The US Dollar slid and equities gained after Fed Chair Powell said that he and his colleagues remain open to increasing bond purchases if deemed necessary. As for today, the central bank torch will be passed to the SNB and the BoE, though we don’t expect any material changes from these Banks. Tonight, it will be the turn of the BoJ, which we don’t expect to act either.

Fed Keeps Policy Unchanged, But Stays Ready To Do More

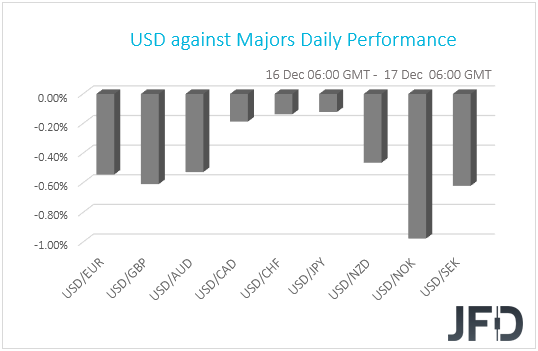

The US dollar continued sliding against the other G10 currencies on Wednesday and during the Asian session Thursday. It underperformed the most against NOK, SEK, GBP and EUR in that order, while it lost the least ground versus JPY and CHF.

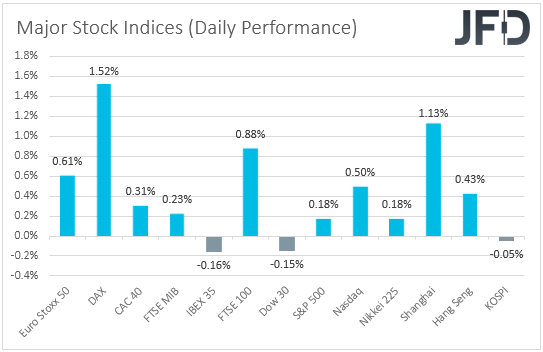

The weakening of the safe havens US dollar, Japanese yen and Swiss franc, suggests that markets continued trading in a risk on fashion yesterday. Indeed, turning our gaze to the equity world, we see that the majority of EU and US indices ended their trading in the green, with the only exceptions being Spain’s IBEX 35 and US’s Dow Jones, which slid 0.16% and 0.15% respectively. The upbeat morale rolled over into the Asian session as well. Although South Korea’s KOSPI fell 0.05%, Japan’s Nikkei 225 and China’s Shanghai Composite gained 0.18% and 1.13% respectively.

Yesterday, the main event on the economic agenda was the FOMC monetary policy decision. The Committee decided to keep its policy settings unchanged, but changed its forward guidance saying that they will continue to buy bonds “until substantial further progress has been made towards the Committee’s maximum employment and price stability goals.”

With regards to their new economic projections, they upgraded their GDP and inflation forecasts for 2021 and 2022, while they downgraded their unemployment rate ones for the whole forecast horizon. The new dot plot revealed that still, one member was in favor of raising interest rates in 2022, while five saw rates higher in 2023. In September, there were four members in favor of higher rates in 2023. With the inflation forecast of 2023 at 2%, this continues to suggest that some members may not be willing to tolerate above-target inflation for some time as noted in the statement.

The US dollar moved higher initially, and equities pulled back, perhaps in the absence of a policy change and/or the absence of strong hints that some sort of action may be in the works early next year. However, those moves were reversed, with the dollar resuming its slide and equities rebounding, during the press conference. Fed Chair Powell said that the recovery has been quicker than expected, but added that they remain open to increasing bond purchases or moving to longer maturities, and if they feel that this will help the economy, they will do it. These remarks may have been the reason behind the reversal in the market’s reaction, as they may have revived investors’ hopes that the Fed will do whatever it takes to support the world’s largest economy.

