Value investing is easily one of the most popular ways to find great stocks in any market environment. After all, who wouldn’t want to find stocks that are either flying under the radar and are compelling buys, or offer up tantalizing discounts when compared to fair value?

One way to find these companies is by looking at several key metrics and financial ratios, many of which are crucial in the value stock selection process. Let’s put Royal Caribbean Cruises Ltd. (NYSE:RCL) stock into this equation and find out if it is a good choice for value-oriented investors right now, or if investors subscribing to this methodology should look elsewhere for top picks:

PE Ratio

A key metric that value investors always look at is the Price to Earnings Ratio, or PE for short. This shows us how much investors are willing to pay for each dollar of earnings in a given stock, and is easily one of the most popular financial ratios in the world. The best use of the PE ratio is to compare the stock’s current PE ratio with: a) where this ratio has been in the past; b) how it compares to the average for the industry/sector; and c) how it compares to the market as a whole.

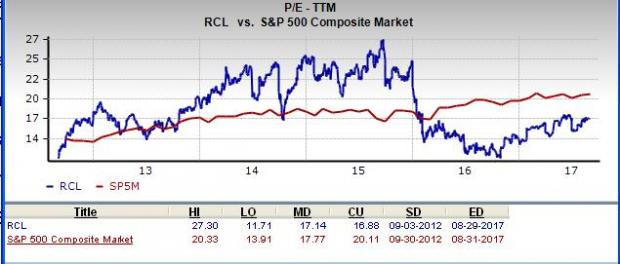

On this front, Royal Caribbean has a trailing twelve months PE ratio of 16.88, as you can see in the chart below:

This level actually compares pretty favorably with the market at large, as the PE for the S&P 500 stands at about 20.11. If we focus on the long-term PE trend, Royal Caribbean’s current PE level puts it below its midpoint over the past five years, with the number having risen rapidly over the past few months.

Further, the stock’s PE also compares favorably with the broader industry’s trailing twelve months PE ratio, which stands at 22.53. At the very least, this indicates that the stock is relatively undervalued right now, compared to its peers.

We should also point out that Royal Caribbean has a forward PE ratio (price relative to this year’s earnings) of just 16.74, so it is fair to say that a slightly more value-oriented path may be ahead for Royal Caribbean stock in the near term too.

P/CF Ratio

An often overlooked ratio that can still be a great indicator of value is the price/cash flow metric. This ratio doesn’t take amortization and depreciation into account, so can give a more accurate picture of the financial health in a business. This is a preferred metric to some valuation investors because cash flows are (a) generally less prone to manipulation by the company’s management, and (b) are less affected by variation in accounting policies between different companies.

The ratio is generally applied to find out whether a company’s stock is overpriced or underpriced with reference to its cash flows generation potential compared with its competitors. However, it is not commonly used for cross-industry comparison, as the average price to cash flow ratio varies from industry to industry.

In this case, Royal Caribbean’s P/CF ratio of 10.1 is higher than the broader industry’s average of 9.1, which indicates that the stock is somewhat overvalued in this respect.

Broad Value Outlook

In aggregate, Royal Caribbean currently has a Value Score of B, putting it into the top 40% of all stocks we cover from this look. This makes Royal Caribbean a solid choice for value investors, and some of its other key metrics make this pretty clear too.

For example, the PEG ratio for Royal Caribbean is just 0.7, a level that is far lower than the industry average of 1.4. The PEG ratio is a modified PE ratio that takes into account the stock’s earnings growth rate.

What About the Stock Overall?

Though Royal Caribbean might be a good choice for value investors, there are plenty of other factors to consider before investing in this name. In particular, it is worth noting that the company has a Growth Score of A and a Momentum Score of B. This gives RCL a Zacks VGM score — or its overarching fundamental grade — of A. (You can read more about the Zacks Style Scores here >>)

Meanwhile, the company’s recent earnings estimates have been mixed at best. The current quarter has seen eight estimates go higher in the past sixty days, while the full year estimate has seen nine up in the same time period.

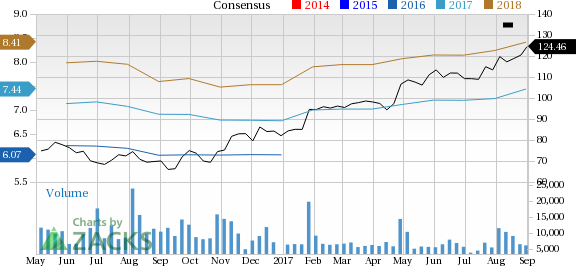

This has had just a small impact on the consensus estimate though as the current quarter consensus estimate has risen by 6.1% in the past two months, while the full year estimate has increased by 3.1%. You can see the consensus estimate trend and recent price action for the stock in the chart below:

Royal Caribbean Cruises Ltd. Price and Consensus

Royal Caribbean Cruises Ltd. Price and Consensus | Royal Caribbean Cruises Ltd. Quote

This positive trend signifies bullish analyst sentiment, and its Zacks Rank #2 (Buy) indicates robust fundamentals and expectations of outperformance in the near term.

Bottom Line

Royal Caribbean is an inspired choice for value investors, as it is hard to beat its incredible lineup of statistics on this front. However, with a sluggish industry rank it is hard to get too excited about this company overall. In fact, over the past two years, the broader industry has clearly underperformed the broader market, as you can see below:

So, value investors might want to wait for the broader factors to turn around in this name first, but once that happens, this stock could be a compelling pick.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Royal Caribbean Cruises Ltd. (RCL): Free Stock Analysis Report

Original post

Zacks Investment Research