In the Q2 earnings season, the Finance sector was one of the best performers. Though inflation-related issues and increasing signals of political uncertainty are anticipated, we can still add some of the banking stocks to our portfolio based on strong fundamentals and solid long-term growth opportunities.

Comerica Incorporated (NYSE:CMA) is one such stock that has been witnessing upward estimate revisions, reflecting analysts’ optimism about its future prospects. Over the last 60 days, the Zacks Consensus Estimate for 2017 and 2018 moved up 4.2% and 2.2%, respectively.

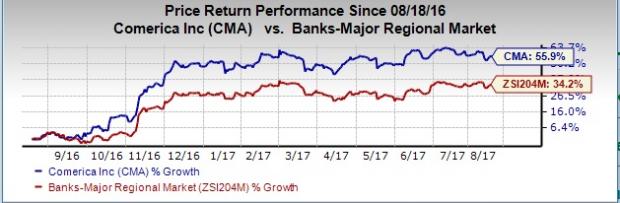

Further, shares of this Zacks Rank #2 (Buy) stock gained around 56% over the last year, outperforming 34.2% growth recorded by the industry it belongs to.

Notably, Comerica has a number of other aspects that make it an attractive investment option.

Why is Comerica a Must Buy

Organic Growth: Comerica continues to make steady progress toward improving its top line. Sales witnessed a 4.3% compounded annual growth rate (CAGR) over the last four years (2013-2016). Also, the company’s projected sales growth (F1/F0) of 10.41% (as against the industry average of about 6.25%) indicates constant upward momentum in revenues.

Earnings Growth: Comerica witnessed earnings growth of 59.5% in the last three-five years. In addition, the company’s long-term (three-five years) estimated EPS growth rate of 18.8% promises rewards for investors over the long run. Also, it recorded average positive earnings surprise of 7.29% over the trailing four quarters.

Prudent Expense Management: Comerica remains on track to achieve its $125-million cost-savings target for 2017 through the GEAR Up initiatives. Expenses decreased in the first six months of 2017. Moreover, the company’s focus on driving long-term efficiency through the GEAR Up initiative keeps us optimistic. Such initiatives are anticipated to deliver annual pre-tax income of about $270 million by the year-end 2018. Further, initial actions will help in achieving a double-digit return on equity and an enhanced shareholder value.

Stock is Undervalued: Comerica has P/E and P/B ratios of 15.14x and 1.84x, compared to the S&P 500 average of 18.92x and 3.10x, respectively. Based on these ratios, the stock seems undervalued.

Strong Leverage: Comerica’s debt/equity ratio is valued at 0.75 compared to the industry average of 0.88, indicating relative lower debt burden. It highlights the financial stability of the company despite an unstable economic environment.

Stocks to Consider

LPL Financial Holdings Inc. (NASDAQ:LPLA) has been witnessing upward estimate revisions for the last 60 days. Over the past year, the company’s share price has been up more than 68%. It also flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Raymond James Financial, Inc. (NYSE:RJF) has been witnessing upward estimate revisions for the last 60 days. Further, the stock has surged nearly 42.1% over the past year. It currently carries a Zacks Rank #2.

E*TRADE Financial Corporation (NASDAQ:ETFC) has been recording upward estimate revisions for the last 60 days. In addition, the company’s shares have risen nearly 61.4% over the past year. It currently holds a Zacks Rank #2.

One Simple Trading Idea

Since 1988, the Zacks system has more than doubled the S&P 500 with an average gain of +25% per year. With compounding, rebalancing, and exclusive of fees, it can turn thousands into millions of dollars.

This proven stock-picking system is grounded on a single big idea that can be fortune shaping and life changing. You can apply it to your portfolio starting today.

Learn more >>

Comerica Incorporated (CMA): Free Stock Analysis Report

E*TRADE Financial Corporation (ETFC): Free Stock Analysis Report

Raymond James Financial, Inc. (RJF): Free Stock Analysis Report

LPL Financial Holdings Inc. (LPLA): Free Stock Analysis Report

Original post

Zacks Investment Research