My previous article about Freedom Holding Corp (NASDAQ:FRHC) was published on Investing.com approximately seven months ago. Since then, the stock has increased by more than 40%, significantly beating most broader market indices like the S&P 500 or even the NASDAQ Composite.

[Source: Investing.com, FRHC since 04/09/2024]

Previously, I explained in detail why the company's strategic shift to the telecom and streaming sectors should add significant value. I still hold this view today, as I believe management continues to follow this chosen path. The performance and market capitalization growth we've observed over the past five years is more than justified, and I assess Freedom Holding's prospects for further growth as very promising.

Freedom Holding reported for its fiscal Q1 FY2025 (quarter ended on June 30, 2024) in early August, delivering generally robust results for all of its segments.

The brokerage segment - comprising 49 offices in Kazakhstan, Cyprus, and the United States - provided securities brokerage services across all sectors and hired 1,510 people, including 1,219 full-time employees. Freedom Bank KZ lost 3% assets and 5% loan volume, but its deposit volume rose 11%. Although the trading portfolio shrank due to “negative appraisal of quasi-government bonds”, the interest revenue amount grew.

The insurance business line performed well, as well: 944 employees and 29.5% growth in clients helped keep the leading position in Kazakhstan’s online insurance market.

Freedom Holding’s increased customer base resulted in 42.5% revenue growth over the same period to approximately $450.7 million in Q1 FY2025 compared to $316.2 million in 2023. Interest income increased 51% to $226.0 million with the growth coming from margin loans, customer loans, and trading securities. Revenue from underwriting for insurance rose 188% to $129.4 million, driven by growth in pension annuity and accident coverage classes. Brokerage fees and commissions increased 17% to $115.5 million. The business also experienced a $12.5 million net derivative gain (a 141% increase) on currency swap revaluations.

The company's trading activities, including the sale of securities, resulted in a net loss of $52.1 million, which was primarily attributable to Kazakhstan sovereign bonds. As a result, the company's phenomenal growth in operations suffered some financial setbacks that could temporarily affect the overall business outlook.

Despite the challenges in Q1, I believe the strategic investments and ongoing client growth provide a strong foundation for overcoming these challenges and for future success.

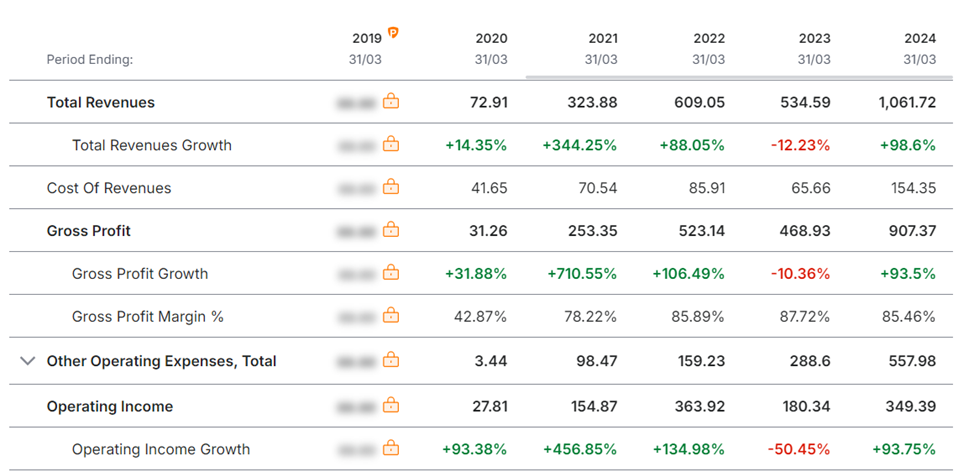

If we just zoom out and look outside the latest quarter, which was full of one-off events damaging the growth picture, we’ll see consistent revenue growth, including a record full-year revenue of $1.6 billion in fiscal 2024 (+105% year-on-year), with a net profit of $375 million (up 82% YoY), while the holding company’s assets increased by 63% YoY to $8.301 billion. Since I don't believe the challenges faced by FRHC in Q1 will extend into the remaining three quarters of the 2025 fiscal year, the past successes vividly indicate, in my opinion, what lies ahead as the company continues to actively expand and diversify its business ambitions.

