Signet Jewelers Limited (NYSE:SIG) , a retailer of diamond jewelry, watches and other products, is slated to report second-quarter fiscal 2018 results on Aug 24. In the previous quarter, the company’s earnings missed the Zacks Consensus Estimate by a margin of 38%. Notably, in two out of the trailing four quarters, the company’s earnings lagged the estimate by 0.4%.

What to Expect?

The question lingering in investors’ minds now is whether Signet Jewelers will be able to post positive earnings surprise in the quarter to be reported. The current Zacks Consensus Estimate for the quarter under review is pegged at $1.10, down over 3% year over year. We note that the Zacks Consensus Estimate has been stable in the past 30 days. Analysts polled by Zacks expect revenues of $1,335 million, down nearly 3% from the year-ago quarter.

Factors at Play

In an effort to drive growth in the long run, Signet Jewelers has been implementing certain strategies including growth in mid-market and best in bridal. Moreover, the company is focusing on diversifying store base. Further, it is opening more stores at off-mall locations. Moreover, Signet’s digital marketing efforts and focus on Customer-First omnichannel strategy might help the stock to regain its lost momentum in the near future. The company’s plan to outsource its credit program should also draw investors’ attention, as it is likely to ease some costs and bad debts eventually.

However, the company’s lower-than-expected top-line performance has been a major concern for the investors. Evidently, first-quarter fiscal 2018 marked the company’s 10th straight top-line miss. The industry has been grappling with waning store traffic, stiff competition from online retailers and unwillingness of consumers to spend exorbitantly on discretionary items. It projects same-store sales to decline in the range of low to mid-single digit in fiscal 2018. In fiscal 2017, same-store sales had declined 1.9%. Further, it anticipates earnings per share between $7.00 and $7.40 for the current fiscal year, in comparison with fiscal 2017 figure of $7.45.

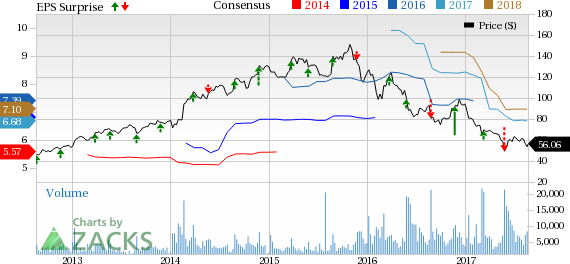

Signet Jewelers Limited Price, Consensus and EPS Surprise

Signet Jewelers Limited Price, Consensus and EPS Surprise | Signet Jewelers Limited Quote

What Does the Zacks Model Unveil?

Our proven model does not conclusively show that Signet Jewelers is likely to beat on earnings estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. Signet Jewelers has an Earnings ESP of -0.19% along with a Zacks Rank #3 makes us less optimistic about the earnings beat. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Stocks Poised to Beat Earnings Estimates

Here are some companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Burlington Stores, Inc. (NYSE:BURL) has an Earnings ESP of +3.23% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Big Lots, Inc. (NYSE:BIG) has an Earnings ESP of +0.72% and a Zacks Rank #2.

GameStop Corp. (NYSE:GME) has an Earnings ESP of +0.31% and a Zacks Rank #3.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Gamestop Corporation (GME): Free Stock Analysis Report

Big Lots, Inc. (BIG): Free Stock Analysis Report

Burlington Stores, Inc. (BURL): Free Stock Analysis Report

Signet Jewelers Limited (SIG): Free Stock Analysis Report

Original post

Zacks Investment Research