Summary: US stocks will likely rise in 2018. By how much is anybody's guess: the standard deviation of annual returns is too wide to get even close to a correct estimate on a consistent basis. Earnings growth implies 6% price appreciation, but tax cuts could boost that to 13%. Investor psychology could push returns much higher (or lower).

While it's true that investors are already bullish and valuations are already high, neither of these implies a likelihood of negative returns in 2018. That the stock market rose strongly this year also has no adverse impact on next year's probable return.

A bear market is always possible, but is also unlikely. That said, the S&P typically experiences a drawdown every year of about 10%; even a 14% fall would be within the normal, annual range. It will feel like the end of the bull market when it happens.

The Fed will likely continue to raise rates next year, which normally leads to higher stock prices. While political risks seem high, the stock market usually ignores these. The "Year 2" presidential cycle provides no investment edge.

This article highlights 11 key ideas to explain what to expect in 2018.

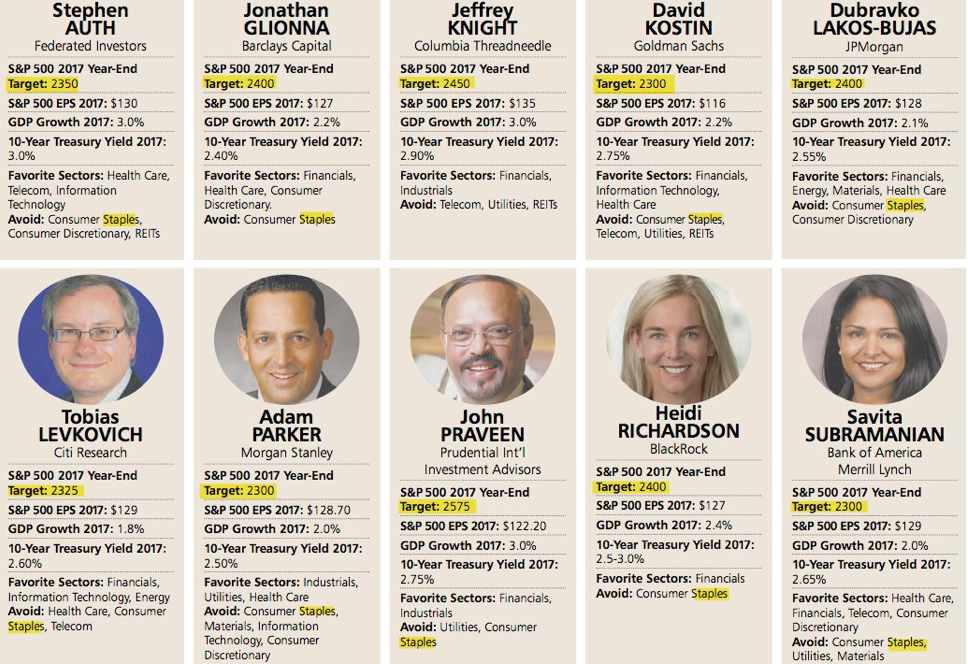

Heading into the end of the year, investment pundits are beginning to share their expectations for how stocks will fare next year. All ten strategists polled by Barron's expect the S&P to rise in 2018, by a mean/median of 6-7% (full article is here; the next three charts from Barron's). Enlarge any image by clicking on it.

It's not a good idea to view these forecasts too precisely. They are rarely so accurate, mostly because data will emerge during the course of the year that forecasters don't have in December when they make their estimates. It's important to realize that strategists provide these forecasts because humans desire certainty. Clients want to know what will happen, even if these guesses are subsequently proven wrong.

Setting rough expectations for the year ahead is appropriate. Even more important is monitoring and adjusting expectations as new data is revealed.

As we look towards 2018, what information is useful and what should be largely ignored in setting expectations for the year ahead? This article highlights 11 key ideas to explain what to expect in 2018.

1. Forget About Precise Price Forecasts

Forecasting where the stock market will finish a year from now is next to impossible. At the end of last year, Wall Street strategists estimated that the S&P would rise to 2380 in 2017, a gain of 5%. That target was reached in February after just 6 weeks. The S&P 500 is now over 2650 and up 17% for the year. Strategists were much too conservative.

In contrast and in hindsight, strategists were absurdly optimistic about 2008. The S&P was heading into its worst year in many generations yet all expected a positive return with an average expected gain of 10%. Instead, stocks fell almost 40%.

Before laughing at how bad these forecasts were, recall that strategists were hardly alone. Professional fund managers, responsible for managing more than $600b in assets, were more than 40% overweight equities in October 2007. Bullish newsletter writers polled by Investors Intelligence outnumbered bears by more than 3 to 1.

The reality is that very few correctly anticipated what would happen in 2008; if they did, it was mostly by luck as proven by the fact that almost all of these pundits have been wrong in expecting a repeat collapse the past several years.

To understand why more precise forecasting of the S&P is so difficult, consider the following:

Over the past 38 years, the S&P has typically gained 10% per year. This is the average.

But the standard deviation from this average is 16%. The standard deviation measures how much any single year typically varies from the average. In other words, it would be normal for the S&P to return anywhere between a loss of 6% to a gain of 26% in any one year. That range captures about 70% of the annual returns since 1980.

The problem is not extreme outliers. The S&P fell 38% in 2008 and 23% in 2002, its two worst years since 1980. At the other end of the spectrum, the S&P gained 35% in 1995 and 31% in 1997, its two best years. There's more than a 60 percentage point difference between the annual returns of the best and worst four years. But even if these extremes are ignored, the standard deviation for the remaining years is a still substantial 11%. This implies a typical year could return anywhere between 0% and 22%.

Even if you exclude all years in which the S&P fell, the standard deviation for all of the positive years is 10%, implying a return anywhere between 6% to 26%.

What all of this means is that getting very precise about where the stock market will end a year from now is an exercise in futility. The probability of getting it consistently right - even within 5 to 10 percentage points - is poor.

Further reading: Everyone Is Bad At This (here).

2. Where To Start: Equities Have A Strong Upward Bias

Just because precise forecasts are impractical doesn't mean we should have no idea what will likely happen to stocks over the next year. There are certain assumptions we can make that can inform our decision making and our expectations. We can use this as a starting point in making investments and adjust as new information becomes available.

The most important fact to always remember is this: stocks in the US have high propensity to rise each year. The S&P has risen in 79% of the years since 1980, and in 72% of the years since 1950. In other words, the long-term historical odds of stocks rising next year are about 2 to 3 times greater than for stocks falling. Equities are fundamentally biased upwards over time.

Why do strategists expect equities to rise every year? Because they usually do.

To read the entire report Please click on the pdf File Below: