Most EU and US equity indices closed in the green yesterday as the vaccination progress around the world has been keeping investors interested in increasing their risk exposures on signs of several nations reopening their economies. That said, participants turned cautious during the Asian session today, perhaps as they await the outcome of the Fed meeting, which concludes tomorrow. Ahead of the decision, during the Asian session Wednesday, Australia’s CPIs for Q1 are due to be released.

EU And US Equities Rise, But Asians Slid As Fed Decision Looms

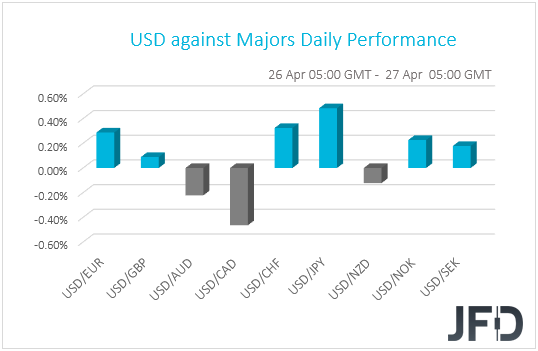

The US dollar traded higher against the majority of the other G10 currencies. It gained versus JPY, CHF, EUR, NOK, SEK, and GBP in that order, while it lost ground against CAD, AUD, and NZD.

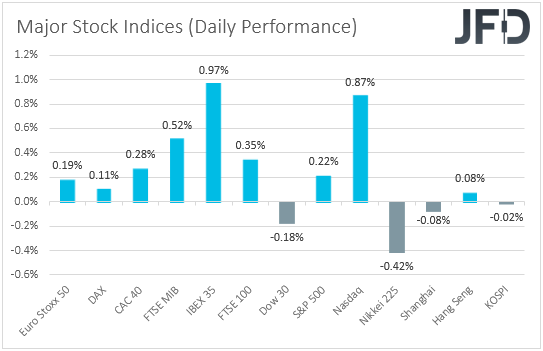

The strengthening of the commodity-linked Loonie, Aussie and Kiwi, combined with the weakness in the safe-havens yen and franc, suggests that markets traded in a risk-on fashion yesterday and today in Asia. Indeed, turning our gaze to the equity world, we see that major EU and US indices closed in the positive territory, with the only exception being the Dow Jones, which slid 0.18%. That said, risk appetite eased during the Asian session today, with both Japan’s Nikkei 225 and China’s Shanghai Composite sliding 0.42% and 0.08% respectively.

It seems that the vaccination progress around the world has been keeping investors interested in increasing their risk exposures on signs of several nations reopening their economies. The fact that several major central banks are willing to keep their monetary policy extra loose for long is also providing support to equity markets.

In the US, NASDAQ was the main gainer, fueled by a 1.3% advance in Tesla (NASDAQ:TSLA) on expectations that the company will report a rise in first-quarter revenue after the closing bell, something it did. The overall optimism faded during the Asian session today, perhaps as investors turned cautions ahead of the Fed’s two-day monetary policy meeting, which starts today.

Overall, we expect the Fed to maintain its dovish stance, with Fed Chief Powell repeating that any spikes in inflation this year are likely to prove to be temporary and that it is too early to start discussing policy normalization. Therefore, even if equities correct lower ahead of the decision, we expect them to rebound again in the aftermath and head for new record highs. Risk-linked currencies, like the Aussie and the Kiwi, may strengthen as well, while the US dollar and other safe havens, like the yen, are likely to come under renewed selling interest.

