Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Burlington Stores, Inc. (NYSE:BURL) delivered robust bottom-line results in fourth-quarter fiscal 2019. Earnings not only grew year over year but also outshined the Zacks Consensus Estimate for the third straight time. Although the top line lagged the consensus mark, the same improved year over year on impressive comparable store sales and solid contributions from new and non-comparable stores.

Notably, Burlington Stores is on track with its strategic initiatives. Management will now focus on higher investment in merchandizing capabilities, operating with leaner inventories, enhancing operational flexibility and controlling costs. In addition, the company has decided to wind down e-commerce operations, which represented nearly 0.5% of total sales. The decision will enable the off-price retailer to focus more and deploy resources in the bricks-and-mortar platform.

Let’s Introspect

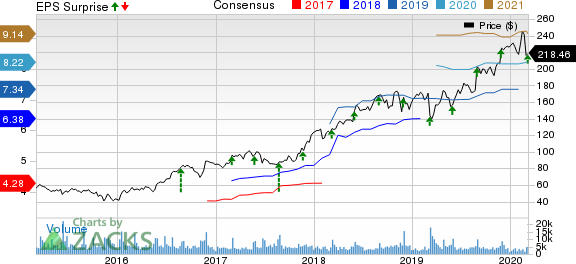

The company delivered fourth-quarter adjusted earnings (exclusive of management transition costs) of $3.25 per share that surpassed the Zacks Consensus Estimate of $3.22. Notably, earnings rose 14.8% from the prior-year quarter on higher net sales, merchandise margin improvement and leverage on SG&A.

Burlington Stores, Inc. Price, Consensus and EPS Surprise

Burlington Stores, Inc. price-consensus-eps-surprise-chart | Burlington Stores, Inc. Quote

Net sales advanced 10.5% year over year to $2,201.4 million. However, the reported figure lagged the consensus mark of $2,206 million, marking the second consecutive quarterly miss. New and non-comparable stores contributed $151 million to sales. Other revenues came in at $7.2 million, up 9.1% year over year.

Meanwhile, comparable store sales rose 3.9% in the reported quarter, up from an increase of 2.7% in the preceding quarter. Comps growth was mainly backed by rise in units per transactions with AUR and a marginal increase in conversions, somewhat offset by a slight fall in traffic. Notably, this was the 28th successive quarter of comparable store sales growth.

Gross margin grew 20 basis points (bps) to 42.1%, driven by an increase of 40 bps in merchandise margin, partly offset by higher freight costs.

Adjusted SG&A expenses, as a percentage of net sales, declined 20 basis points to 22.5% owing to sturdy sales growth that led to leveraged occupancy and marketing expenses, and corporate costs. This excludes management transition costs of $2.9 million incurred during the reported quarter.

Adjusted operating income (exclusive of management transition costs) improved 13.6% to $296.8 million, while adjusted operating margin, as a percentage of net sales, expanded 40 bps to 13.5%.

Over the past six months, shares of this Zacks Rank #2 (Buy) company have gained 8.2%, outperforming the industry’s 3.4% rise.

See 8 breakthrough stocks now>>

Using the Elliott Wave Principle (EWP), we have been tracking the most likely path forward for the Nasdaq 100 (NDX). Although there are many ways to navigate the markets and to...

Investors are on edge about what tariff policy means for markets Coming off a strong Q4 earnings season, fresh February corporate sales figures can help assess the macro...

Broadcom stock is in a dynamic rebound phase. Markets seem optimistic ahead of the earnings release. Let's take a deep dive into what to expect from the report. Get the...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.