This article was originally published at TopDown Charts

Executive Summary

-

Treasuries are expensive, but near-term indicators like technicals, sentiment and seasonality suggest there’s further to go.

-

We could possibly say the same about equities and property as valuations reach unnervingly familiar levels amid the wash of global liquidity.

-

Commodities continue to present a longer-term bullish case.

Equities Increasingly Expensive

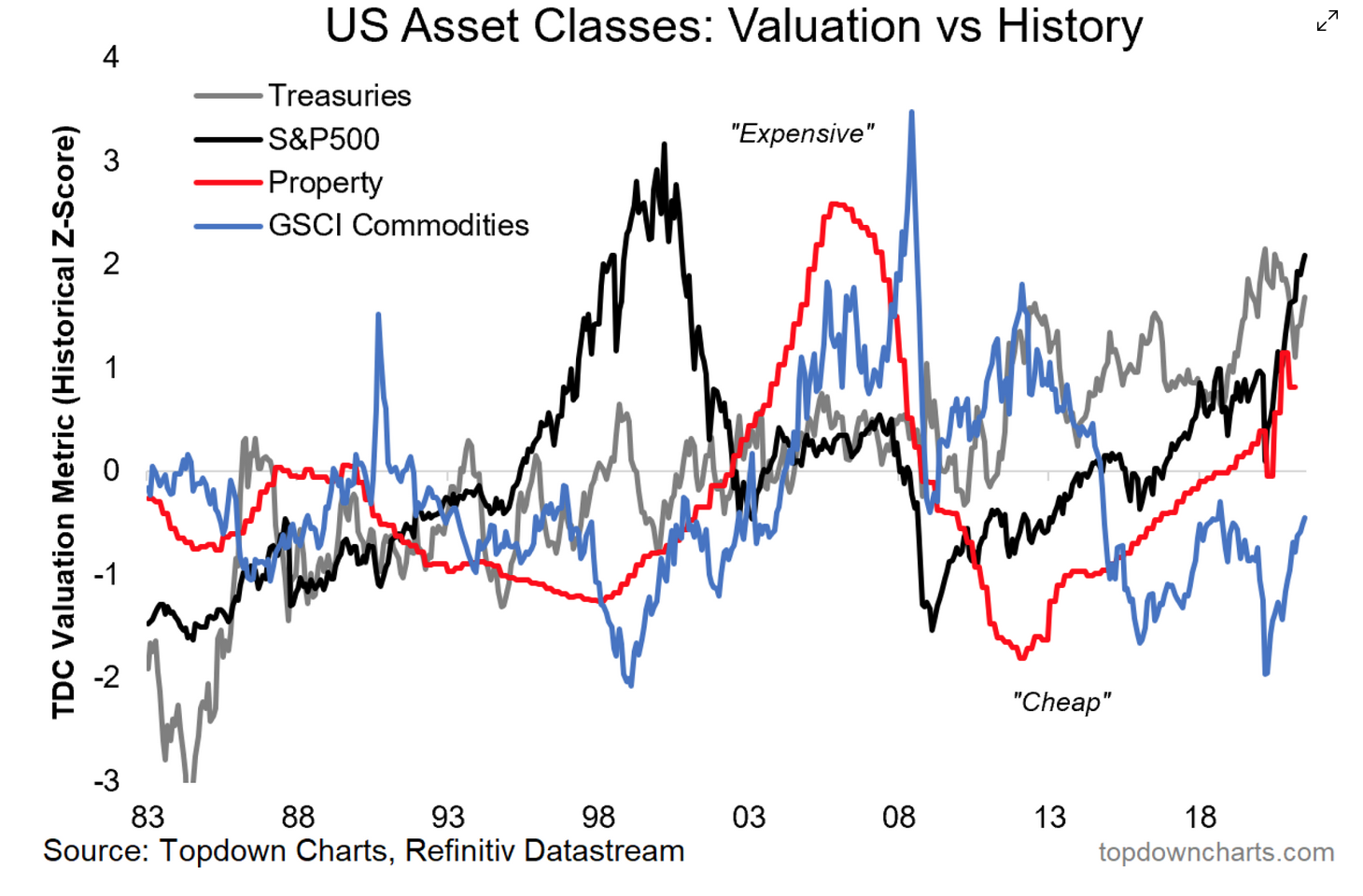

Putting money to work in an asset class has not gotten any easier this year. The S&P 500 has soared to new all-time highs of late and global markets, while trading at reasonable valuations, are significantly off their 2020 nadirs. One equity valuation metric we track is the global PE10 breadth. It shows that more country stock markets feature PE10s in the 10-25x range ("expensive") versus the 10-15x range ("cheap") for the first time in many years. Value has eroded. Where to turn?

Treasuries Increasingly Expensive, But Might Catch A Tailwind

In the fixed income space, the emerging rally in bonds with the U.S. 10-year yield falling from its Q1 high near 1.74% to under 1.30% at times last week (a 5-month low) presents challenges to investors looking to find a cheap asset class in safe securities. But we see near-term bullish trends in Treasuries.

We noted that the U.S. 10-year yield failed at climbing through resistance earlier this month. The bond bulls are also excited about near-term seasonality—the U.S. 10-year rate tends to fall now through early Q4. Longer-term, however, low yields today make for expensive valuations and weak expected real returns.

Real Estate Too Hot To Handle

What about real estate? The U.S. property market is “on fire,” as has become common terminology. A variety of macro and demographic factors are at play, while low interest rates have made U.S. housing market valuations particularly sky high.

Commodities Still Somewhat Cheap

Another asset class up our sleeve are commodities. The GSCI Commodity Index features a Z-score (a measure of the current valuation versus history) that is below 0. Other asset classes listed above are one to two standard deviations more expensive than their historical average, according to our preferred valuation metric as shown in the Chart of the Week.

Chart Of The Week: U.S. Asset Classes: Valuation vs. History

Our Weekly Macro Themes report turned bullish on commodities on March 20, 2020, and the thesis has worked well over the last 16 months. Recently, commodities like lumber and copper have pulled back, while oil prices have sustained their bull market into the third quarter. Oil typically rallies during the first half of a year, then meanders in Q3. We’ve seen that already with WTI pulling back last week.

Commodity Rotation

Could there be more commodity rotation on the way? Precious metals present an interesting case. The Weekly Macro Themes report outlines how defensive assets perform from July through December in the average year. Gold tends to do well in August and September as the U.S. dollar is sometimes under pressure. Some momentum has already emerged with gold rallying three straight weeks.

A Tough Period for Risky Assets—Treasuries Often The Safe Haven

The third quarter is notorious for bringing about volatility in stocks and high yield bonds, while the VIX tends to trough in mid-July then spike in early October. Both equities and credit-sensitive fixed income appear expensive in absolute terms and seasonality is generally negative for both areas. We see elevated downside risk over the coming months while Treasuries present a compelling Q3 case.

What could drive the risk-off price-action? Several macro factors are at play including more Fed taper headlines, COVID virus mutation & resurgence risks, and higher expectations for economic/earnings figures.

That’s a near-term scenario. Longer-term, investors should expect muted returns from Treasuries, the S&P 500, and U.S. property. The commodity index could offer returns in addition to its usual diversification benefits.

Conclusion

The recent drop in global bond yields leaves investors hungry for return opportunities. We see equities as still being reasonable compared to expensive bonds, but pricey on a nominal basis. U.S. property is in a similar camp. The last pocket of value outside of some global equities markets is commodities. In the near-term, U.S. Treasuries may have further upside.

You can see Mike Zaccardi's original post here.