We don't have any central bank meetings on this week's calendar. Still, we will hear from several central bankers, including Fed Chair Jerome Powell, European Central Bank (ECB) President Christine Lagarde, and Bank of England (BoE) Governor Andrew Bailey. Therefore, it will be interesting to see whether we get any new information regarding monetary policy.

On top of that, market participants are likely to stay focused on developments surrounding the Evergrande (OTC:EGRNY) saga, as the firm missed a payment on offshore bonds last week, and more payments are due this week.

On Monday, the first piece of news in the morning was that Germany's Social Democrats narrowly won Sunday's national elections, claiming a "clear mandate" to lead a government for the first time since 2005.

However, with neither major party securing a majority and both reluctant to repeat their "grand coalition," it may take weeks or even months to form a coalition government. Perhaps, that's why the Euro opened the week in a quiet mode.

As for today's data, the only worth mentioning is the US durable goods orders for August. Headline orders are forecast to have rebounded 0.7% mom after sliding 0.1%, but the core rate is expected to have declined to +0.5% mom from +0.8%.

Despite not having top-tier data on Monday's agenda, we will get to hear from ECB President Christine Lagarde ahead of the ECB's Forum on Central Banking. Starting tomorrow, we will also get speeches from Fed Chief Jerome Powell, BoE Governor Andrew Bailey, and Bank of Japan (BoJ) Governor Haruhiko Kuroda.

Other policymakers are also due to speak throughout the week. Therefore, we will pay extra attention to their remarks, as they could provide additional clues and hints regarding monetary policy.

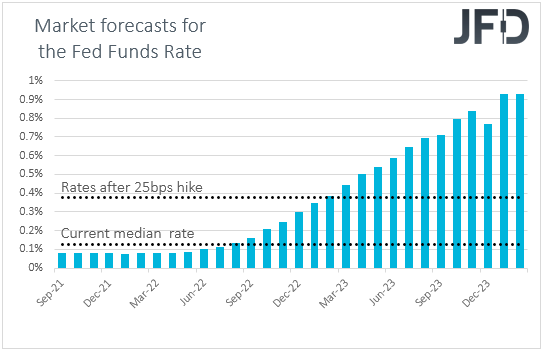

Last week, the Fed confirmed that quantitative easing (QE) tapering is likely to start this year, with investors hoping that this will happen as early as November. Thus, remarks adding credence to that view may result in further US Dollar Index buying.

Meanwhile, in the UK, the BoE appeared more hawkish than expected, encouraging participants to bring forth their rate-hike expectations. It would be interesting to see whether we get any hints on when the first hike may occur.

Officials of the ECB announced a "moderately lower pace" in its Pandemic Emergency Purchase Program (PEPP) purchases. Still, they made it clear that this is not a tapering move and that when PEPP is over, they have all the other tools available. With that in mind, we look for any comments as to whether the bank intends to compensate by buying more through different schemes, like the Asset Purchase Program (APP).

There is not much to anticipate as far as the Bank of Japan (BoJ) is concerned. Japanese policymakers have been stuck with extra loose monetary policy, showing no intention to proceed with any changes any time soon.

On Tuesday, besides speaking at the ECB's forum, Fed Chair Jerome Powell will testify before Congress on the central bank's policy response to the pandemic. He will speak before the Senate Banking Committee on Tuesday, while he will present the same testimony before the House Financial Services Committee on Wednesday.

As we already noted, we will be looking for clear clues as to whether November is the better choice for the Fed to start scaling back its QE purchases. With Powell speaking several times this week and various other officials scheduled to step up to the rostrum this week, the chances of getting some new information may be decent.

As for Tuesday's data, we have the Conference Board Consumer Confidence Index for September, which is expected to have risen to 114.5 from 113.8.

On Wednesday, the main event may be the leadership elections of Japan's ruling Liberal Democratic Party (LDP). The winner will succeed Yoshihide Suga as a Prime Minister. He may not hold that position for long as national elections will occur on or before Nov. 28. Taro Kono appears to be the favorite, a candidate that supports a spending package that focuses on boosting wages and growth.

However, we don't expect Japanese markets to react massively to the outcome. Remember that in the days after Suga's announcement that he will step down, Japan's Nikkei 225 surged almost 12%, suggesting that investors have already cheered the prospect of better days with a new Prime Minister.

As for the rest of Wednesday's events, we do have Germany's retail sales for August and the US pending home sales for the same month. On Thursday, during the Asian session, Japan's primary industrial production and retail sales, both for August, are coming out. Industrial production is expected to slide again, but at a slower pace than in July. While retail sales are forecast to fall, 1.0% mom, after rising 2.4% the month before.

China's official PMIs for September are due to be released. We have a forecast for the manufacturing index, which could climb to to 50.2 from 50.1. Even if the data come in stronger than expected, we believe that market participants will stay more focused on the Evergrande saga developments.

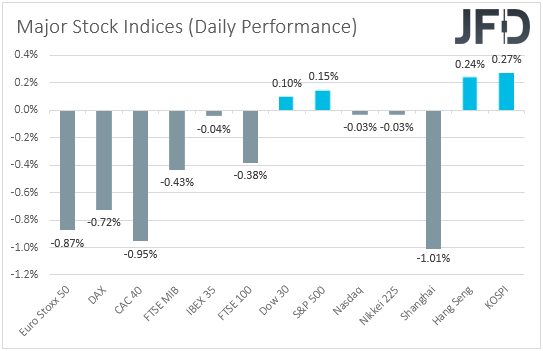

Last week, the firm missed a payment on offshore bonds, with more payments due this week. We repeat that Evergrande has 30 days to settle the payments following their scheduled date. Otherwise, the bonds will default. So, with that in mind, the default risks remain will on the table, and therefore, they could weigh more on the broader market sentiment.

Appetite was soft on Friday, while today, China's Shanghai Composite fell around 1%.

During the European session, Germany releases its preliminary inflation data for September. The CPI and HICP YOY rates could rise further, to +4.2% and +3.8%, from +3.9% to +3.4%, respectively. This may raise speculation that Eurozone's headline rate may increase as well. From the UK and the US, we get the final GDP prints for Q2, but as is the case most of the time, they might not confirm their preliminary or second estimates.

Finally, on Friday, Asian time, Japan's Tankan survey for Q3 will be released, with the Large Manufacturers Index (LMI) expected to have ticked down to 13 from 14. Still, the Large non-manufacturers index is forecast to rise to 3 from 1. The nation's employment report for August is also coming out.

During the EU session, we have Eurozone's preliminary CPIs for September. The headline CPI rate could rise to +3.3% YoY from +3.0%, while the HICP excluding Energy and Food is forecast to increase to +1.8% YoY from +1.6%.

Despite the headline rate moving further above the ECB's objective of 2%, underlying inflation could stay below that target, something that may add more credence to the ECB's view that policy should remain accommodative, despite the slowdown in PEPP purchases.

Later in the day, from the US, we have the personal income and spending numbers for August and the core PCE index for the month. The ISM non-manufacturing index for September is also on the agenda. Its forecast points to a slight decline, to 59.5 from 59.9. From Canada, we get the monthly GDP for July.