Actually, FRHC follows an aggressive international expansion and services diversification as its end markets now span 22 different countries from Kazakhstan, the US to several European countries including Cyprus, Poland, and Spain. I believe Freedom Holding can leverage these diverse growth prospects across both emerging and mature markets through this broad geographical footprint, while their presence in the markets listed above are still minimal (except for Kazakhstan, of course). The European brokerage department alone boasts over 300,000 customers to date, illustrating how the firm is able to attract and keep a huge clientele even in already well-saturated markets. This growth can be attributed to the company's ecosystem approach, where it offers a range of financial products (such as asset management and brokerage services), all at once. By aiming to reach as broad an audience as possible, this strategy appears to be successful.

In addition, Freedom’s innovative attitude makes it a fintech innovator among financial and payment technology firms. Through an exemplary trading platform and innovative banking applications, the company shows its interest in innovation; with strategic investments like its acquisitions of the US broker Prime Executions, the Kazakh companies DITel and Aviata, they have further enhanced their position. In consolidating these various business units, Freedom Holding is developing a total ecosystem, notably in Kazakhstan, with banking, brokerage, insurance, lifestyle and lifestyle, for long-term growth.

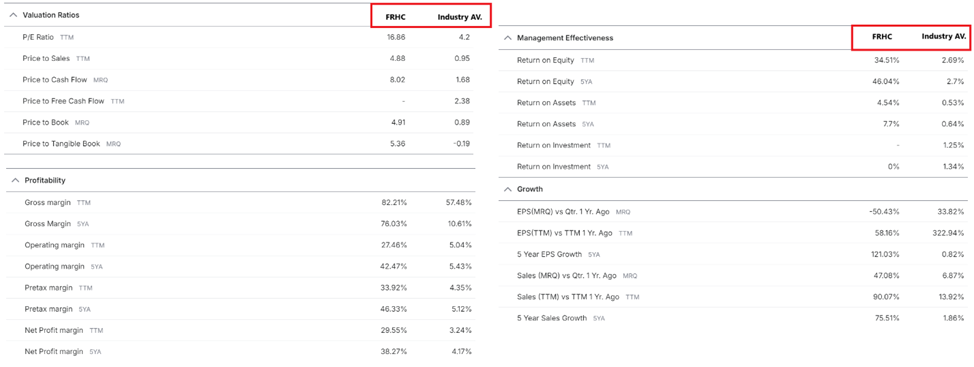

I believe the FRHC stock is trading at a relatively cheap valuation, at just 16.9x its TTM earnings. Yes, according to Investing.com data, this is significantly higher than the average for the financial sector, especially when adjusted for market cap. The same is true for other key valuation multiples. However, it's important to highlight that Freedom Holding's current profitability and key margin metrics are at very solid levels, often exceeding the industry average by a substantial margin. At the same time, the growth of key financial metrics like revenue and net profit far surpasses average industry norms, which, in my opinion, more than justifies the current valuation.

[Source: Investing.com, FRHC, Boris Dubov’s notes]

I think that if we assume a net profit growth of 30-35% next year while maintaining the current P/E multiple of 16-17x, this represents the potential growth for the stock itself that can be anticipated today.

Of course, my upside conclusion carries several important risks.

Firstly, the company operates in an industry with very high regulatory standards. If any issues arise, the company might need to respond quickly, which could amplify the negative effects on its financials observed in the first quarter.

Secondly, Freedom Holding is heavily dependent on its operations in Kazakhstan, meaning that despite being registered in the US (as a holding company), it still faces geographic risks. These risks could potentially hinder the stock's multiple from growing sufficiently to reflect all the business's growth prospects.

However, despite these significant risks, I believe there’s potential for FRHC’s rally we've witnessed over the past years to continue. This October marks the company's anniversary since its listing on the NASDAQ exchange back in 2019, and over the past 5 years, its market cap has increased more than sevenfold, as I noted at the very beginning of this article. I believe this growth is well-deserved, and currently, the stock doesn’t seem overvalued to me. On the contrary, it presents an opportunity for long-term investors to get in, especially since Freedom Holding's profile is still relatively unknown to the wide audience of even highly sophisticated investors.

Therefore, I maintain my positive rating on Freedom Holdings (NASDAQ:FRHC) stock, more than six months after publishing my last article about the company