- S&P 500 closes at all time high as yields fall after Treasury cuts borrowing estimate

- But worries grow about China’s economy amid Evergrande fallout

- Euro steadies as Eurozone dodges a recession

- Dollar and gold hold within range as ME crisis, Fed angst keep investors one edge

Another day, another record for Wall Street

Shares on Wall Street surged on Monday after the US Treasury said it will borrow less in the current quarter than what it had estimated back in October. The announcement took many investors by surprise, sparking a relief rally, as the Treasury Department was widely expected to slightly increase its borrowing requirements amid a burgeoning budget deficit.

Treasury yields declined across the board, with long-dated yields falling the most, led by the 10 year, which is close to slipping below 4.0% today. The new borrowing plan sees debt rising by $760 billion in the first quarter versus the earlier forecast of $816 billion. More details on quarterly refunding will follow on Wednesday when the Treasury is anticipated to maintain its estimate of a higher issuance of long-term notes and bonds.

Wall Street eyes Big Tech earnings, shrugs off China gloom

The drop in yields just ahead of the slew of Big Tech earnings releases and the Fed’s policy decision potentially sets the stage for a week-long rally for US equities should there not be any negative surprises.

Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOGL) and AMD (NASDAQ:AMD) are scheduled to report after today’s market close and with all three stocks trading at all-time highs, they are vulnerable to a sharp correction if any element of their earnings figures questions their lofty valuations.

Both the Dow Jones and S&P 500 ended Monday's session at record highs. The Nasdaq 100 closed at an all-time high too, though it failed to match last week’s intra-day peak.

The optimism wasn’t shared in Asia, however, as Chinese indices slumped again despite the recent support measures announced by authorities. The liquidation order for Evergrande has cast another cloud over China’s economic prospects, upping the pressure on Beijing to formulate a large fiscal stimulus package, as investors have so far been unimpressed by the drip-feed approach.

Rate cut signals awaited

The outcome of Wednesday's FOMC decision will also be crucial for equities this week amid the frenzied speculation about how soon the Fed will cut rates. The odds for a March cut have slid slightly below 50% following a string of solid economic data as well as some pushback from Fed officials. With the economy performing so well, it’s hard to see Chair Powell explicitly signalling a rate reduction in March, or even May, but he is unlikely to rule it out either.

For the markets, that could be enough to prop up the positive sentiment as long as Powell sounds confident that achieving the inflation mandate is within sight. Moreover, any hints about putting an early end to quantitative tightening could also cheer investors.

Gold and dollar battle it out amid geopolitical flare up

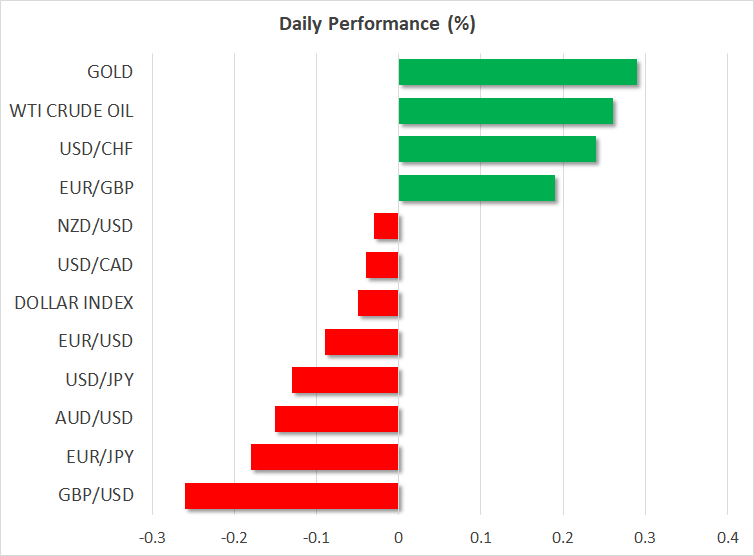

The US dollar has been mostly rangebound lately against a basket of currencies as investors await more clues on the path of interest rates before deciding on the next move. However, much of the support for the greenback is coming from safe-haven flows rather than from bets that the Fed won’t cut rates soon. The worsening economic outlook in China and the Eurozone, combined with the escalating conflict in the Middle East are boosting demand for the world’s reserve currency, even as yields slide.

Washington has pledged to respond to the killing of three American soldiers in a drone attack on Sunday in Jordan, while attacks by Houthi rebels in the Red Sea continue.

Gold has been attempting to make a fresh upside move this week on the back of the heightened geopolitical tensions but a firm US dollar has been getting in the way.

