- Fed makes long-awaited pivot towards cutting rates, markets rejoice

- Dow Jones soars to new all-time high, S&P 500 approaches its previous record

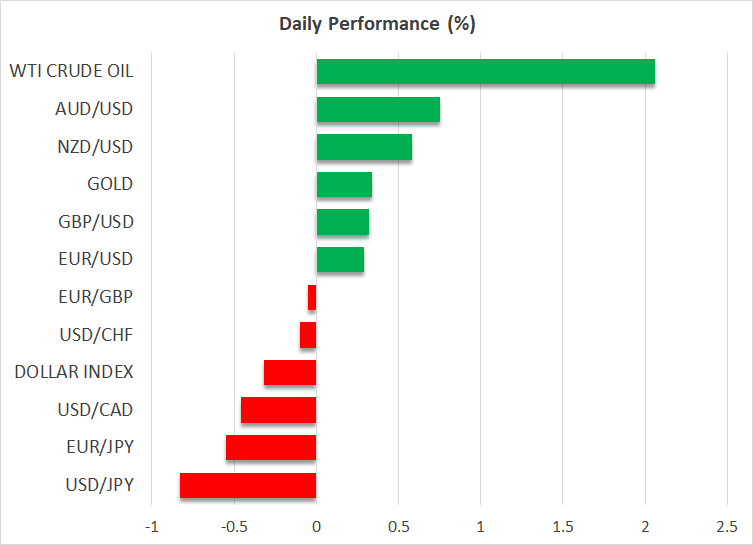

- Dollar takes a dive as Treasury yields sink, gold rallies

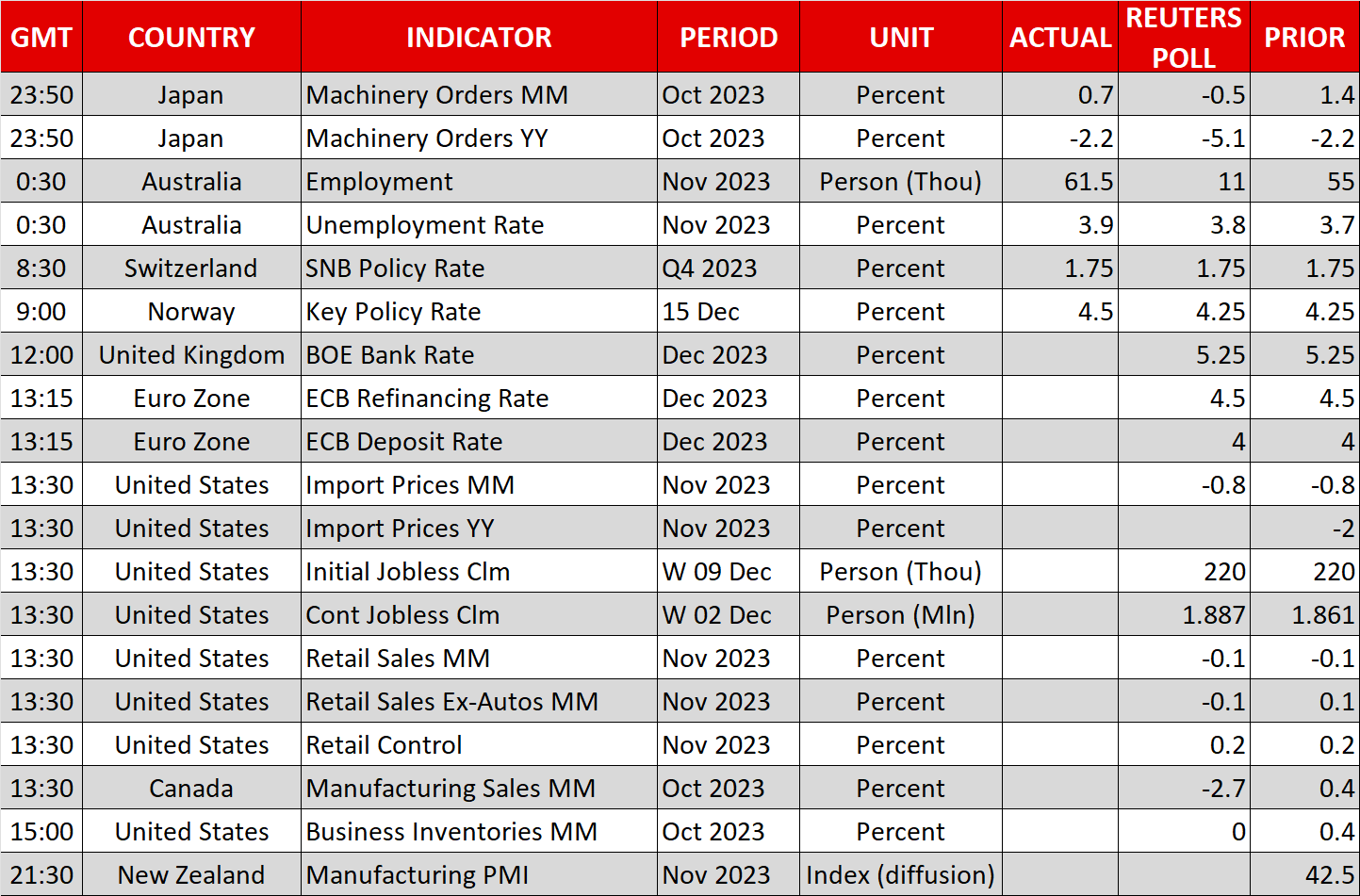

- SNB also holds rates, ECB and BoE decisions coming up next

Powell gives markets what they wanted

The Federal Reserve left interest rates unchanged as expected on Wednesday but struck a somewhat more dovish tone than anticipated, spurring a powerful rally in bond and equity markets. In a marked shift from his previous stance, Fed Chair Jay Powell pointed out that FOMC members are no longer writing down rate hikes in the dot plot, claiming “that’s us thinking we’ve done enough”.

Whilst Powell did not completely rule out more tightening and the statement was tweaked to add “any” before “additional policy firming”, he couldn’t be clearer in his press conference by saying that a rate hike “is not the base case anymore” in what was music to markets’ ears.

It seems that the latest declines in both consumer and producer price inflation this week offered policymakers the reassurance they were seeking that no further adjustment is needed in their policy settings. Powell even suggested that some officials revised their dot plot forecasts after the CPI and PPI data.

Following last Friday’s slightly hotter-than-expected payrolls report, there were doubts as to the extent of any dovish lean. But Powell acknowledged for the first time that rate cuts are now coming “into view”, and this was underscored by the updated dot plot that showed Fed officials pencilling in a total of 75 basis points of cuts for 2024, while the median projection was lowered by 50 bps compared to September.

This fell short of market expectations of between 100 and 125 bps cuts in the run up to yesterday’s meeting but was nevertheless enough for traders to run wild with their dovish bets and they’re currently pricing in almost 150 bps of cuts over the next 12 months.

Santa comes early for Wall Street

Stocks on Wall Street jumped higher on what appears to have been the dovish pivot that markets had been waiting for. With growth slowing, inflation on the way down but a labour market that’s yet to crack, the US economy might just pull off a soft landing.

For equity markets that have had a very bumpy couple of years, this was the best outcome they could have hoped for. The Fed has now likely triggered a Santa Claus rally that looks set to put stocks on the front foot at the start of the new year.

