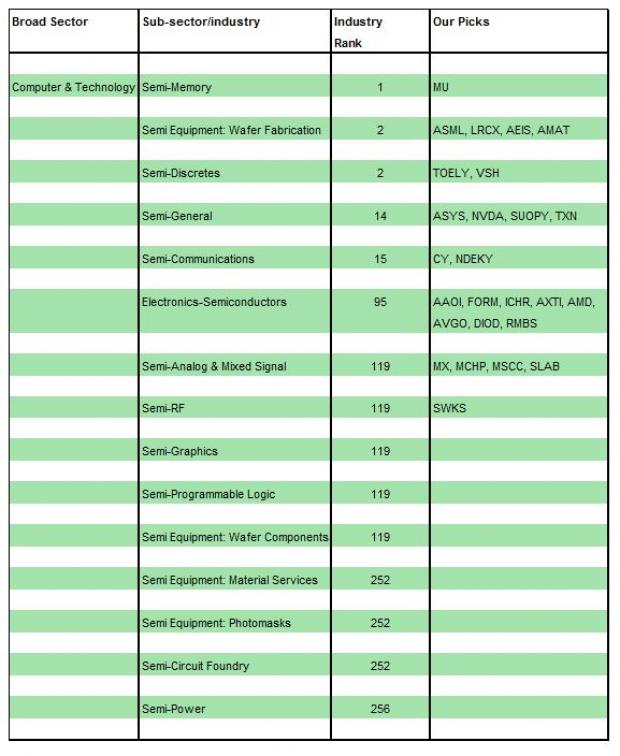

The semiconductor industry is made up of 15 sub-sectors (including 4 for semiconductor equipment) within the Technology sector, which is one of the 16 broad Zacks-categorized sectors.

Similar to the Technology sector, Zacks also breaks down each of the other sectors into groups such that there are a total of 264 sub-sectors or industries. These “X” industries are then grouped in two: the top half (i.e., industries with the best average Zacks Rank) and the bottom half (industries with the worst average Zacks Rank). Over the last 10 years, using a one-week rebalance, the top half beat the bottom half by a factor of more than 2 to 1. (Click here to know more: About Zacks Industry Rank)

Therefore the Zacks Industry Rank is a good indicator of investment opportunities within an industry at any given time. Moreover, because stocks in the same X industry have certain common positive or negative factors affecting them, it has been observed that there is some positive correlation between them.

The X industries pertaining to semiconductor stocks have been tabulated below. The list clearly displays the kind of industries likely to have more winners. The last column enlists our picks, which are basically Zacks Rank #1 (Strong Buy) or Rank #2 (Buy) stocks within the top 132 X industries.

Earnings Trends at a Glance

One of the main factors driving the Zacks Rank for individual stocks is earnings results. Therefore, it makes sense to take a look at how those have been in the last-reported quarter.

From the latest earnings trends report, we see that 80.3% of technology stocks have reported with both top and bottom line results beating the S&P 500. Overall, technology stocks’ earnings were up 17.9% from the year-ago quarter on 9.2% growth. This compares with earnings and revenue growth of 10.8% and 5.8%, respectively. Also, 83.7% of technology stocks beat earnings estimates compared to 74.3% for the S&P 500. A like percentage of technology companies also beat revenue expectations with the S&P 500 averaging much lower at 68.0%.

Major Drivers

This section can be divided into the current and emerging drivers. But before getting into that, it’s important to understand the backdrop. This includes a shrinking traditional market (mainly PCs) that still consumes the bulk of chips as well as several emerging categories that have extremely strong growth potential. Which means that while the industry as a whole may appear sluggish, there are some solid opportunities.

Current Drivers

As far as current drivers are concerned, the most significant are cloud computing, big data and artificial intelligence that are increasing demand for servers and data centers exponentially. Intel (INTC) and NVIDIA (NVDA) are the strongest positioned here, with Intel’s strength mainly on the enterprise side and NVIDIA’s on the HPC side. Intel is working to challenge NVIDIA, but that will take time.