Tepid support for euro from GDP surprise

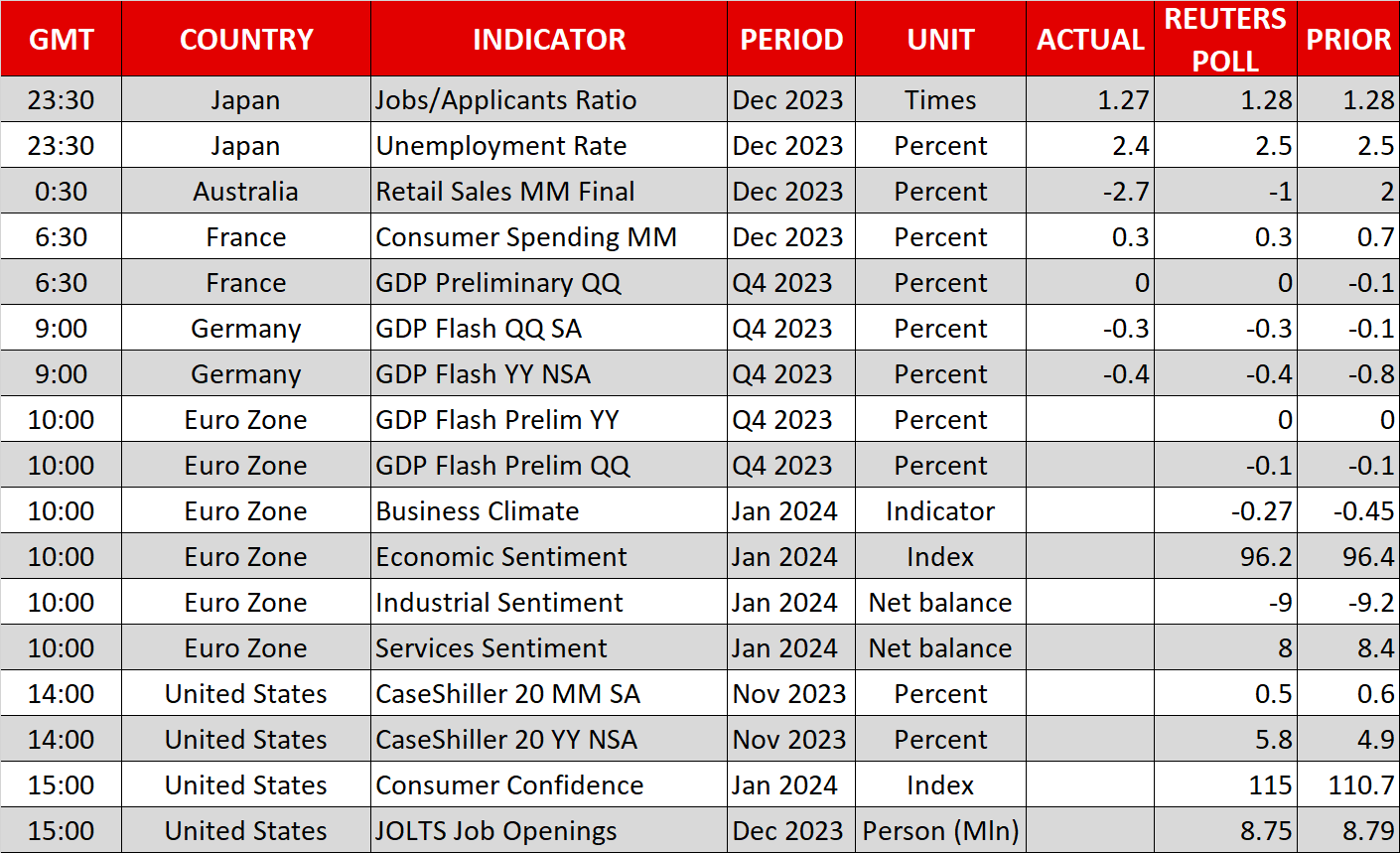

The euro remained on the backfoot on Tuesday, though it was somewhat steadier after the preliminary GDP estimate for the final quarter of 2023 showed that the Eurozone economy narrowly avoided a technical recession. Growth in the euro area was flat in Q4, beating expectations of a 0.1% contraction. However, any relief is likely to be short-lived as data for German GDP wasn’t quite as positive, with Europe’s largest economy shrinking by 0.3%.

The Australian dollar was oddly resilient on Tuesday despite the negative China headlines, while the kiwi spiked higher on hawkish remarks by the RBNZ’s chief economist earlier in the day.