Last week, the S&P 500 put an end to its streak of weekly losses, despite giving back some gains on Friday. Thursday provided the big catalyst, with the ECB’s announcement of its bold new monetary stimulus plan. Investors were cheered and soothed for the moment. And U.S. fundamentals still look strong. But with Greece trying to turn back time, with volatility elevated (and likely to continue as such), and with the technical situation still dicey, the near term outlook is still worrisome.

In this weekly update, I give my view of the current market environment, offer a technical analysis of the S&P 500 chart, review our weekly fundamentals-based SectorCast rankings of the ten U.S. business sectors, and then offer up some actionable trading ideas, including a sector rotation strategy using ETFs and an enhanced version using top-ranked stocks from the top-ranked sectors.

Market overview:

Despite the positive turn in the markets last week, this week has already brought a whole new set of issues to weigh on investors’ minds, starting with Sunday’s snap vote in Greece, which apparently has enough of the pain of austerity. Voters want to return to the past by rolling back austerity measures and thumbing their collective nose at the Eurozone and the broader international community of lenders. In reaction, the euro fell even further than it did in the face of the ECB’s stimulus announcement last week.

The ECB seeks to inflate asset prices and encourage hiring through an open-ended sovereign quantitative easing program that will inject 60 billion euros into European debt securities each month from March 2015 until at least September 2016. Heck, if it helped the U.S. recover, then why not try it everywhere? ECB President Mario Draghi, insisted that stimulus must be accompanied by reforms, because monetary policy alone will not be enough. But Europe still pines for the good old days that, unfortunately, are nothing more than nostalgia.

There is a very real danger that their QE won’t work like it did here, since the U.S. is considered the heart of the global economy and weakness here means weakness everywhere. Without structural reforms, the Eurozone could suffer the same fate as emerging markets in the 1990s. Global investors would love to see economic recovery and strength in European equities. But without an expectation of real economic growth, companies will simply use the enhanced liquidity to pay down debts rather than invest in the future. So for now, the asset classes of choice are distinctly 1990s-esque, i.e., long the U.S. dollar, long higher-quality U.S. equities, and long volatility.

The CBOE Market Volatility Index VIX), a.k.a. fear gauge, closed Friday at 16.66, which is back below the important 20 threshold that suggests real fear, but still above the 15 level that indicates complacency. Whereas last year each spike in volatility quickly dissipated, we’ve seen it linger on the higher end of the spectrum so far this year.

Sabrient’s annual Baker’s Dozen portfolio of 13 top picks finished its sixth straight strong year (since 2009 inception), and this year is already off to a rousing start. Baker’s Dozen represents a sector-diversified group of 13 stocks based on our Growth at a Reasonable Price (GARP) quant model, which was created by our founder and chief market strategist David Brown (who long ago worked for NASA on the lunar landing project). The list is further vetted and confirmed through a rigorous forensic accounting review by our subsidiary Gradient Analytics to help us avoid stocks with elevated risk of accounting-related blow-ups.

Also, many of the investment professionals who have embraced the Baker’s Dozen have asked for access to some of our institutional-level research but at a more affordable price. In response, we have launched a web-based suite of research products geared to investment professionals. In fact, I always employ the ETF Summaries section of the product suite when writing this weekly article to identify highly ranked stocks from the strongest sector ETFs when providing stock ideas for an enhanced sector rotation strategy.

SPY chart review:

The SPDR S&P 500 Trust (SPY) closed last Friday at 204.97. It bounced quite nicely from support at the 100-day simple moving average and the lower trend line of the long-standing bullish rising channel, and now it sits right in the middle of the channel, resting precariously on its 50-day SMA. Oscillators RSI and MACD are still in neutral territory and Slow Stochastic has quickly risen from oversold to near overbought territory. The bearish head-and-shoulders pattern that was apparently forming, with a head around 209 and a neckline at the lower trend line, is possibly still in play, although price is trying to nullify it. We’ll see how investors react to the latest news, as well as the FOMC meeting this week. If current support at the 50-day fails again, the 100-day is at 201, the lower trend line is at 200, and the important 200-day SMA near is near 197. Below that is a prior price gap at 190. However, if instead price rallies from here, overhead resistance will come from the previous highs near 209, and then the upper trend line that has now risen above 212.

