Tuesday May 29: Five things the markets are talking about

Threat of Euro fragmentation

US Treasuries have rallied alongside a number of core-European bonds as the political crisis in Italy and Spain deepens, triggering risk-off trading across capital markets.

The EUR ($1.1512) has tested fresh 11-month lows outright in early Euro trading after Italy’s president scuttled an attempt by a coalition of Italian anti-establishment parties to form a government. With fresh elections appearing increasingly likely, investors should expect the Five Star and the League to campaign on the idea that they were denied the “right to govern,” possibly resulting in a stronger populist sentiment at the next election. This would certainly pose risks to the European integration France and Germany are campaigning for.

Note: An Italian election would resemble a referendum, de facto, on the EU and the single unit.

Meanwhile in Spain, parliament is set to vote Friday (June 1) whether to oust Prime Minister Rajoy and replace his center-right government with one led by the center-left Socialist Party after a Spanish court ruled that Mr. Rajoy’s Popular Party financially benefited from an illegal kickback scheme.

On tap: US CB consumer confidence at 10 am EDT.

1. Global equities extend losses on geopolitical concerns

In Japan, stocks fell to one-month lows overnight, with investors selling cyclical shares as concerns over European politics added to the list of reasons to be cautious about the global economic outlook. The Nikkei average dropped -0.5%, the lowest close in four-weeks, while the broader Topix fell -0.48%.

Down-under, the Aussie shares ended higher on Tuesday, lifted by financials, though gains were capped by declines for consumer and telecom stocks. The S&P/ASX 200 index closed +0.2% higher. The benchmark declined -0.5% on Monday. In S. Korea, the KOSPI also came under pressure closing down -0.9%.

In Hong Kong, stocks ended lower, led by financials, as risk appetite was curbed by market volatility in Europe. The Hang Seng index ended -1% lower, while the Hang Seng China Enterprise (CEI) closed -1.3%.

In China, stocks posted a fifth consecutive session of losses overnight, as investors become concerned about credit risks amid more bond defaults. The blue-chip Shanghai Shenzhen CSI 300 index fell -0.8%, while the Shanghai Composite Index closed down -0.5%.

In Europe, regional bourses open down across the board and have continued the trend as the session progresses. Declines in benchmark US and German bond yields combined with continued uncertainty about regional politics is again put pressure on European bank shares.

US stocks are set to open deep in the ‘red’ (-0.7%).

Indices: Stoxx50 -1.8% at 3,424, FTSE -1.4% at 7,623, DAX -1.5% at 12,666, CAC 40 -1.6% at 5,421; IBEX 35 -2.2% at 9,543, FTSE MIB -2.4% at 21,423, SMI -1.2% at 8,669, S&P 500 Futures -0.7%

2. Oil prices pressure builds on expected crude output increase, gold lower

Oil prices remain under pressure from expectations that Saudi Arabia and Russia would pump more crude oil to ease a potential shortfall in supply.

Brent crude futures are up +21c, or +0.28% at +$75.51 a barrel, after settling at their lowest yesterday since May 8 at +$75.30. US West Texas Intermediate (WTI) crude is down -$1.11, or -1.64%, at +$66.77 a barrel, sitting around its lowest since April 17.

Note: The spread between Brent and WTI stands at around +$8.7 a barrel, the widest since March 2015 due to the depressed price of US crude compared to Brent.

Concerns that Saudi Arabia and Russia could boost output have put downward pressures on oil prices; along with rising oil production in the US.

Both parties have discussed raising OPEC and non-OPEC oil production by some +1m bpd to make up potential supply shortfalls from Venezuela and Iran. Critics don’t believe there is enough time to hammer out a deal before the next OPEC meeting.

Note: OPEC is due to meet in Vienna on June 22.

Ahead of the US open, gold prices have eased a tad as a stronger US dollar continues to weigh on the market amid renewed hopes of an US/North Korea summit. Spot gold is -0.1% lower at +$1,296.91 per ounce, while US gold futures for June delivery fell -0.6% to +$1,296.40 per ounce. Nevertheless, expect the yellow metal to find safe haven support on pullbacks.

3. G7 sovereign yields plummet on risk aversion

In coming back online after the Memorial Day weekend, US Treasury’s have found strong support amid geo-political uncertainty – Italy, Spain and N. Korea.

Italian government debt prices have slid hard since the country’s president scuttled an attempt on the weekend by a coalition of Italian anti-establishment parties to form a government after March’s elections.

The new possibility of fresh elections in the fall has sent the Italian 10-year government BTP bond yield higher, +2.865% from +2.36% early yesterday, while the interest-rate spread over similar German Bunds has widened above +250 bps, the highest in five-years, indicating a high level of market stress.

Elsewhere, yields on US 10-Year Treasury’s has edged down to +2.872% from +2.931% at the end of last week. In Germany, 10-year Bund yields have dipped -4 bps to +0.30%, hitting the lowest in more than five months with its fifth straight decline. While in the UK, the 10-year Gilt yield fell -6 bps to +1.321%, reaching the lowest in 20-weeks on its fifth straight decline.

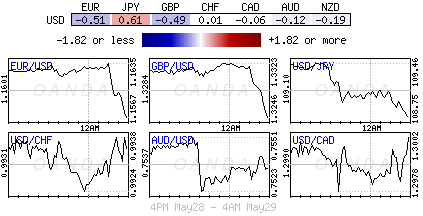

4. Euro drops to 10-month lows

Geopolitical uncertainties favor safe-haven flows – USD, CHF and JPY currencies in the overnight session. The USD Index is again trading atop of its seven-month highs.

EUR/USD has extended its losses, falling to a 11-month low of €1.1512 ahead of the US open. As noted above, the slide in the German Bund yield and the widening spread between Bunds and Italian BTP yields is likely to push the ‘single unit’ down further.

The yen currency is firmer with USD/JPY testing below ¥108.50 and EUR/JPY registering its largest decline in four-months as the cross tested the lower area of the €125.42 handle, down -1.1%.

Elsewhere, consumer confidence in Sweden has fallen below market expectations in May to 98.5 from 100.3 in April and has sent EUR/SEK up to a two-week high of €10.3401 and this despite the EUR being battered by Italian politics.

5. The Central Bank of Turkey pledges to simplify rates

Yesterday, Turkey’s central bank (CBoT) decided to complete the simplification of its monetary policy by setting the one-week repo rate as the policy rate, which will be equal to the current funding rate of +16.5%, in a move to support the TRY.

Note: TRY found immediate support, rising +2.5% outright at $4.5950

The central bank’s simplification process aims to adopt “a single rate to set policy instead of using multiple interest rates.”

CBoT’s overnight borrowing and lending rates will be determined at +150 bps below/above the one-week repo rate and the new operational framework will take effect on June 1.

Note: CBoT took emergency action last week, raising one of its interest rates by +300 bps, in a bid to stop TRY’s fall ahead of presidential and parliamentary elections next month.