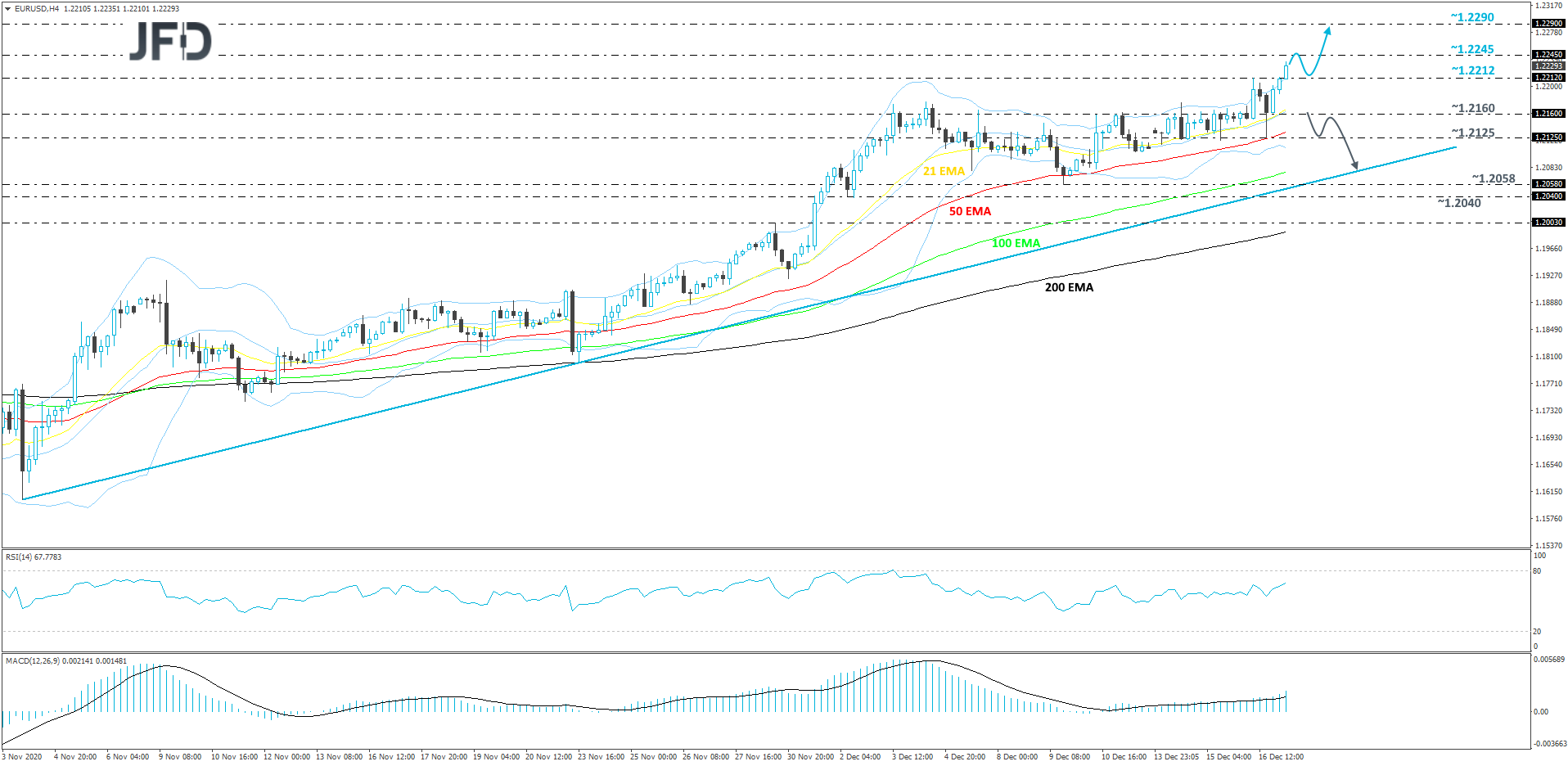

EUR/USD Technical Outlook

EUR/USD came under some buying interest in the first half of this week and it continues to be of interest for the bulls. This morning, the pair is seen climbing higher, breaking above some key resistance areas, one of which is yesterday’s high, at 1.2212. Also, the rate is trading well above its short-term tentative upside support line drawn from the low of Nov. 4. We will take a bullish approach, at least for now.

A further move north could bring the pair closer to the 1.2245 barrier, near the low of April 20 and the high of April 24 of 2018, which might temporarily halt the upmove. EUR/USD may even retrace back down a bit from there. That said, if the rate can stay somewhere above the previously discussed 1.2212 hurdle, that might attract the bulls back into the field. If this time EUR/USD can overcome the 1.2245 zone, the next possible resistance level could be at 1.2290, marked by the high of April 23, 2018.