What’s striking, however, is that the Dow Jones Industrial Average, made up mainly of traditional stocks, is the biggest winner in the post-FOMC rally. Having lagged the other indices for much of the year, the Dow Jones shot up 1.4% yesterday to close at a new all-time high, finishing above the 37,000 level for the first time.

The S&P 500 wasn’t far behind, coming within 2% from its record high, but the Nasdaq Composite still has some way to go before closing in on its 2021 peak.

Dollar under pressure as yields plummet, gold cheers dovish Fed

The sharp drop in bond yields, not just in US Treasuries but globally as well, fuelled the risk-on sentiment, but was anathema for the US dollar. The 10-year Treasury yield has plunged below 4.0% for the first time since August, pulling the dollar index to four-month lows.

Lower yields and a sliding dollar lifted gold prices, however, as the precious metal attempted to recoup its December losses, setting its sights on its all-time high from the start of the month.

Euro and pound in shaky rebounds ahead of ECB and BoE decision

The euro is heading for its third straight day of gains against the greenback, climbing above $1.09. However, there is a danger that it could come under pressure from the European Central Bank’s decision later today. If the ECB makes a dovish pivot of its own, this may seriously cap the euro’s advances, especially if the Eurozone data remains far weaker than the US data.

The pound’s uptrend is also questionable following this week’s poor UK GDP numbers, although what’s different for the British currency is that the Bank of England will probably be the last to begin cutting rates.

The BoE is expected to keep rates unchanged today and will likely reiterate its higher for longer message. The risk for sterling is if the BoE statement emphasises the deteriorating growth outlook, though for now, it is extending its rebound to the $1.2660 area.

Swiss franc slips on SNB currency shift, aussie and kiwi rally

The Swiss franc was broadly weaker on Thursday despite the Swiss National Bank warning that inflation in Switzerland may edge up in the coming months. The SNB kept rates unchanged and opened the door to cuts, but Chairman Jordan signalled that the Bank will ease up on the sale of foreign currency reserves, pressuring the Swissie, which last stood at 0.9491 to the euro.

The aussie was the biggest gainer from the greenback’s woes, rising to 4½-month highs above $0.67 on the back of stronger-than-forecast employment figures out of Australia today. The kiwi also shone even though the New Zealand economy unexpectedly contracted in the third quarter, boosting RBNZ rate cut bets.