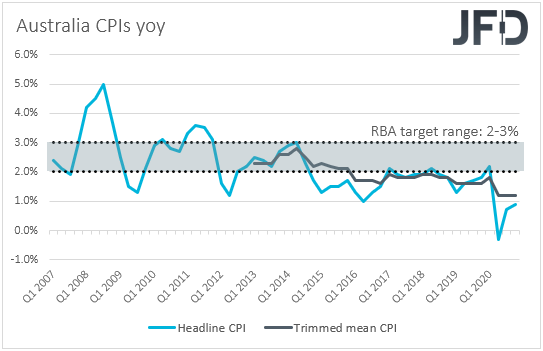

Ahead of the Fed decision, during the Asian morning Wednesday, we get Australia’s CPIs for Q1. The headline rate is forecast to have risen to +1.4% yoy from +0.9%, but the trimmed mean one is expected to have stayed unchanged at +1.2% yoy. Although RBA officials have been repeatedly noting that the economic recovery in Australia is well underway and stronger than previously expected, with both inflation rates staying well below the lower end of their 2-3% target range, we don’t believe that they will start thinking normalization any time soon.

That said, maintaining their optimism with regards to the economy and feeling content with the Aussie’s trading levels means that they are unlikely to ease policy further either. Thus, the faith of the risk-linked Aussie will probably depend more on developments surrounding the broader market sentiment, and perhaps any Chinese data, like the PMIs on Friday, as Australia has very close trading ties with the world’s second largest economy.

