Value investing is easily one of the most popular ways to find great stocks in any market environment. After all, who wouldn’t want to find stocks that are either flying under the radar and are compelling buys, or offer up tantalizing discounts when compared to fair value?

One way to find these companies is by looking at several key metrics and financial ratios, many of which are crucial in the value stock selection process. Let’s put Ralph Lauren Corporation (NYSE:RL) stock into this equation and find out if it is a good choice for value-oriented investors right now, or if investors subscribing to this methodology should look elsewhere for top picks:

PE Ratio

A key metric that value investors always look at is the Price to Earnings Ratio, or PE for short. This shows us how much investors are willing to pay for each dollar of earnings in a given stock, and is easily one of the most popular financial ratios in the world. The best use of the PE ratio is to compare the stock’s current PE ratio with: a) where this ratio has been in the past; b) how it compares to the average for the industry/sector; and c) how it compares to the market as a whole.

On this front, Ralph Lauren has a trailing twelve months PE ratio of 15.14. This level compares pretty favorably with the market at large, as the PE ratio for the S&P 500 comes in at about 19.87.

If we focus on the long-term trend of the stock the current level puts Ralph Lauren’s current PE among its lower zone, well below its median for the term (which stands at 18.09x). Hence, we could infer that the stock is undervalued in this respect, especially in light of its historical trend. Thus, the present level seems to be a suitable entry point for the stock from a PE perspective.

Further, the stock’s PE also compares favorably with its industry’s trailing twelve months PE ratio, which stands at 19.31. At the very least, this indicates that the stock is relatively undervalued right now, compared to its peers. In fact, since the beginning of 2014, Ralph Lauren has been consistently trading cheaper than the industry in terms of PE.

PS Ratio

Another key metric to note is the Price/Sales ratio. This approach compares a given stock’s price to its total sales, where a lower reading is generally considered better. Some people like this metric more than other value-focused ones because it looks at sales, something that is far harder to manipulate with accounting tricks than earnings.

Right now, Ralph Lauren has a P/S ratio of about 1.12. This is lower than industry average, which comes in at 1.84x right now. Also, this is in the lower zone for this stock in particular, over the observed term.

This clearly suggests some level of undervalued trading for RL—at least compared to historical norms.

Broad Value Outlook

In aggregate, Ralph Lauren currently has a Value Score of ‘B’, putting it into the top 40% of all stocks we cover from this look. This makes Ralph Lauren an apt choice for value investors, and some of its other key metrics make this pretty clear too.

For example, the PEG ratio for Ralph Lauren is just 1.11, a level that is lower than the industry average of 1.38. The PEG ratio is a modified PE ratio that takes into account the stock’s earnings growth rate. Additionally, its P/CF ratio (another great indicator of value) comes in at just 5.46, which is far better than the industry average of 9.47. Clearly, RL is a solid choice on the value front from multiple angles.

What About the Stock Overall?

Though Ralph Lauren might be a good choice for value investors, there are plenty of other factors to consider before investing in this name. In particular, it is worth noting that the company has a Growth grade of ‘A’ and a Momentum score of ‘A’. This gives RL a Zacks VGM score—or its overarching fundamental grade—of ‘A’. (You can read more about the Zacks Style Scores here >>)

Our VGM Score identifies stocks that have the most attractive value, growth, and momentum characteristics, and a good VGM score can increase your odds of success. All things considered, Ralph Lauren seems to have pretty striking prospects.

Meanwhile, the company’s recent earnings estimates have been trending upward lately. The current quarter has seen four estimates go higher in the past thirty days compared to none lower, while the full year estimate has seen six upward revisions and no downward revisions in the same time period.

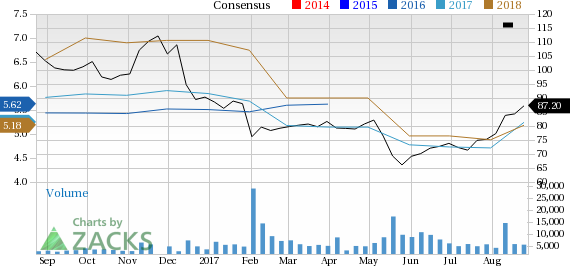

This has had a meaningful impact on the consensus estimate as the current quarter consensus estimate has jumped 22.1% in the past month, while the full year estimate has increased 11.3%. You can see the consensus estimate trend and recent price action for the stock in the chart below:

Ralph Lauren Corporation Price and Consensus

The stock holds a Zacks Rank #3 (Hold), which indicates expectations of in-line performance from the company in the near term. However, Ralph Lauren is enjoying bullish analyst sentiment, as indicated by the positive estimate revisions, and this works in the company’s favor.

Bottom Line

Ralph Lauren is an inspired choice for value investors, as it is hard to beat its incredible lineup of statistics on this front. Moreover, a strong industry rank (Top 20% out of more than 250 industries) further supports the growth potential of the stock.

Recently, Ralph Lauren posted solid first-quarter fiscal 2018 earnings, which grew year over year and marked its 10th straight beat. Management remained impressed with its performance, as it enhanced quality of sales by reducing promotions and markdowns, alongside reducing SKU count to drive productivity. Further, the company managed to curtail inventory levels and also achieved cost savings by lowering operating costs. These factors, which also drove margins, clearly reflect Ralph Lauren’s focus on its Way Forward Plan and Restructuring activities.

So, despite a Zacks Rank #3, we believe that it might pay for value investors to delve deeper into the company’s prospects, as fundamentals indicate that this stock could be a compelling pick.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Ralph Lauren Corporation (RL): Free Stock Analysis Report

Original post