Apartment Investment & Management Co. (NYSE:AIV) – commonly known as Aimco – is slated to report second-quarter 2017 results on Jul 27, after the market closes. While its funds from operations (“FFO”) per share are expected to grow year over year, revenues might see a decline.

Last quarter, this residential real estate investment trust (“REIT”) delivered an in-line performance. Results reflected conventional same-store property net operating (NOI) growth, higher contribution from development, redevelopment and acquisition activities, along with higher renewals rate from expiring lease rates. However, the positive was partially offset by the loss of income from apartment sales in 2016.

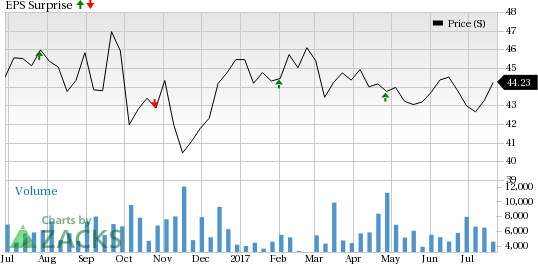

However, Aimco has a mixed earnings surprise history. Over the trailing four quarters, the company surpassed the Zacks Consensus Estimate in one occasion, reported in-line numbers in two and missed the mark in another. Overall, Aimco delivered an average positive surprise of 0.43%. This is depicted in the chart below:

Apartment Investment and Management Company Price and EPS Surprise

Apartment Investment and Management Company Price and EPS Surprise | Apartment Investment and Management Company Quote

In addition, year to date, shares of Aimco have underperformed the industry. While the company’s shares fell 2.7%, the industry gained 5.1% over this period.

Factors to Influence Q2 Results

Aimco has a solid portfolio diversified both in terms of geography and high priced units. The company has been revamping its portfolio through property sales and re-investing the proceeds in select apartment homes with higher rents, superior margins and higher-than-expected growth. This is likely to enhance the quality and expected growth rate of its portfolio in the quarter to be reported.

Also, the company is well on track to strengthen its balance sheet and liquidity position, as well as improve its leverage. Aimco is aimed at boosting its financial flexibility by increasing the pool of unencumbered apartment assets.

However, there is a slowdown in rent growth of Aimco in certain locations due to competition from new supply. In fact, in many markets new lease rent increases have either slowed or turned negative. As such, in the second quarter, this new supply is expected to put pressure on new lease pricing, particularly at the high price point units.

Moreover, even though it is a strategic fit on part of the company to sell non-core assets and buy property in higher-growth in-fill areas, the dilutive impact on earnings from such asset dispositions cannot be bypassed.

For second-quarter 2017, Aimco projects pro forma FFO per share in the band of 56–60 cents. The Zacks Consensus Estimate for the same is currently pegged at 60 cents. This estimate remained unchanged over the past 60 days, reflecting lack of any solid catalyst.

Earnings Whispers

Our proven model does not conclusively show that Aimco will likely beat estimates this season. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. However, that is not the case here as you will see below.

Zacks ESP: The Earnings ESP, which represents the percentage difference between the Most Accurate estimate of 59 cents and the Zacks Consensus Estimate of 60 cents, is -1.67%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter

Zacks Rank: Aimco’s Zacks Rank #2 increases the predictive power of ESP. However, we also need to have a positive ESP to be confident of an earnings beat.

Stocks That Warrant a Look

Here are a few stocks in the REIT sector that you may want to consider, as our model shows that these have the right combination of elements to report a positive surprise this time around:

Liberty Property Trust (NYSE:LPT) , expected to release earnings on Jul 25, has an Earnings ESP of +1.61% and a Zacks Rank #2.

Regency Centers Corp. (NYSE:REG) , likely to release second-quarter results on Aug 3, has an Earnings ESP of +1.12% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

CyrusOne Inc (NASDAQ:CONE) , expected to release quarterly numbers on Aug 2, has an Earnings ESP of +2.70% and a Zacks Rank #2.

Note: All EPS numbers presented in this write up represent funds from operations (FFO) per share. FFO, a widely used metric to gauge the performance of REITs, is obtained after adding depreciation and amortization and other non-cash expenses to net income.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020. Click here for the 6 trades >>

Regency Centers Corporation (REG): Free Stock Analysis Report

Apartment Investment and Management Company (AIV): Free Stock Analysis Report

CyrusOne Inc (CONE): Free Stock Analysis Report

Liberty Property Trust (LPT): Free Stock Analysis Report

Original post

Zacks Investment Research