HPC is where a lot of the innovation is going on and NVIDIA continues to pick up share of spending because of its lead in machine learning. Intel has plans to get in the game with the technology it acquired through Nervana Systems and Altera. Both Intel and NVIDIA are working on hybrid solutions because GPUs do a better job of processing the huge amounts of data to train a neural network while CPUs do a better job of applying that data to a given situation.

Xilinx (NASDAQ:XLNX) (XLNX) is another important player working with FPGAs on top of ARM-based chips. With a $16 billion artificial intelligence market (according to MarketsandMarkets) by 2020 waiting to be tapped, it’s no wonder that players are going all out to grab their share.

Some disruption is afoot in the enterprise segment as well because of the work done by the Open Compute Project (OCP) that Facebook (NASDAQ:FB) (FB) founded and continues to feed. The social networking company generates huge volumes of data that it needs to store, manage and process as quickly and cost-efficiently as possible.

Others with similar interest like Apple (AAPL), Microsoft (MSFT) and Google (GOOGL), and differing interest like Intel, HP, Cisco (CSCO) and Juniper are also part of the project. Facebook designs hardware that is then optimized by the OCP so it becomes something members can standardize on. So far, so good. But if the OCP is able to design chips that perform better or comparably with Intel chips, the chip maker’s cloud business can be hurt. Intel being part of the effort implies that it is working to get its technology in as part of the standard.

Another challenge for traditional semiconductor players includesGoogle, which is working with IBM’s (IBM) new chip designs. It is reportedly the only top chip buyer that doesn’t sell servers but instead builds them for internal use. Therefore, Google’s decisions are significant in the chip consumption context.

Google has done two things in the past that could be viewed as second-sourcing or maybe creating leverage against Intel to pressure it into lowering prices. The company has declared that everything it now does also supports IBM’s Power systems and it is also in talks with Qualcomm (QCOM) that could result in its using some of its ARM-based server chips.

Amazon (NASDAQ:AMZN) is the leading provider of cloud infrastructure, followed by Microsoft, IBM and Google. This is another chip-hungry segment with long-term demand for the devices. Since infrastructure providers need a huge number of chips, each has its own development efforts. Amazon for instance has acquired and hired people for the purpose; Google has announced that it is testing IBM and ARM technology while Microsoft is collaborating with Qualcomm to test ARM designs.

Cost per watt, reliability and low-latency are factors determining purchases and it’s possible that all these efforts will eventually beat Intel. It’s only when (or if) these players take their consumption in house will there be pressure on semiconductor players. In that case, Intel the incumbent would be the worst affected.

Another important segment for semiconductor companies that is relatively low-key is Industrial. Since semiconductors facilitate increased automation on the factory floor, they are increasingly used to drive efficiency and lower cost. Reportedly, PricewaterhouseCoopers (PwC) expects the industrial semiconductor market to grow at a CAGR (compounded annual growth rate) of 9.7% between 2014 and 2019. IHS Markit says that the market grew 3.8% in 2016 to $43.5 billion driven by commercial and military avionics, digital signage, network video surveillance, HVAC, smart meters, PV inverters, LED lighting and various medical electronics.

The U.S. is the biggest spender but improving economic conditions in Europe, China, India and Brazil also drove demand. A Global Industry Analysts (GIA) report says that the U.S. is the largest market for industrial semiconductors although the Asia/Pacific is the fastest growing on account of its being a manufacturing hub. The overall market is expected to be worth $60 billion by 2022.

One of the fastest-growing emerging markets for semiconductor devices is automotive, as the consumption of electronic components for safety, infotainment, navigation and fuel efficiency continues to increase. A recent report from MarketsandMarkets says that the automotive semiconductor market will grow at a CAGR of 5.8% from 2016 through 2022.

Power components like MOSFET and IGBT devices are some of the fastest growing because of the increased electrification of vehicles. The growing middle class in several Asian markets like China, India, Thailand, Indonesia and Malaysia is greatly increasing the demand for passenger cars, thus accounting for most of the semiconductor shipments into the automotive market.