Alternatively, a strong move back below the 1.2160 area, marked by the high of Dec. 10 and yesterday’s intraday swing low, may open the door for a larger correction to the downside. EUR/USD could then drift to the 1.2125 obstacle, a break of which might set the stage for a push towards the aforementioned upside line, which may provide support.

SNB, BoE And BoJ Take The Central Bank Torch

As for today, the central bank torch will be passed to the SNB and the BoE. Kicking off with the SNB, when they last met, policymakers of this Bank kept their policy untouched, reiterating that the Swiss franc is highly valued and that they remain ready to step up FX-market interventions when deemed necessary.

Since then, the Swiss franc has gained notably against the US dollar, but stayed relatively unchanged against the euro. In our view, bearing in mind that SNB pays more attention to the EUR/CHF exchange rate, officials are unlikely to strengthen their intervention language. We believe that they will keep their policy unchanged and that the statement will be more or less a repetition of the previous one.

Now passing the ball to the BoE, we don’t expect any action here either. At its prior gathering, the BoE decided to keep interest rates unchanged at 0.10%, but expanded its asset purchase program by more than initially expected. In the statement accompanying the decision, officials noted that the outlook for the economy remains unusually uncertain and that they stand ready to increase QE again if market functioning worsens.

Although officials of this Bank are ready to deliver more, we don’t expect this to happen now. Over the weekend, EU and UK Brexit negotiators agreed to extend talks over a potential trade agreement, something that increased hopes that an accord could eventually be reached. Therefore, we believe that the central bank will wait for the final outcome before deciding whether and how to act. A trade accord may allow policymakers to stay sidelined for a while more, while a no-deal Brexit may force them to cut rates into the negative territory for the first time in the Bank’s history.

For now, the pound is likely to stay sensitive to headlines surrounding the negotiations. Anything suggesting that the two sides are getting closer in sealing a trade accord could result in more positive waves, while reports hinting that the differences-gap is not narrowing could hurt the currency.

Tonight, during the Asia session Friday, another central bank decides on monetary policy, and this is the BoJ. No material change is expected from this Bank either and thus, the yen is unlikely to react. We believe that the safe-haven currency will stay mostly sensitive to developments surrounding the broader market sentiment. With the Fed committed to do more if deemed necessary, US lawmakers getting closer in passing a coronavirus-aid bill, and some vaccines already distributed in several countries, risk appetite may stay supported, something that will keep the safe-haven yen under selling interest.