Latest sector rankings:

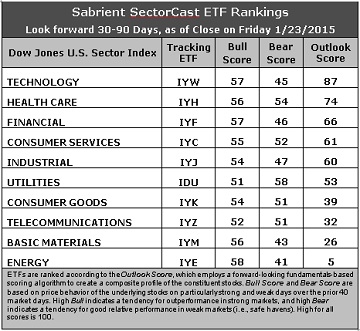

Relative sector rankings are based on our proprietary SectorCast model, which builds a composite profile of each equity ETF based on bottom-up aggregate scoring of the constituent stocks. The Outlook Score employs a forward-looking, fundamentals-based multifactor algorithm considering forward valuation, historical and projected earnings growth, the dynamics of Wall Street analysts’ consensus earnings estimates and recent revisions (up or down), quality and sustainability of reported earnings (forensic accounting), and various return ratios. It helps us predict relative performance over the next 1-3 months.

In addition, SectorCast computes a Bull Score and Bear Score for each ETF based on recent price behavior of the constituent stocks on particularly strong and weak market days. High Bull score indicates that stocks within the ETF recently have tended toward relative outperformance when the market is strong, while a high Bear score indicates that stocks within the ETF have tended to hold up relatively well (i.e., safe havens) when the market is weak.

Outlook score is forward-looking while Bull and Bear are backward-looking. As a group, these three scores can be helpful for positioning a portfolio for a given set of anticipated market conditions. Of course, each ETF holds a unique portfolio of stocks and position weights, so the sectors represented will score differently depending upon which set of ETFs is used. We use the iShares that represent the ten major U.S. business sectors: Financial (iShares US Financials (NYSE:IYF)), Technology (iShares Dow Jones US Technology (NYSE:IYW)), Industrial (IYJ), Healthcare (iShares US Healthcare (NYSE:IYH)), Consumer Goods (iShares US Consumer Goods (NYSE:IYK)), Consumer Services (iShares US Consumer Services (NYSE:IYC)), Energy (iShares DJ US Energy Sector Fund (NYSE:IYE)), Basic Materials (iShares US Basic Materials (NYSE:IYM)), Telecommunications (iShares US Telecommunications (NYSE:IYZ)), and Utilities (iShares US Utilities (NYSE:IDU)). Whereas the Select Sector SPDRs only contain stocks from the S&P 500, I prefer the iShares for their larger universe and broader diversity. Fidelity also offers a group of sector ETFs with an even larger number of constituents in each.

Here are some of my observations on this week’s scores:

1. All sectors continue to get hit with net downward revisions to forward earnings estimates by Wall Street sell-side research analysts. Nevertheless, Technology continues to rank first with an Outlook score of 87. It displays the best return ratios, a good forward long-term growth rate and forward P/E, and relatively good sell-side analyst sentiment (only slight downward revisions to earnings estimates). Healthcare holds second place with a score of 74, displaying a solid forward long-term growth rate, relatively good sell-side analyst sentiment (only slight downward revisions), reasonably good insider sentiment (buying activity), and good return ratios. Financial is still in third place with a 66, followed by Consumer Services/Discretionary and Industrial. All in all, it’s a bullish top five.

2. Energy continues to hold the bottom spot given the plunge in oil prices. Its Outlook score is an anemic 5. Joining Energy in the bottom two again is Basic Materials, as these two sectors continue to endure Wall Street’s downward revisions to forward earnings estimates and also display the weakest insider sentiment.

3. Looking at the Bull scores, Energy displays the top score of 58, followed closely by Technology and Financial. Utilities scores the lowest at 51. However, the top-bottom spread is only 7 points, which is quite low and reflects extremely high sector correlations during particularly strong market days, i.e., highly-correlated risk-on action. It is generally desirable in a healthy market to see low correlations and a top-bottom spread of at least 20 points, which indicates that investors have clear preferences in the stocks they want to hold, rather than the all-boats-lifted-in-a-rising-tide (risk-on) mentality.

4. Looking at the Bear scores, Utilities displays the highest score of 58 this week, which means that stocks within this sector have been the preferred safe havens on weak market days. Energy has the lowest score of 41. The top-bottom spread is 17 points, reflecting fairly low sector correlations on particularly weak market days. In other words, certain sectors are holding up relatively well while others are selling off. Again, it is generally desirable in a healthy market to see low correlations and a top-bottom spread of at least 20 points.

