Markets had another interesting week as US President Donald Trump pledged more tariffs ahead. A potential peace deal appears to be gaining traction between Russia and Ukraine but this did little to dent the appeal of Safe havens as Gold continues to hold the high ground.

US Equity markets did take a slight hit toward the backend of the week largely driven by news from Walmart (NYSE:WMT).

The $780 billion retailer reported strong holiday and January sales, thanks to wealthier customers looking for deals. However, it warned that inflation could hurt shoppers, causing its stock value to drop by 6%. This shows that the economic optimism seen after Donald Trump’s election may be starting to fade.

Walmart acknowledged “uncertain times,” which led to a cautious outlook and a $50 billion drop in its market value. Being a key indicator of U.S. spending habits, Walmart’s concerns matter. Even Donald Trump admitted that “inflation is back,” and research shows consumer confidence in business and jobs fell sharply in January.

Wall Street is also uneasy. David Kelly, a strategist at JPMorgan, warned about risks to economic growth from new policies, including tariffs and deportations. If Walmart is feeling nervous, it could signal a growing wave of fear in the economy.

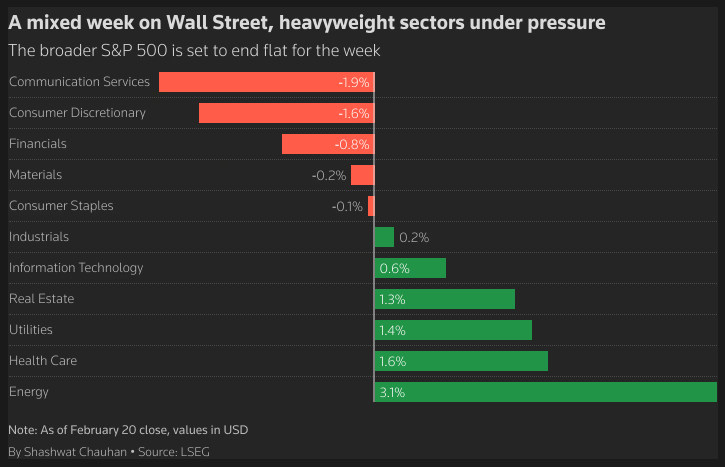

This was compounded by weak US data as the S&P Global data showed that U.S. business activity barely grew in February as worries about import tariffs and major government spending cuts increased.

The S&P 500 and Nasdaq 100 both printed fresh highs before a selloff on Thursday and Friday, reflecting the market’s concerns about these developments.

Source: LSEG

On the commodities front, Gold continued its advance this week but did have a bit of a seesaw run. The one concern that bulls may have is that this week’s rally failed to print fresh all-time highs. Is this a sign that bullish pressure may be waning?

Oil prices had an interesting week with gains every day before a significant selloff on Friday left Brent crude trading flat for the week. Supply jitters continue to persist, but President Trump’s wish of lower energy and oil prices clearly is weighing on the minds of market participants. News filtered through today that the US is putting pressure on Iraq to restart the pipeline to Turkey which could explain the fall in Oil prices, or at least partially so.

On the FX front, the US Dollar struggled this week largely due to a massive selloff on Thursday. This was a surprise given that Wednesday FOMC minutes showed the Fed is concerned about the impact of tariffs on inflation. This has led to the idea that rate cuts may be pushed back later in the year than had been previously anticipated.

The Week Ahead: US CPE Will be Key After Hot US CPI data, German Elections are in Focus as Well

Asia Pacific Markets

The main focus this week in the Asia Pacific region for me will be inflation data from Japan while we also have some Chinese data to monitor.

The week’s key focus is Tokyo’s inflation data, expected to hold at 3.3% in February. Rising fresh food prices may drive costs up, but energy subsidies should balance this out. The BoJ will monitor if higher food costs, like rice, are affecting consumers. Economic data suggests a slow recovery, with industrial output improving due to exports and retail sales boosted by better wages and more tourists.

China’s schedule for economic data is light in the last week of February. On Tuesday, the People’s Bank of China is expected to decide on the medium-term lending facility (MLF) rate. Since the focus has shifted to the 7-day reverse repo rate as the main policy tool, no changes to the MLF rate are expected this month. Any surprise however could have a knock on effect on emerging markets.

Europe + UK + US

In developed markets, the US CPI release last week really stoked concerns about higher rates for longer. However, Fed Chair Powell was quick to stress how the Fed prefers the PCE data as their inflation gauge and cautioned against reading too much into the CPI release.

Next (LON:NXT) week’s PCE data includes the Fed’s preferred inflation measure, the core personal consumer expenditure (PCE) deflator. While the core CPI rose by a concerning 0.4% month-on-month, other data suggests that the core PCE deflator is likely to show a smaller increase of 0.3%. To reach the 2% yearly inflation target, monthly inflation needs to average 0.17%. Due to these factors, it’s unlikely we’ll see any rate cuts before the September FOMC meeting.

Europe’s most industrialized economy faces a big weekend as Germans head to the polls in what will be a key election for Europe as a whole. The German economy faces a host of challenges while the question of immigration has also been a key campaign point.

The elections could have an impact on both the Euro and German Bunds as well when the market opens on Sunday night.

Chart of the Week

This week’s focus is on the US Dollar Index (DXY) after Thursday’s selloff and a break of the key level of support at 107.00.

Moving into next week and with the PCE data on the horizon, will the DXY rebound? That is the big question for market participants.

Currently the DXY has found support at the 100-day MA resting at 106.47 with a bullish inside bar candle close on Friday.

This leaves me to believe that we could get some bullish strength on Monday and perhaps a retest of the 107.00 handle.

More tariff chatter could help propel the DXY above the support turned resistance at 107.00, however in the absence of tariff chatter the DXY may grind sideways until the release of the PCE Data.

US Dollar Index Daily Chart – February 21, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 106.47

- 106.13

- 105.63

Resistance

- 107.00

- 108.00

- 108.49