Philip Morris International Inc. (NYSE:PM) is slated to report second-quarter 2017 results on Jul 20, before the opening bell.

The question lingering in investors’ minds is whether this tobacco leader will be able to post a positive earnings surprise in the to-be-reported quarter. Its earnings have lagged the Zacks Consensus Estimate in three of the trailing four quarters, with an average miss of 2.3%. Let’s see how things are shaping up for this announcement.

What Does the Zacks Model Unveil?

Our proven model does not conclusively show an earnings beat for Philip Morris this quarter. This is because a stock needs to have both a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) and a positive Earnings ESP for this to happen.

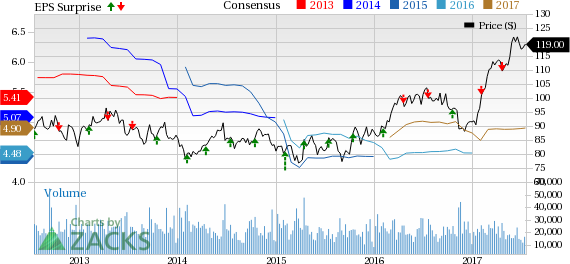

Philip Morris International Inc Price, Consensus and EPS Surprise

Philip Morris International Inc Price, Consensus and EPS Surprise | Philip Morris International Inc Quote

Philip Morris has an Earnings ESP of -1.63% as the Most Accurate estimate is $1.21, while the Zacks Consensus Estimate is pegged higher at $1.23. Although the company’s Zacks Rank #2 increases the predictive power of ESP, we need a positive Earnings ESP in order to be confident about an earnings surprise. You may uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Which Way Are Estimates Treading?

Let’s look at the estimate revisions in order to get a clear picture of what analysts are thinking about the company right before earnings release. The Zacks Consensus Estimate of $1.23 for the second quarter has been stable in the last seven days and reflects growth from $1.15 posted in the prior-year period. However, the same has moved up by a penny to $4.90 for 2017 and also shows growth from $4.48 delivered in 2016.

Further, analysts polled by Zacks expect revenues of $7.06 billion and $28.63 billion for the impending quarter and 2017, which are also 6.2% and 7.3% higher than the respective year-ago periods.

Factors Influencing the Quarter

We note that Philip Morris has been witnessing declining demand for cigarettes due to the ongoing anti-tobacco campaigns, government restrictions and rising taxes on it. In fact, the U.S. Food and Drug Administration (FDA) has also made it mandatory for tobacco companies to use precautionary labels on cigarette packets to dissuade customers from smoking. These regulations adversely impact the company’s performance and, in turn, its overall profitability. Moreover, consumers are currently opting for e-cigarettes or substitutes for cigarettes, thereby affecting cigarette volume. Evidently, the company’s top line lagged the Zacks Consensus Estimate in five of the trailing six quarters, including the last reported quarter.

As smoking rates are declining in developed countries, the race to replace traditional cigarettes is putting pressure on the tobacco industry. Particularly, serious health hazards due to cigarette smoking have pushed consumers toward low-risk, reduced risk products. Therefore, Philip Morris is aggressively investing in creating smoke-free products such as IQOS (Heatsticks that heat tobacco instead of burning it) in order to boost its business and market share. Meanwhile, it continues to benefit from its strong portfolio of tobacco brands and always managed to remain afloat and generate revenues with higher cigarette pricing.

We expect the company’s continued focus on accelerating IQOS volume growth and pricing actions will help it deliver upbeat results in the upcoming quarter as well as in 2017.

Driven by these factors, shares of Philip Morris have rallied 30.1% year to date, comfortably outperforming the Zacks categorized Tobacco industry’s advance of 18.5%. Meanwhile, the broader Consumer Staples sector gained 9.2%.

Stocks Poised to Beat Earnings Estimates

Here are some companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

The Clorox Company (NYSE:CLX) has an Earnings ESP of +0.67% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Tyson Foods, Inc. (NYSE:TSN) has an Earnings ESP of +1.64% and a Zacks Rank #2.

Newell Brands Inc. (NYSE:NWL) has an Earnings ESP of +1.18% and a Zacks Rank #2.

5 Trades Could Profit "Big-League" from Trump Policies

If the stocks above spark your interest, wait until you look into companies primed to make substantial gains from Washington's changing course.

Today Zacks reveals 5 tickers that could benefit from new trends like streamlined drug approvals, tariffs, lower taxes, higher interest rates, and spending surges in defense and infrastructure. See these buy recommendations now >>

Newell Brands Inc. (NWL): Free Stock Analysis Report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

Clorox Company (The) (CLX): Free Stock Analysis Report

Philip Morris International Inc (PM): Free Stock Analysis Report

Original post