5. Technology displays the best all-around combination of Outlook/Bull/Bear scores, while Energy is clearly the worst. Looking at just the Bull/Bear combination, Healthcare is the leader, followed closely by Utilities, indicating superior relative performance (on average) in extreme market conditions (whether bullish or bearish). Energy and Basic Materials are the worst, indicating general investor avoidance.

6. Overall, this week’s fundamentals-based Outlook rankings still look bullish to me, with the top five sectors all economically-sensitive and growth-oriented (or in the case of Healthcare, all-weather). Moreover, all five have Outlook scores of 60 or greater. Keep in mind, the Outlook Rank does not include timing or momentum factors, but rather is a reflection of the fundamental expectations of individual stocks aggregated by sector.

Stock and ETF Ideas:

Our Sector Rotation model, which appropriately weights Outlook, Bull, and Bear scores in accordance with the overall market’s prevailing trend (bullish, neutral, or defensive), is sticking with a neutral bias, even though SPY has regained and is still holding support (barely) at its 50-day simple moving average, and the model suggests holding Technology, Healthcare, and Financial, in that order. (Note: In this model, we consider the bias to be neutral from a rules-based trend-following standpoint when SPY is between its 50-day and 200-day simple moving averages.) If the 50-day holds support over the next couple of days, the bias would move back to bullish.

Other highly-ranked ETFs from the Technology, Healthcare, and Financial sectors include PowerShares Dynamic Semiconductors Portfolio (PSI), iShares NASDAQ Biotechnology ETF (IBB), and PowerShares KBW Insurance Portfolio (KBWI).

For an enhanced sector portfolio that enlists some top-ranked stocks (instead of ETFs) from within the top-ranked sectors, some long ideas from Technology, Healthcare, and Financial sectors include Spansion (CODE), Ambarella (AMBA), Pharmacyclics (PCYC), Incyte (INCY), PrivateBancorp (PVTB), and Simon Property Group (SPG). All are highly ranked in the Sabrient Ratings Algorithm and also score within the top two quintiles (lowest accounting-related risk) of our Earnings Quality Rank (a.k.a., EQR), a pure accounting-based risk assessment signal based on the forensic accounting expertise of our subsidiary Gradient Analytics. We have found EQR quite valuable for helping to avoid performance-offsetting meltdowns in our model portfolios.

However, if you prefer to maintain a bullish bias, the Sector Rotation model suggests holding Technology, Financial, and Healthcare, in that order. And if you prefer a defensive stance on the market, the model suggests holding Utilities, Healthcare, and Consumer Services/Discretionary, in that order.

Note that Fidelity offers its own line of U.S. sector ETFs that can be used for sector rotation, including Fidelity MSCI Information Technology Index ETF (FTEC), Fidelity MSCI Health Care Index (FHLC), Fidelity MSCI Consumer Discretionary Index ETF (FDIS), Fidelity MSCI Utilities Index ETF (FUTY), and Fidelity MSCI Financial Index ETF (FNCL).

IMPORTANT NOTE: I post this information each week as a free look inside some of our institutional research and as a source of some trading ideas for your own further investigation. It is not intended to be traded directly as a rules-based strategy in a real money portfolio. I am simply showing what a sector rotation model might suggest if a given portfolio was due for a rebalance, and I may or may not update the information each week. There are many ways for a client to trade such a strategy, including monthly or quarterly rebalancing, perhaps with interim adjustments to the bullish/neutral/defensive bias when warranted -- but not necessarily on the days that I happen to post this weekly article. The enhanced strategy seeks higher returns by employing individual stocks (or stock options) that are also highly ranked, but this introduces greater risks and volatility. I do not track performance of the ETF and stock ideas mentioned here as a managed portfolio.

Disclosure: Author has no positions in stocks or ETFs mentioned.

Disclaimer: This newsletter is published solely for informational purposes and is not to be construed as advice or a recommendation to specific individuals. Individuals should take into account their personal financial circumstances in acting on any rankings or stock selections provided by Sabrient. Sabrient makes no representations that the techniques used in its rankings or selections will result in or guarantee profits in trading. Trading involves risk, including possible loss of principal and other losses, and past performance is no indication of future results.