The US dollar lost the most ground against the risk-linked Kiwi, Aussie, and Loonie yesterday and today in Asia, but equities traded more cautiously, though Wall Street’s S&P 500 and NASDAQ hit fresh records again. With no top-tier evens on the agenda yesterday, neither today, it seems that market participants may have become somewhat more careful ahead of the Jackson Hole economic Symposium, where Fed Chief Powell could provide (or not) clear signals on the Fed’s QE-tapering plans.

Risk-Linked Currencies Gain, But Equities Trade More Mixed Ahead Of Fed's Symposium

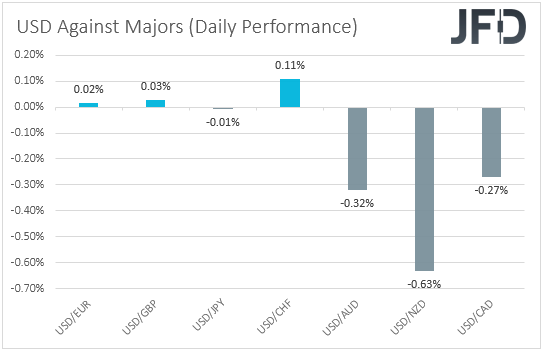

The US dollar traded lower or unchanged against all but one of the other major currencies. It gained only versus CHF, while it underperformed against NZD, AUD, and CAD in that order. The greenback was found virtually unchanged against JPY, EUR, and GBP.

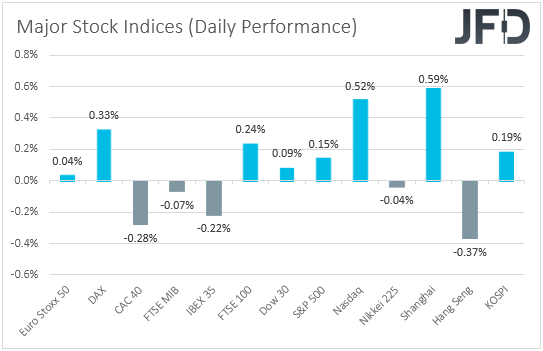

The weakening of the US dollar against its Australian, New Zealand, and Canadian counterparts suggests that markets may have continued trading in a risk-on fashion yesterday and today in Asia. That said, turning our gaze to the equity world, we see that major EU indices traded mixed, with Germany’s DAX being the main gainer, and France’s CAC 40 losing the most. Later, in the US, appetite was improved with both the S&P 500 and NASDAQ hitting fresh record highs for a second day in a row. Today though, in Asia, the optimism deteriorated somewhat again. Although China’s Shanghai Composite and South Korea’s KOSPI traded in the green, Japan’s Nikkei 225 and Hong Kong’s Hang Seng slid.

It seems that the news over the approval of Pfizer's (NYSE:PFE) vaccine by the FDA may have allowed some market participants to continue adding to their risk exposure, especially in the US, where more people may get encouraged to take the treatment after the approval. However, remember what we said yesterday. We said that heading into the Jackson Hole Economic Symposium, investors may become more cautious, as they are eager to find out what are the Fed’s plans with regards to monetary policy. Fed Chief Powell, who sounded dovish at the press conference following the latest FOMC gathering, is scheduled to speak on Friday, and, following the strong employment and inflation data, it would be interesting to see whether he has changed his mind to support an earlier QE tapering.

Up until last week, and especially following the minutes of the last meeting, which revealed that officials largely expect the process to begin this year, market participants may have added to their bets over a September action. However, on Friday, Dallas Fed President Robert Kaplan said he might reconsider his hawkish stance if the virus hurts the economy, while on Monday, data showed that business activity in the US slowed for a third straight month due to the virus spreading. This may have lessened confidence that Powell will provide a clear QE-tapering timeline. Therefore, with the outcome very uncertain, we believe that investors may maintain a cautious approach heading into the event.

As we noted yesterday, for the greenback to resume its recent uptrend, we believe that fresh signals over early tapering may be needed. If we don’t get them from Powell this week, traders may sell the dollar, but not massively, as they may keep an eye on the next employment report, scheduled for Sept. 3, where another set of strong numbers may add credence to the case of beginning the tapering process very soon.