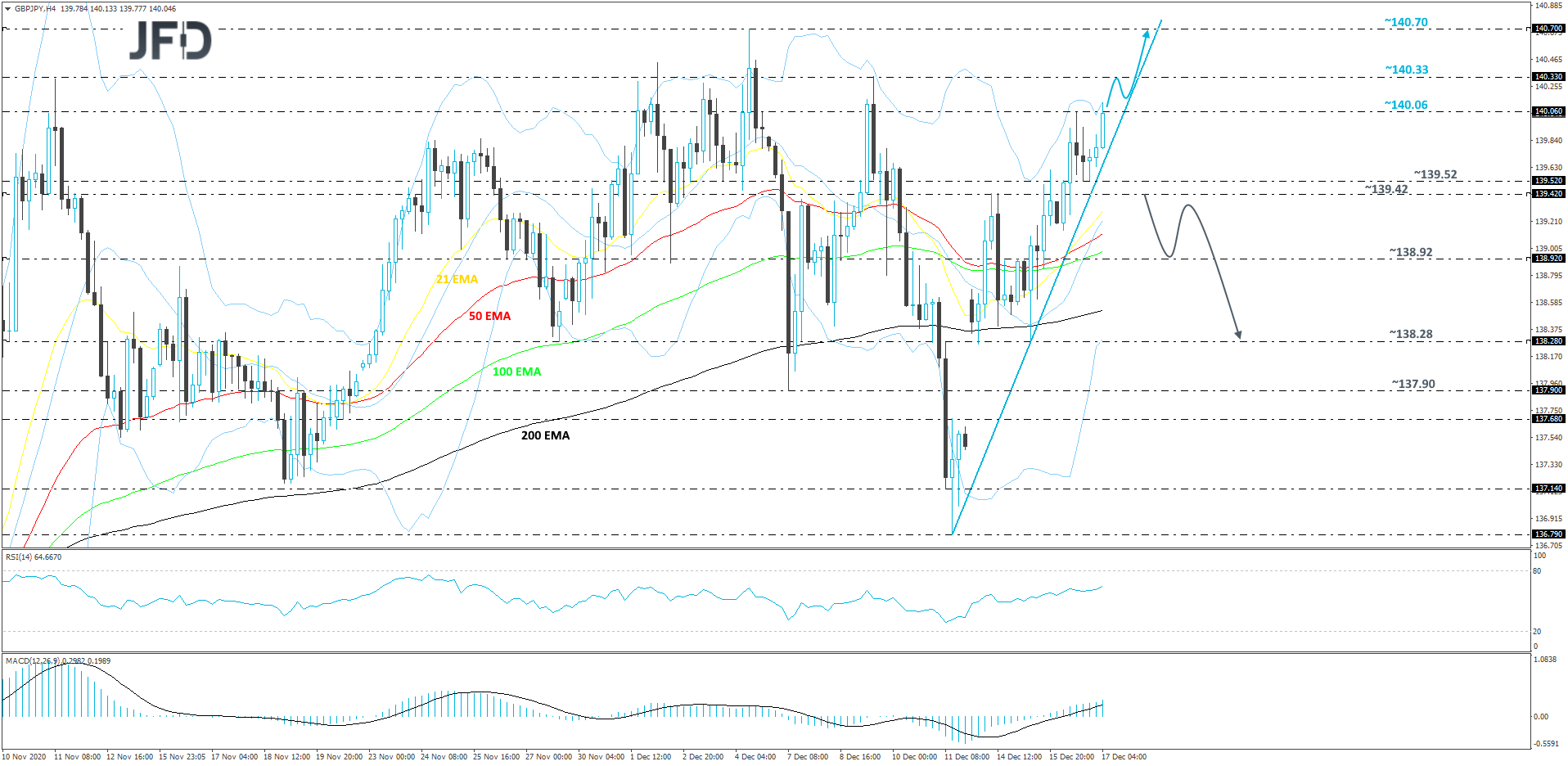

GBP/JPY Technical Outlook

GBP/JPY continues to rally, after gapping to the upside on Monday morning. The pair is trading above a steep short-term tentative upside line, marked by the low of Dec. 11. As long as that upside line remains intact, we will stay positive with the near-term outlook.

Another push above yesterday’s high, at 140.06, could invite more buyers into the game and lead the rate to its next potential resistance area, at 140.33, marked by the high of Dec. 9. The pair could get halted there for a bit, but if the buyers are feeling very comfortable still, they might lift GBP/JPY even higher, possibly bringing it the highest point of December, at 140.70.

On the downside, a break of the aforementioned upside line could make the bulls worry, as such a move might increase the pair’s chances of drifting lower. The buyers may start slowly abandoning the battlefield if GBP/JPY drops below the 139.42 area, marked by the high of Dec. 14. The pair may then slide to the 138.92 obstacle, a break of which could set the stage for a move to the 138.28 level, marked near the lows of Nov. 27, Dec. 14 and 15.

As For The Rest Of Today's Events

During the European session, we get Eurozone’s final CPIs for November, but as it is always the case, they are expected to confirm their preliminary estimates.

In the US, the building permits and housing starts for November are due to be released, as well as the initial jobless claims for last week. Building permits and housing starts are expected to have held relatively steady, while initial jobless claims are anticipated to have declined to 800k from 853k.

Tonight, during the Asian morning Friday, apart from the BoJ decision, we also have New Zealand’s trade balance for November, and Japan’s National CPIs for the same month.

As for the speakers, besides SNB President Jordan, who will hold a press conference after his Bank’s decision, we have three more speakers on today’s agenda. Those are BoE Deputy Governor Ben Broadbent, ECB Vice President Luis De Guindos and ECB Executive Board member Isabel Schnabel.