Infineon, STMicroelectronics, Renesas (which acquired Intersil), Texas Instruments (TXN), Analog Devices (ADI) and Cypress are important players. Qualcomm, after its acquisition of NXP Semiconductor, which itself acquired Freescale Semiconductor, has become a major player in automotive semiconductors.

The automotive market has an emerging adjacent market in the form of autonomous/self-driving cars that will consume a huge number of semiconductors, particularly sensors, processors and other technology enabling the vehicles.

Wireless infrastructure builds have been necessitated by increasing data volumes and connectivity issues (network congestion, power reliability, privacy and security) in wireless networks. These builds will require increased investment in semiconductors, thus driving sales. New materials (a compound of two or more) are being used in this segment with Galium Nitride gaining share of RF high-power semiconductors, according to ABI Research.

According to Strategy Analytics, the greatest driver of these compound semiconductors is the convergence of voice, video and data networks that is leading to the explosive growth of data traffic across wireless devices, within fixed and wireless networks, in driver assistance systems, in network-centric battlefield philosophies, solid-state lighting and high-power electronics. The firm expects compound semiconductor revenue to grow at a 13% compounded average annual growth rate (CAAGR) to double revenue to $11 billion by 2020.

The PC market still consumes a large number of chips but its importance as a driver continues to decline. That’s because the market itself is shrinking (Gartner estimates that it declined 4.3% in the second quarter while IDC estimates that it declined 3.3%). IDC believes that Japan grew for the second straight quarter with LatAm and the U.S. outperforming its expectations. Gartner doesn’t include chromebooks in its calculations, but said that they were moderately impacting the PC market posting 38% growth in 2016 compared to a 6% decline in PCs.

Consumers are hesitant to spend on upgrades given that they already have many more devices than they need (developed markets) and because Internet and many other conveniences of computers are now easily available on smartphones and tablets (emerging markets). But gaming enthusiasts and enterprises require stronger and faster machines, so they are the major drivers.

In either case, it’s very clear that the steady growth seen in years past is history. IDC, for one, expects the PC market to shrink 2.1% in 2017. So semiconductor players with PC market exposure can at best profit from market share gains, BYOD exposure and increased exposure to the top PC vendors, which are HP, Lenovo, Dell, Apple and Asus according to both IDC and Gartner.

Apple makes its own PCs, software and also a lot of its own processors, relying largely on Intel, Qualcomm and Samsung (KS:005930) for its other semiconductor requirements. Microsoft makes software and limited quantities of hardware, relying largely on third-party device makers for chips, PCs and mobile devices. It’s also a major player in the cloud, which makes it an important ally for semiconductor companies like Intel, Qualcomm or NVIDIA. Alphabet’s chromebooks on the other hand are made by a number of hardware makers that use either Intel or ARM technology.

Emerging Drivers

Traditionally, the consumer technology market included smartphones, tablets and electronic gadgets like LCD TVs and Blu-ray players. But that is changing as we speak with the Consumer Technology Association (CTA), formerly called Consumer Electronics Association ("CEA") estimating that U.S. consumer technology retail sales will be driven by IoT this year to touch $321 billion (estimate six months earlier was $286.6 billion).

Moreover, these traditional segments are expected to decline this year with their contribution dropping to less than 50% of total sales for the first time next year. Smartphones, tablets and TVs are mature categories with shipments expected to grow a respective 3%, -5% and -1%. Laptops will grow 2%.

Of the emerging technology categories, ultra 4K HD TVs will grow 59%; wearables will grow 9% (includes fitness activity trackers, other health and fitness devices, hearables, over-the-counter hearing devices and smartwatches); smart Home encompassing products like thermostats, smart smoke and CO2 detectors, IP/Wi-Fi cameras, smart locks, smart home systems, and smart switches, dimmers and outlets, will grow 50%; drones will grow 40%, VR 79% and voice-activated digital assistants like Amazon’s Echo 53%.

Most of the emerging technology categories fall in the group more commonly referred to as Internet of Things (IoT). A recent McKinsey report says that the installed base of IoT devices was in the range of 7-10 billion at 2015-end and is expected to increase by about 15-20% annually over the next few years to 26-30 billion units by 2020.