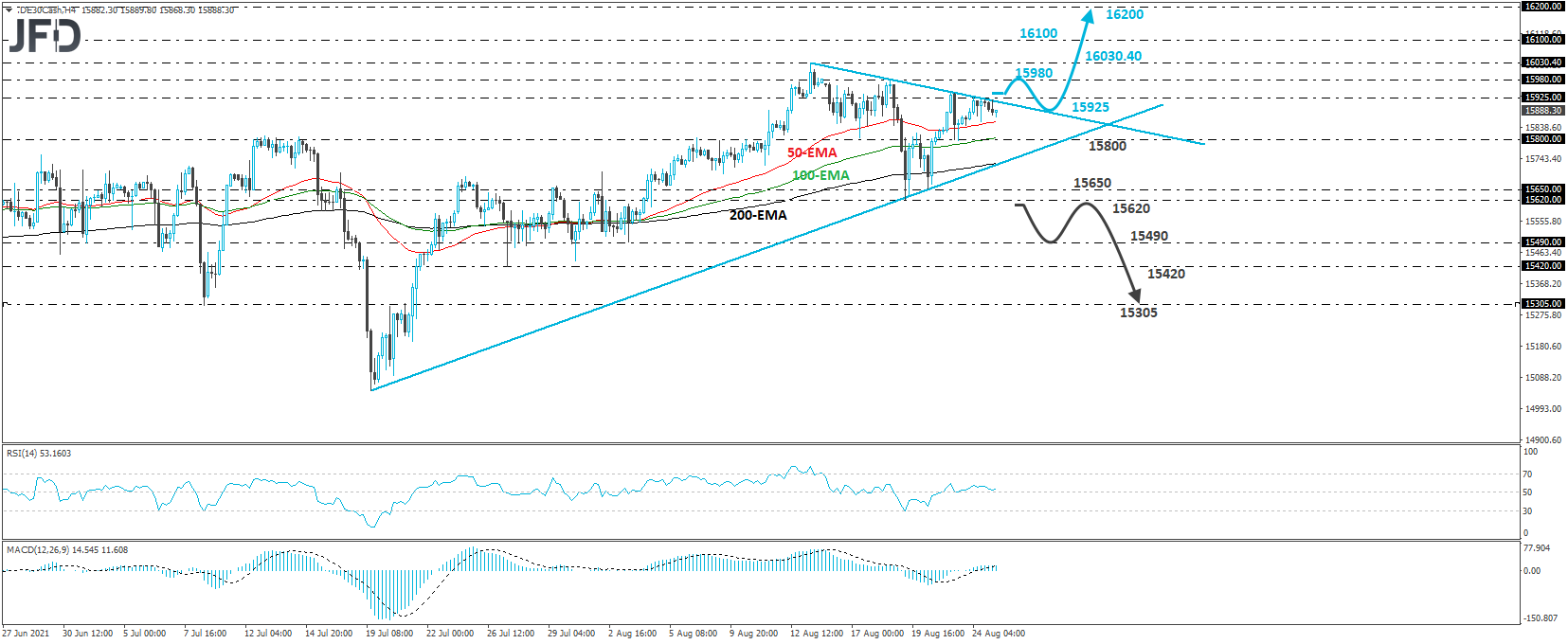

DAX Technical Outlook

The German DAX cash index traded higher yesterday, but the advance remained limited near the downside resistance line drawn from the high of Aug. 13, when the record of 16030.40 was hit. Overall though, the index continues to balance above the upside support line taken from the low of July 19, and thus, we would consider the near-term outlook to be cautiously positive.

If participants are strong enough to push the action above the aforementioned short-term downside line, and the 15925 barrier, we could initially see a test at 15980, the high of Aug. 18, or the record of 16030.40, hit on Aug. 13. If this time investors are not willing to stop there, a break higher could carry larger bullish implications, perhaps paving the way towards the round figure of 16100. Another break, above 16100 could set the stage for the 16200 zone.

On the downside, a dip below 15620 could signal a short-term reversal to the downside. The index would already be below the upside line drawn from the low of July 19, while the dip below 15620 would confirm a forthcoming lower low on both the 4-hour and daily charts. The bears may push the action towards the low of Aug. 3, at 15490, or the low of July 27, at 15420, where another break could see scope for extensions towards the 15305 zone, defined as a support by the low of July 8.

