After navigating brazenly through the rough tide caused by Brexit, investors are again geared up for the Q2 reporting cycle, which has thus far unveiled modest improvement compared to the last couple of quarters. Per the latest Zacks Earnings Trends report as of Jul 22, out of the 126 S&P 500 members that have come up with their quarterly numbers, approximately 70.6% have posted positive earnings surprises, while 55.6% beat top-line expectations.

According to the report, earnings for the 126 S&P 500 companies that have reported so far are down 1.1% from the same period last year, while revenues have dropped 2.6%.

The report further projects that earnings for the total S&P 500 companies will decline 3.4% from the year-ago period, and total revenue will dip 0.5%. We observe that this will be the fifth straight quarter, if the index witnesses a decline in earnings. Well, as the earnings season gets into full swing, the scenario would be much more prominent. So don’t be in a rush to count your chickens before they hatch.

The performance of the index is not restricted to a single sector, and of the 16 Zacks sectors, 9 are expected to witness an earnings decline in Q2, with Basic Materials, Industrial Products, Oil/Energy, Technology and Transportation being a big drag. However, the Consumer Discretionary sector is showing some resilience in spite of overseas turmoil, yet-to-recover Chinese economy, fluctuating commodity prices and Fed rate-related controversies that to an extent are affecting consumers’ spending behavior.

Total earnings for the Consumer Discretionary sector are expected to drop marginally by 0.6%, whereas revenues are projected to increase 3.4%. As of Friday, 22.9% of the total number of S&P 500 companies in this sector had reported their results, wherein all delivered an earnings beat and about half cruised ahead of revenue estimates. While earnings surged 14.4% year over year, revenues advanced 4.4%.Apparel forms part of the Consumer Discretionary sector.

Among Apparel stocks lined up to report, let’s take a sneak peek at two companies.

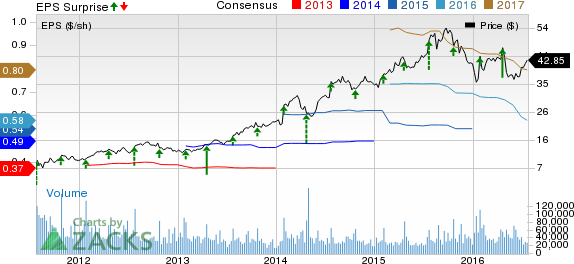

Under Armour, Inc. (NYSE:UA) , the developer, marketer and distributor of branded performance apparel, footwear, and accessories, is slated to report second-quarter 2016 results on Jul 26. Under Armour trimmed its 2016 outlook after one of its major customers, The Sports Authority, faced bankruptcy as it has been burdened with more than $1 billion of debt. For the second quarter, management expects impairment charge of nearly $23 million related to The Sports Authority. Previously, the company had estimated sales of $163 million from the sports retailer for 2016. However, now that it has filed for bankruptcy, Under Armour is likely to recognize only $43 million of the sales. The company now expects net revenue for 2016 to be nearly $4.925 billion, as against the previous estimate of about $5 billion.

However, Under Armour’s sustained focus on brand development, expansion of its DTC business, product innovation and foray into the technology-based fitness business bode well, as it registered revenue growth of over 20% for the past 24 straight quarters. For the second quarter, the company continues to project revenue growth in the high 20% range.

UNDER ARMOUR-A Price, Consensus and EPS Surprise

UNDER ARMOUR-A Price, Consensus and EPS Surprise | UNDER ARMOUR-A Quote

Under Armour carries a Zacks Rank #4 (Sell) with an Earnings ESP of 0.00%. The Zacks Consensus Estimate for the quarter is pegged at 1 cent. (Read: Will Under Armour Q2 Earnings Disappoint Investors?). In the trailing four quarters, the company outperformed the Zacks Consensus Estimate by an average of 34.4%.

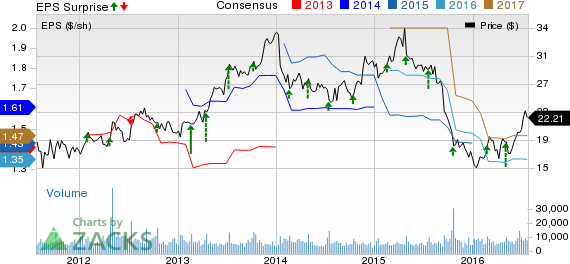

Wolverine World Wide, Inc. (NYSE:WWW) is expected to report second-quarter 2016 results tomorrow. Though the company commenced 2016 on a high note, it might not be able to maintain the momentum in the second quarter, amid economic upheaval both in the U.S. and abroad, as well as a tough domestic retail environment. Strengthening of the U.S. dollar is also likely to have an adverse effect on its performance in the quarter to be reported, given its huge overseas operations. The company expects consolidated reported revenues to decline nearly 4.3–0.5% to $2.475–$2.575 billion in 2016.

Wolverine World Wide has a Zacks Rank #4 with an Earnings ESP of 0.00%. The Zacks Consensus Estimate for the quarter stands at 22 cents. (Read: Wolverine World Wide Q2 Earnings: Will it Disappoint?). In the trailing four quarters, the company outperformed the Zacks Consensus Estimate by an average of 19.6%.

WOLVERINE WORLD Price, Consensus and EPS Surprise

WOLVERINE WORLD Price, Consensus and EPS Surprise | WOLVERINE WORLD Quote

WOLVERINE WORLD (WWW): Free Stock Analysis Report

UNDER ARMOUR-A (UA): Free Stock Analysis Report

Original post

Zacks Investment Research