Early investors could realize exceptional profits.

Click here to see the 5 stocks >>

• Trump’s trade war, U.S. jobs report, and last batch of Q4 earnings will be in focus this week. • Costco's earnings report is seen as a potential catalyst for growth, making it a...

Home improvement retailers Lowe’s (NYSE:LOW) and Home Depot (NYSE:HD) turned a corner, and their Q4 2024 earnings reports confirmed it. The corner is a return to comparable store...

One of our old flames, a former Contrarian Income Portfolio holding, has pulled back sharply in recent weeks. Time to buy the dip in this 4.3% dividend? Let’s discuss. Kinder...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.