Wednesday May 3: Five things the markets are talking about

The Fed is widely expected to keep interest rates unchanged today with the focus on language for its next move in June.

The market risk is the central bank adopting a more-cautious description of U.S economic performance amidst recent data. If Ms. Yellen and company happen to do so, it will put renewed pressure on the ‘mighty’ dollar and on U.S rates.

Currently, investors are pricing a less than +5% chance of a rate rise today; instead, they will be looking for any hints at a rate increase next month.

Fed Fund futures are pricing in a +66% chance of a hike in June. The current state of affairs suggests that the Fed does not need to work as hard to manage those expectations as they had to in early Q1. U.S policy makers have two more employment reports, including this Friday’s, ahead of that decision.

In France, Emmanuel Macron and the far right’s Marine Le Pen, go head-to-head today in a televised French Presidential election debate. Opinion polls still show Macron holding a strong lead of +20 points over the National Front’s Le Pen with just four days to go to the final vote.

1. Equities react negatively to earnings

Declines in materials shares and disappointing earnings news, particularly from Apple (NASDAQ:AAPL), have sent global stocks lower overnight ahead of today’s update from the Fed.

Note: Markets in Japan, South Korea and Hong Kong were closed for holidays.

Down-under, financials have dragged down Aussie bourses for a second consecutive session with the S&P ASX 200 off -1%.

In China, equities were mostly weaker as investors sold stocks related to the designated economic zone. The Shanghai Composite Index was down -0.3%.

In Europe, indices trade slightly lower across the board as U.S earnings again weighed on investor sentiment. Energy and commodity shares are supporting the FTSE ahead of the U.S open.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.1% at 3573, FTSE -0.3% at 7226, DAX -0.2% at 12481, CAC 40 -0.3% at 5287, IBEX 35 -0.1% at 10810, FTSE MIB -0.2% at 20689, SMI 0.0% at 8873, S&P 500 Futures -0.2%

2. Oil rebounds from yearly lows, gold lower

Oil prices have rebounded from yesterday’s fresh yearly lows after preliminary data yesterday showed a much higher-than-expected fall in U.S crude stocks.

Ahead of the U.S open, Brent crude futures are up +37c at +$50.83 a barrel, while U.S West Texas Intermediate (WTI) crude is at +$47.96 a barrel, up +30c from yesterday’s close.

WTI had slid -2.4% yesterday on concerns about falling OPEC compliance with its production-curbing deal.

Yesterday’s API data revealed that crude stocks had fallen last week by -4.2m, nearly double the drop expected by the market.

Note: The U.S government will release ‘official’ inventory data from the EIA at 2:30 pm EST.

Gold prices are holding atop of their three-week low hit Tuesday on rising equities and a firmer dollar. The markets are waiting for cues on a U.S interest rate hike from the Fed. Yesterday, the yellow metal hit a low of +$1,251.37 per ounce, its worst level since April 10.

3. Global yields to take directions from the Fed

U.S. 10-Year yields have edged down a touch to +2.29% from +2.30% overnight ahead of today’s Fed meeting.

Note: The U.S Treasury releases its quarterly refunding plans for issuance of longer-term debt – this will get more attention than usual after Treasury Secretary Mnuchin flagged potential interest in selling bonds with maturities beyond 30 years. If so, it should steepen up the U.S curve.

Elsewhere, France 10-Year yields (OAT’s) have edged lower to +0.740% while German Bund yields have fallen to +0.31% ahead of a today’s televised debate between Macron and Le Pen. Earlier this morning, Germany sold €2.4B 10-Year Bunds at an average yield of +0.33% vs. +0.21% on April 12 with a bid-to-cover ratio of +1.5 vs. +1.4.

Down-under, the yield on Aussie debt with a similar maturity dropped -1 bps to +2.59%.

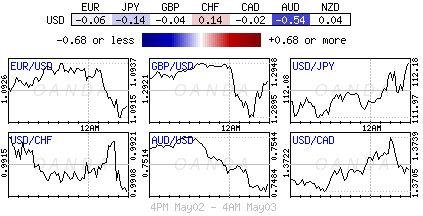

4. Dollar firms ahead of Fed decision

The dollar is finding some support ahead of the Fed decision. Markets will be looking for clues about the timing of the next hike, and how and when, the Fed will shrink its balance sheet.

The EUR is down -0.15% at €1.0911, while the pound is down -0.1% at £1.2925.

Note: Any weakness in this morning’s ADP payrolls data, or a less “hawkish” tone from the Fed could help push both currency pairs towards their medium term targets of €1.1000 and £1.3000 respectively. However, if far-right French Presidential candidate Le Pen does well in today’s debate expect the Eurozone’s single unit to come under immediate pressure.

USD/JPY up +0.2% at ¥112.21.

5. Eurozone grew in Q1

Data this morning showed that the combined GDP of the 19-member Eurozone was +0.5% higher than in the final three months of 2016, and +1.7% higher than in the first quarter of that year.

That is the equivalent to an annualized growth rate of +1.8%, stronger than the +0.7% expansion recorded by the U.S and the +1.2% expansion recorded by the U.K in the same period.