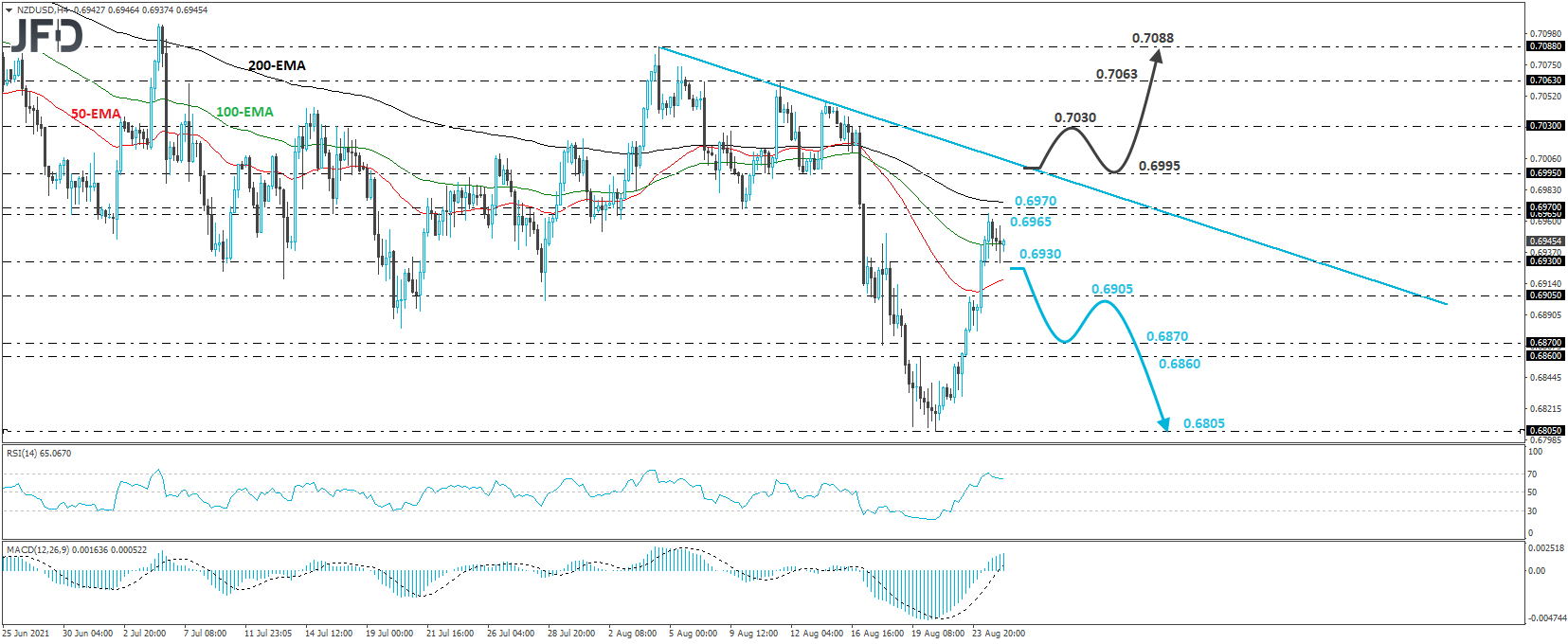

NZD/USD Technical Outlook

NZD/USD has been in a rally mode since Friday, when market appetite began to improve. However, yesterday, the pair hit resistance at 0.6965 and then it pulled back. Overall, the rate continues to trade below the downside resistance line taken from the high of Aug. 4, and thus, even if we see some further advance, we see decent chances for the bulls to meet strong resistance near that line.

In our view, a dip back below 0.6930 may be the first sign that the recent rally was just a correction that is now over. Initially we could see a test at 0.6905, the break of which could allow declines towards the 0.6870 or 0.6860 barriers, marked by the low of Aug. 18, and the inside swing high of Aug. 19 respectively. If neither barrier is able to stop the slide, then we may see the fall extending towards the low of Aug. 20, at 0.6805.

We will start getting more confident on the upside, if we see a break above the aforementioned downside line and the 0.6995 zone. This may encourage advances towards the 0.7030 area, the break of which could extend the gains towards the highs of Aug. 6 and 11, at around 0.7063. The next territory to consider as a resistance may be at 0.7088, defined by the high of Aug. 4.

As For Today's Events

The agenda is light today as well, with the only data worth mentioning being Germany’s Ifo survey for August, and the US durable goods orders for July. With regards to the Ifo numbers, the current assessment index is anticipated to have inched up to 100.8 from 100.4, but the expectations one is forecast to have slid to 100.0 from 101.2. This is likely to take the business climate index down to 100.4 from 100.8. As for the US durable goods, headline orders are forecast to have declined 0.2% mom after rising 0.9% in June, while the core rate is expected to have held steady at +0.5% mom.

As for the speakers, we will only get to hear from ECB Vice President Luis de Guindos.