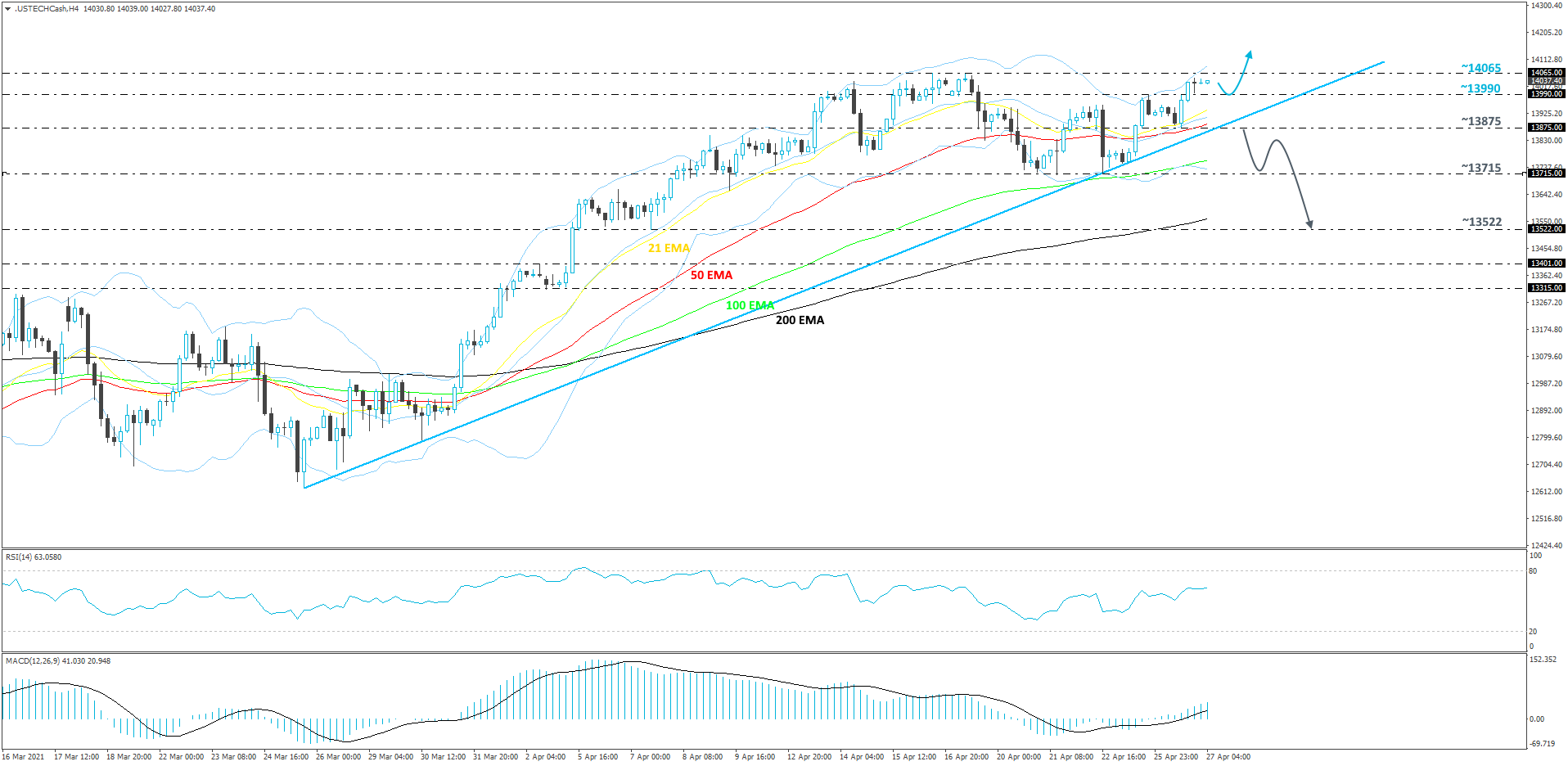

NASDAQ 100 Technical Outlook

After last week’s small correction lower, NASDAQ 100 made its way up again and got closer to its all-time, at 14065. This morning, the cash index continues to trade just slightly below that barrier. The price is also trading above a short-term upside support line taken from the low of Mar. 25. Even if the index corrects slightly lower, as long as that upside line stays intact, we will continue aiming higher.

If NASDAQ 100 struggles to overcome the current all-time high straight away, it may correct a bit lower, potentially dropping back somewhere to the 13990 zone, marked by the high of April 23rd. If that area is able to provide support, a reversal to the upside might occur, as the bulls might take advantage of the lower price and drive it north again. Another test of the resistance area near the previously-mentioned 14065 hurdle could eventually force it to surrender. If so, this would confirm a forthcoming higher high and place NASDAQ 100 into the uncharted territory.

Alternatively, if the index moves lower, breaks the aforementioned upside line and falls below the 13875 zone, marked by yesterday’s low, that could attract more sellers into the game, as such a move may lead to a change in the direction of the current short-term trend. NASDAQ 100 could then travel to the 13715 obstacle, a break of which would confirm a forthcoming lower low and set the stage for a push to the 13522 level, marked by the low of Apr. 7.

