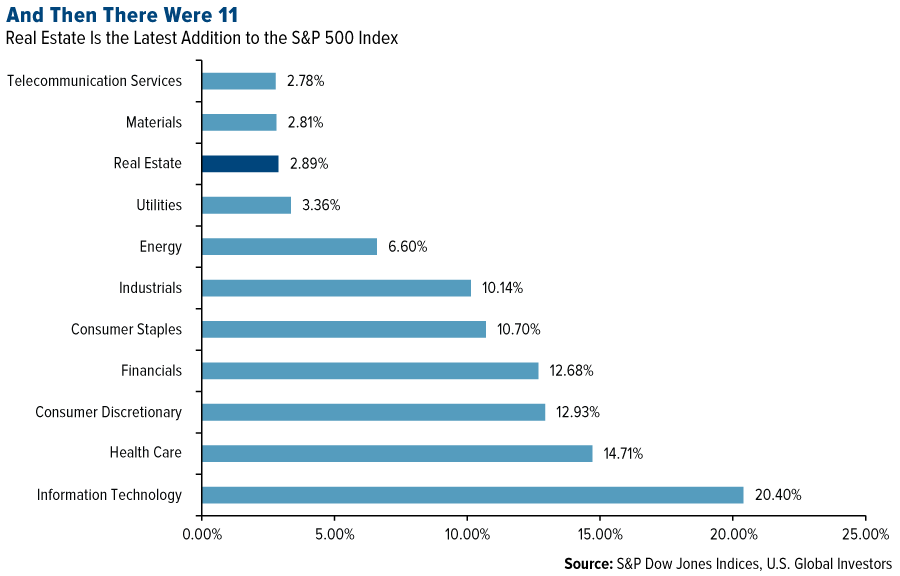

In case you haven’t noticed, the S&P 500 Index is looking a little different these days. Once a sub-industry of the financials sector, real estate now has its own zip code in the universe of blue chip stocks. It’s the first time since 1999 that such a change has been made to the S&P’s composition.

The new sector has a weighting of nearly 3 percent, all of it taken out of financials.

As I told CNBC Asia’s Bernie Lo recently, I think real estate’s promotion will attract more institutional and individual investors to the space. It tells them this is no longer a niche market but one with a distinct and significant presence, with its own unique business drivers.

This has been a long time coming, to be perfectly honest. Ever since the housing and financial crisis, real estate investment trusts (REITs) have been pulling in some serious cash as more become available for trading on the New York Stock Exchange and elsewhere. Altogether, REITs currently have a market cap of over $1 trillion, according to REIT.com.

With investors on the hunt for yield, it’s not hard to see why. As of August 31, the FTSE NAREIT All Equity REIT Index yielded an average of 3.61 percent, compared to the S&P 500’s 2.11 percent.

During 2015, stock exchange-listed REITs paid out a whopping $46.5 billion in dividends.

Builders Rush to Meet Demand

Looking just at the residential housing market, business is definitely booming. With 30-year mortgage rates at below 3.5 percent, the market is scorching hot in many parts of the U.S.—so much so, some builders are reporting a shortage of construction workers to meet demand.

New construction starts rose to 1.2 million in July, beating analysts’ forecasts and suggesting the U.S. housing market appears to have finally made a full recovery, eight years following the recession, with Bloomberg calling this the “strongest home sales since the start of the economic expansion.”

…But Homeownership Is Falling

Trouble could be brewing, however. As I shared with you last month, millennials just aren’t buying homes at the same rate we’ve historically seen from 18- to 34-year-olds. There are many theories as to why this is, from millennials delaying starting families to focus on careers, to a loss of trust in home ownership as a reliable investment or even as an institution, to a preference to rent. This trend has contributed to the lowest U.S. home ownership rate in five decades.

But how can this be? How could there be both massive housing demand and yet declining home ownership?

One answer might lie in population growth. Simply put, there are more of us living in the U.S. than ever before, which translates into more renting and more buying. And with single-person households on the rise every year, a need for additional housing units has become a priority. Whereas one unit would have served a married couple only a few years ago, now two are needed.

Whether you believe this or not, it seems reasonable to expect the new real estate sector to attract assets to the space, as more mutual funds will add to their exposure to better reflect the S&P 500. If anything, it will help investors monitor and track this important segment of the market.

Disclosure: All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Investing in real estate securities involves risks including the potential loss of principal resulting from changes in property value, interest rates, taxes and changes in regulatory requirements. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.