IC Insights estimates that IoT semiconductor sales will increase 16.2% in 2017 to $21.3 billion and will grow at a CAGR of 14.9% from 2015 to 2020. For the period, semiconductor revenue growth in smart cities of 8.9%, wearables 17.1%, industrial Internet 24.1%, connected homes 21.3% and connected vehicles 32.9%.

However, despite the strong revenue prospects, this is still a nascent market with several challenges to its continued growth. These would be security/privacy because of the huge amount of data generated and collected, still-limited availability of consistent standards enabling interoperability, relatively low ROI for chipmakers necessitating the integration of additional technology or the final product by the chipmaker, and the possibility of a growing number of niche products.

Companies are doubling down on these challenges. For instance, NXP is part of the Embedded Microprocessor Benchmarking Consortium (EEMBC) to identify embedded security gaps and set guidelines for IoT manufacturers to make more secure devices.

Also, both Intel and ARM (now acquired by Softbank) have increased focus on security. Intel is working on building chip-level security while also facilitating security in the cloud through the McAfee Data Exchange Layer. ARM will likely build some security features into its designs.

On the standardization front, companies like Intel, IBM, Cisco, GE and AT&T (NYSE:T) have formed the Industrial Internet Consortium to develop common standards. The process could take time but once available, the standards could generate higher-margin revenue for semiconductor players. There will, however, be increased scrutiny on privacy considerations.

Component Forecast

The Semiconductor Industry Association (SIA) estimates that semiconductor sales in 2016 were up 1.1% from 2015 levels (versus expectations of a 0.1% increase. Logic, memory and micro-ICs were the top three segments, sensors and actuators was the fastest growing segment (up 22.7%), NAND Flash (up 11.0%), DSP (12.5%), diodes 8.7%, small signal transistors 7.3% and analog 5.8%. regionally, China was strongest (up 9.2%) followed by Japan (up 3.8%), while Asia Pacific/All Other dropped 1.7%, Europe dropped 4.5% and the Americas were down 4.7%. WSTS data projects 2017 growth of 6.5% (previous 3.3%) driven by sensors, analog and memory. It will be followed by 2.3% growth in 2018.

IC Insights has doubled its 2017 growth forecast to 11% (previous 5%) because of significant upward revisions in DRAM (up 39%) and NAND (up 25%) sales. The increase will be driven by higher prices (37% for DRAM and 22% for NAND).

Gartner estimates that semiconductor capital spending will rise 10.2% in 2017 due to strong manufacturing demand in memory and leading-edge logic. WFE and packaging will grow 17.9% with other semiconductor capital spending growing 1.8%.

Definition

The Semiconductor Industry serves as a driver, enabler and indicator of technological progress. Developments in the industry determine the way we work, transport ourselves, communicate, entertain ourselves, defend ourselves and respond to our environment.

The emergence of categories like health monitoring devices and home automation gadgets, and the increased automation on factory floors, automobiles and elsewhere have added a new dimension to the industry. Environmental concerns and the need for judicious use of resources have also opened upopportunities in the form of chipsreducing power consumption, reducing heat dissipation, capturing solar energy, creating more efficient lighting solutions and so forth.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaries," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Xilinx, Inc. (XLNX): Free Stock Analysis Report

Texas Instruments Incorporated (NASDAQ:TXN): Free Stock Analysis Report

QUALCOMM Incorporated (NASDAQ:QCOM): Free Stock Analysis Report

NVIDIA Corporation (NASDAQ:NVDA): Free Stock Analysis Report

Microsoft Corporation (NASDAQ:MSFT): Free Stock Analysis Report

Intel Corporation (NASDAQ:INTC): Free Stock Analysis Report

International Business Machines Corporation (NYSE:IBM): Free Stock Analysis Report

Alphabet Inc. (NASDAQ:GOOGL): Free Stock Analysis Report

Facebook, Inc. (FB): Free Stock Analysis Report

Cisco Systems, Inc. (NASDAQ:CSCO): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Apple Inc. (NASDAQ:AAPL): Free Stock Analysis Report

Original post

Zacks Investment Research