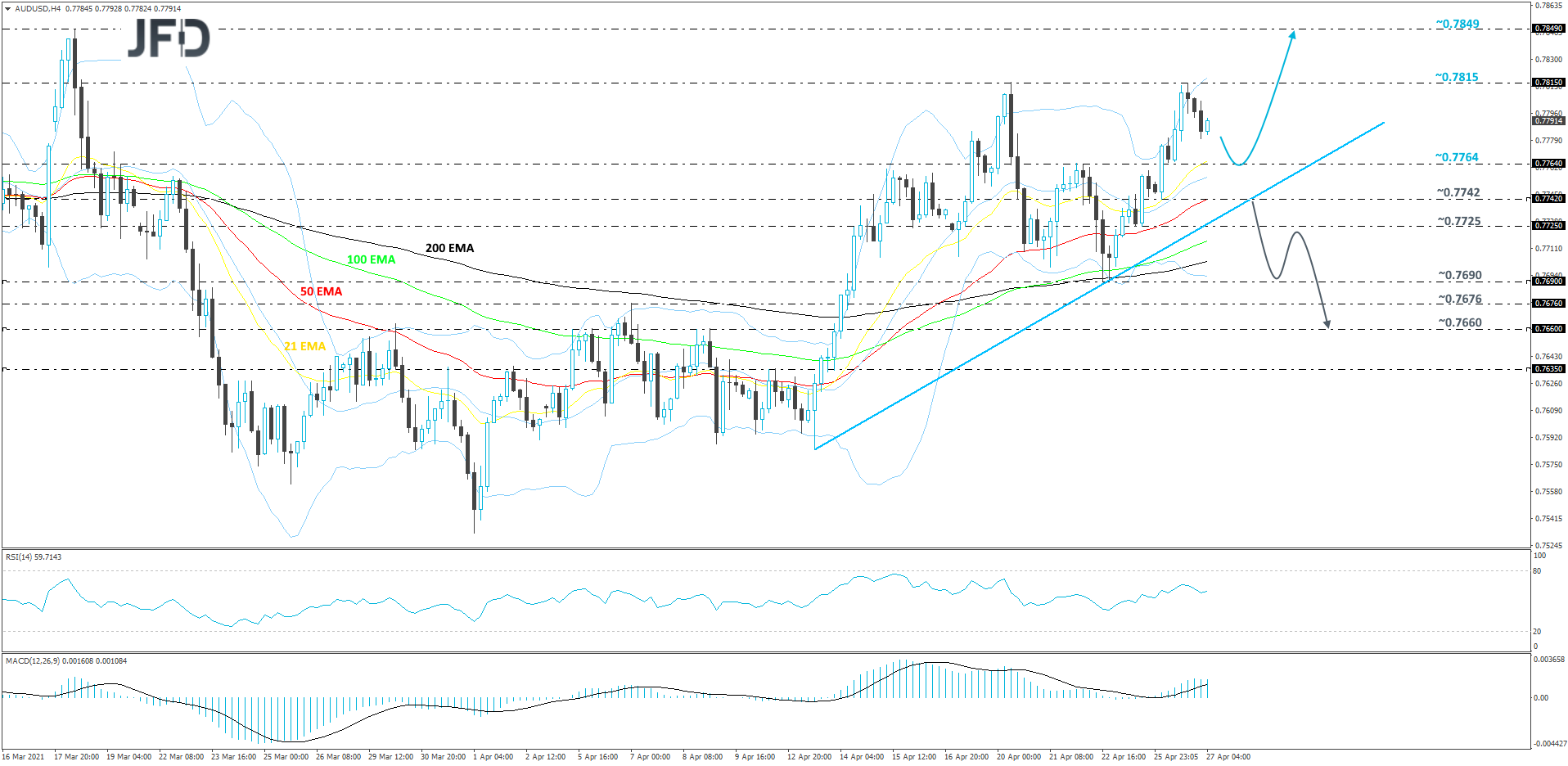

AUD/USD Technical Outlook

Once again, AUD/USD found strong resistance near the 0.7815 zone and corrected lower. So far, that area continues to hold throughout the whole month of April. At the same time, the pair is trading above a short-term tentative upside support line drawn from the low of Apr. 13. Even if the rate slides a bit more, as long as it stays above that upside line, we will continue aiming higher overall.

If the rate moves a bit lower and finds support near the 0.7764 hurdle, which is marked by the high of Apr. 22 and coincides with the 21 EMA, that could invite the buyers back into the game and send the pair north again. We will then target the previously discussed 0.7815 barrier, which if gets broken, would confirm a forthcoming higher high, potentially opening the door for further advances. Our next target then could be the 0.7849 level, marked by the highest point of March.

On the other hand, if the aforementioned upside line fails to hold and the rate also drops below the 0.7742 hurdle, marked by the low of Apr. 26, that could spook the remaining buyers from the arena temporarily. AUD/USD might drift to the 0.7725 obstacle, or to the low of last week, at 0.7690, where a temporary hold-up may occur. If the bears are still feeling comfortable, they could easily push the pair further south, potentially targeting the 0.7676 obstacle, or the 0.7660 level, marked by the highs of Apr. 8 and 9.

As For Today's Events

During the Asian session today, we already got a BoJ decision, but the outcome was broadly as expected. The Bank kept its policy settings unchanged, revising up its growth forecasts, but downgrading its inflation ones. Given that this was the base case scenario, the yen and Japanese equities did not react on the decision.

Later in the day, the only releases worth mentioning are the US Conference Board consumer confidence index for April and the API (American Petroleum Institute) report on crude oil inventories for last week. The CB index is expected to have risen to 113.0 from 109.7, while, as it is always the case, no forecast is available for the API report.

As for the speakers, we have only one on today’s agenda and this is BoC Governor Tiff Macklem.