Wednesday May 17: Five things the markets are talking about

If you thought last week was bad for President Trump this week is becoming even worse.

The U.S President now faces the deepest crisis of his presidency after a memo written by former FBI Director Comey surfaced yesterday. It alleges that Trump asked him to drop an investigation of former National Security Adviser Michael Flynn.

The possibility of obstruction by the Trump administration is weighing on market risk appetite, boosting the yen and gold and sending stocks lower.

The ‘mighty’ dollar has slipped to its lowest level in seven-months on fears that current controversies will make it more difficult for the White House administration to push through pledged tax cuts and infrastructure spending.

Yesterday’s weaker-than-expected housing data is also weighing on the dollar. April’s U.S new-home construction declined modestly for the third consecutive time in four-months.

1. Global indices see red

In Japan, stocks came under pressure after the dollar eased against the yen (¥112.43) on weak U.S economic data, while financial underperformed hit by lower U.S yields. The Nikkei shares average fell -0.5%, while the broader broader Topix also shed a similar -0.5%.

In Hong Kong, stocks ended lower, but continue to hover atop of their 21-mont highs. The Hang Seng index fell -0.2%, while the China Enterprises Index lost -0.5%.

In China, equities broke their four-day winning streak as regulatory concerns again linger. The blue-chip CSI 300 index fell -0.5%, while the Shanghai Composite Index lost -0.3%.

Note: Chinese stocks had declined for five consecutive weeks amid concerns that Beijing’s stepped-up efforts to reduce leverage would trigger liquidity stress and damage the economy.

In Europe, majority of indices remain on the back foot on Trump hearsay conversations. However, the FTSE 100 is outperforming as energy prices and air transport providing early support.

U.S stocks are set to open deep in the red (-0.5%).

Indices: Stoxx50 -0.2% at 3271, FTSE flat at 7523, DAX -0.4% at 12753, CAC 40 -0.5% at 5378, IBEX 35 -0.4% at 10937, FTSE MIB -0.6% at 21648, SMI -0.4% at 9088, S&P 500 Futures -0.5%

2. Oil dips on U.S inventory build, gold shines

Oil prices are on the back foot after industry data yesterday showed a surprise increase in U.S crude inventories despite OPEC-led output cuts that Saudi Arabia and Russia want extended.

Yesterday’s U.S API crude inventories rose by +882K in the week ending May 12 to +523m barrels, resisting expectations of a drop.

Brent crude is down -15c at +$51.50 per barrel, while U.S light crude (WTI) fell -26c to +$48.40.

Both benchmarks have rallied more than +$5 a barrel since hitting five-month lows last week.

Note: Data from the government’s Energy Information Agency, which is seen as more complete, is due this morning (10:30 am EST). Analysts are expecting another draw on inventories for the sixth consecutive week, falling -2.4m barrels.

Global inventories remain high, and the output from other producers, especially the U.S is rising, which is keeping prices below the psychological +$60 some OPEC members would like to see.

OPEC and non-OPEC countries meet to decide policy on May 25 in Vienna.

Ahead of the U.S open, gold prices have rallied for a fifth straight day, boosted by a weakening dollar. The spot price of gold has climbed +0.52% to +$1,243.5 a troy ounce.

3. U.S yields trade at the lower end of range

U.S. Treasury yields are under pressure after yesterday’s data showed that U.S homebuilding unexpectedly fell in April, adding to recent economic weakness that has raised new doubts over how many times the Fed will raise interest rates this year.

Last Friday’s disappointing U.S Retail Sales and CPI data has fixed income dealers trimming the odds for a Fed hike next month. Fed fund futures currently see a +68% chance of a hike, down from +83% pre-data release.

U.S. 10-Year Treasury yields have dipped to +2.29%, again flirting with its lowest level in two-weeks.

Note: U.S 10-year yields have largely held in a range between around +2.20% and +2.40% since late March as the market waits for clarity on whether the Trump administration is likely to pass tax and fiscal overhauls this year.

Elsewhere, benchmark yields in France lost -3 bps to +0.86%, while those in Germany declined -3 bps to +0.41%.

4. Diverging rate differential starting to take on a new effect.

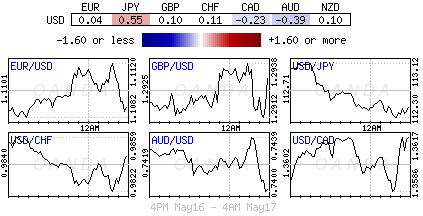

The USD remains in trouble, flirting with new post U.S Presidential lows on Trump political troubles and a recent spat of softer U.S economic data.

With the Eurozone beginning to see more positive data, conversations are starting the call for the ECB to think about normalizing its monetary policy. The ‘single’ unit hit an overnight high of €1.1117 and many analysts continue to see further upside for the EUR. As long as €1.1030 is not broken, a further rise to €1.1150 remains on the cards.

GBP (£1.2940) was little fazed by this morning’s April Claimant Count data that rose by over +19K. It has been unable to find the momentum to tackle the psychological £1.30 handle – fixed income dealers are pricing in a BoE unlikely to raise interest rates in 2017 or 2018. With the Fed on track to hike rates next month and the worries of tough Brexit negotiations with the E.U, sterling bears have their sights on a sub £1.28 in the short to medium-term.

Elsewhere, JPY (¥112.34) is firmer as risk aversion again creeps back into sentiment.

5. U.K unemployment at four-decade low, but real wages fall

Data this morning showed that U.K unemployment rate fell to a 40-year low in Q1 (-0.2% to +4.6%), but regular wages adjusted for inflation declined for the first time in three-years (-0.2%).

Note: U.K’s annual inflation stood at +2.7% in April – the fastest rate of price growth in over three-years, overshooting the BoE’s +2% target for the third consecutive month.

This data would suggest that ahead of Brexit negotiations Britons are facing a living standards squeeze despite the robust labor market and provide a potential drag on the U.K’s economic growth just as PM Theresa May goes to the polls in a general election on June 8.

Note: Polls are suggesting she is likely to increase her parliamentary majority, but individuals economic squeeze will help the Labour Party to shift focus from Brexit to individual’s living standards.