Value investing is easily one of the most popular ways to find great stocks in any market environment. After all, who wouldn’t want to find stocks that are either flying under the radar and are compelling buys, or offer up tantalizing discounts when compared to fair value?

One way to find these companies is by looking at several key metrics and financial ratios, many of which are crucial in the value stock selection process. Let’s put The Dun & Bradstreet Corporation (NYSE:DNB) stock into this equation and find out if it is a good choice for value-oriented investors right now, or if investors subscribing to this methodology should look elsewhere for top picks.

PE Ratio

A key metric that value investors always look at is the Price to Earnings Ratio, or PE for short. This shows us how much investors are willing to pay for each dollar of earnings in a given stock, and is easily one of the most popular financial ratios in the world. The best use of the PE ratio is to compare the stock’s current PE ratio with: a) where this ratio has been in the past; b) how it compares to the average for the industry/sector; and c) how it compares to the market as a whole.

On this front, Dun & Bradstreet has a trailing twelve months PE ratio of 15.36, as you can see in the chart below:

This level actually compares pretty favorably with the market at large, as the PE for the S&P 500 compares in at about 19.72. If we focus on the stock’s long-term PE trend, the current level puts Dun & Bradstreet’s current PE ratio almost on par with over the past five years.

Further, the stock’s PE also compares favorably with its industry’s trailing twelve months PE ratio, which stands at 25.37. At the very least, this indicates that the stock is relatively undervalued right now, compared to its peers.

We should also point out that Dun & Bradstreet has a forward PE ratio (price relative to this year’s earnings) of 15.67, so it is fair to expect a slight increase in the company’s share price in the near future.

P/S Ratio

Another key metric to note is the Price/Sales ratio. This approach compares a given stock’s price to its total sales, where a lower reading is generally considered better. Some people like this metric more than other value-focused ones because it looks at sales, something that is far harder to manipulate with accounting tricks than earnings.

Right now, Dun & Bradstreet has a P/S ratio of 2.37. This is lower than the S&P 500 average, which comes in at 3.10 right now. Also, as we can see in the chart below, this is below the highs for this stock in particular over the past few years.

If anything, this suggests some level of undervalued trading—at least compared to historical norms.

Broad Value Outlook

In aggregate, Dun & Bradstreet currently has a Zacks Value Style Score of ‘B’, putting it into the top 40% of all stocks we cover from this look. This makes Dun & Bradstreet a solid choice for value investors, and some of its other key metrics make this pretty clear too.

For example, the PEG ratio for Dun & Bradstreet is 1.74, a level that is lower than the industry average of 1.90. The PEG ratio is a modified PE ratio that takes into account the stock’s earnings growth rate. Additionally, its P/CF ratio (another great indicator of value) comes in at 15.09, which is substantially better than the industry average of 19.67. Clearly, Dun & Bradstreet is a solid choice on the value front from multiple angles.

What About the Stock Overall?

Though Dun & Bradstreet might be a good choice for value investors, there are plenty of other factors to consider before investing in this name. In particular, it is worth noting that the company has a Growth grade of ‘D’ and a Momentum score of ‘B’. This gives Dun & Bradstreet a Zacks VGM score—or its overarching fundamental grade—of ‘C’. (You can read more about the Zacks Style Scores here >>)

Meanwhile, the company’s recent earnings estimates have been encouraging. The current year and next has seen four upward estimate revision in the past sixty days, compared to none downward.

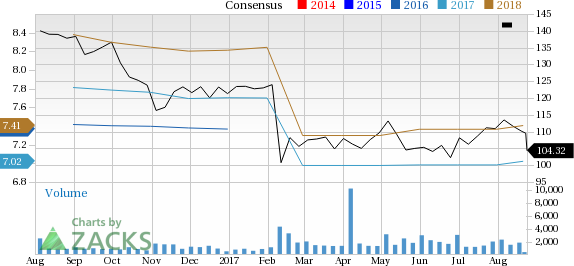

As a result, the current year consensus estimate has increased by about 0.6% in the past two months, while the next year estimate has increased 0.5%. You can see the consensus estimate trend and recent price action for the stock in the chart below:

Dun & Bradstreet Corporation (The) Price and Consensus

This positive trend signifies bullish analyst sentiment, and its Zacks Rank #2 (Buy) indicates robust fundamentals and expectations of outperformance in the near term.

Bottom Line

Dun & Bradstreet is an inspired choice for value investors, as it is hard to beat its incredible lineup of statistics on this front. Furthermore, a robust industry rank (among the Top 28%) and a solid Zacks Rank instills investor confidence. Again, so far this year, the industry to which it belongs has clearly outperformed the broader market, as you can see below:

So, it might pay for value investors to delve deeper into the company’s prospects as fundamentals indicate that this stock could be a compelling pick.

Zacks' 10-Minute Stock-Picking Secret

Since 1988, the Zacks system has more than doubled the S&P 500 with an average gain of +25% per year. With compounding, rebalancing, and exclusive of fees, it can turn thousands into millions of dollars.

But here's something even more remarkable: You can master this proven system without going to a single class or seminar. And then you can apply it to your portfolio in as little as 10 minutes a month.

Learn the secret >>

Dun & Bradstreet Corporation (The) (DNB): Free Stock Analysis Report

Original post

Zacks Investment Research