At this point, I don’t think I really need to say that Trump 2.0 is a lot different than Trump 1.0. And one of those differences—which very few people are talking about—is a huge tailwind for the two big dividends we’re going to dive into today.

Think back to our first go-’round with Trump. Remember his relationship with Jay Powell? Terrible, right?

Back in 2018, he tweeted that Powell and the Fed had “no sense, no guts, no vision” when they failed to cut rates as much as the president wanted. A year later, he called Powell an “enemy.”

And that’s just a small sample of the torment unleashed upon poor Jay! No doubt our man couldn’t wait to get home at night so he could turn off his phone.

These days? Crickets.

While there has been the odd jab, Trump has said that he’d let Jay serve out his term, which ends in May 2026. When Powell and the Fed held rates steady in early February, Trump said it was “the right thing to do.”

Out With the “Short” Rate, In With the “Long”

Why the change?

I think it has a lot to do with Treasury Secretary Scott Bessent, who’s straight-up told us that it’s the 10-year Treasury rate (the so-called “long” end of the yield curve) that he and Trump are focused on, not the “short” end (which is controlled by the Fed).

This has been mostly overlooked in the media. But it’s a critical detail when it comes to dividend stocks. Here’s why.

Bessent has said he aims to bring down “long” rates—and the interest rates on most consumer and business loans with them. He has a three-part strategy that he’s articulated:

- Tariffs (which, as we’ve written before, aren’t inflationary because they act as a drag on economic growth).

- Drilling—to bring down energy costs.

- Deregulation—also to bring down costs (see “drilling” above), but in this case to lower the cost of doing business, while boosting productivity.

Another tailwind for the long rate? A softer labor market, due in part to DOGE. That’s already happening, with the number of layoff notices issued in February jumping 245% from January, hitting levels not seen since June 2020, according to outplacement firm Challenger, Gray & Christmas.

The 10-year has taken note: Even with the slight increase we’ve seen over last week’s tariff drama, it’s down sharply since Bessent was appointed:

10-Year Takes Its Cue From Bessent …

Of course, this isn’t all due to Bessent—we’re also seeing signs of a slowing economy, including the latest reading from the Atlanta Fed’s GDPNow indicator, pointing to an annualized 2.8% drop in the first quarter.

We don’t have to get any further into the weeds here, because the upshot is this: The narrative that tariffs will cause “inflation forever” is dead. I think we’re likely to see a quicker shift to lower rates—with the Fed and the 10-year—than most people think.

And when rates fall, bonds—and bond proxies—jump.

… And so Does This Core CIR Holding

Total Return")

Managed by Dan Ivascyn—known as “the Beast”, with strong track record and deep connections in Bond-land—this corporate-bond focused closed-end fund (CEF) kicks out a 13% yield that’s due to get a lot more attention as rates drop. Especially when you consider that PDI (OTC:IDXG) pays monthly, and its payout is as steady as they come.

No Way Investors Will Ignore This Steady 13% Dividend as Rates Fall

")

Source: Income Calendar

One note of caution here: PDI is now trading at a higher-than-average premium to NAV, so we’re not recommending new buying (see below to learn how you can get an update when we flip this one back to a buy).

Meantime, there are some other “bond proxies” almost certain to see a nice lift as rates drop: utility stocks. Most have been stuck in neutral since Bessent took the job at Treasury, so unlike PDI, we’ve still got room to buy here.

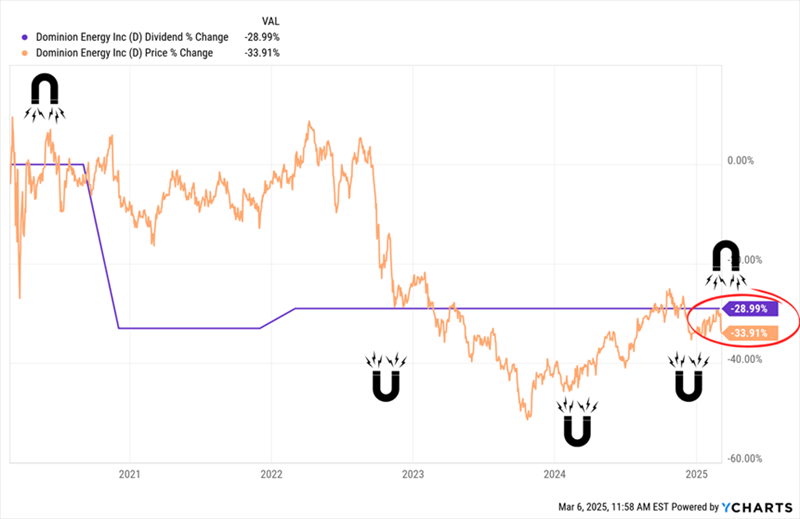

Take Virginia-based Dominion Energy (NYSE:D), with 4.5 million power customers across 13 states. It’s another CIR pick, yielding 4.9%. Unlike PDI, it’s largely moved sideways as the 10-year Treasury rate declined:

Dominion’s “Disconnect” Is an Opportunity (SO:FTCE11B)

Total Return")

Virginia is important here: It’s ground zero for the data-center boom that continues to support AI’s growth.

Remember DeepSeek? I know that seems like a year ago, but my take on it remains the same: The power miser of chatbots will, if anything, drive more AI adoption overall. So our electricity story here remains intact.

What’s more, ChatGPT recently dropped its latest version, ChatGPT 4.5, which was trained on more data than the previous version, boasts a range of new features (including a more conversational interface) and, yes, uses even more computing power than the previous version.

And it’s not just AI: Electric cars continue to hit the road, too. And more consumers continue to look to heat pumps over oil and gas furnaces.

According to the Air Conditioning, Heating and Refrigeration Institute, shipments of central air conditioners and air-source heat pumps jumped 11.8% last year, to 9,681,770 units. Compare that to oil and gas furnaces, which rose just 4.1%. Total shipments were also far behind air conditioners and heat pumps: just 3,120,677. This shift is clearly baked in, no matter what happens in Washington.

Dominion is likewise projecting a doubling of demand for its power by 2039. That said, we are, as mentioned, mainly looking to the stock as a play on lower rates.

Income investors look to “Big D” for the stock’s 4.9% yield, more than four times the 1.2% the typical S&P 500 stock pays and far ahead of the 2.9% you’d draw from the typical utility. Still, the income crowd hasn’t fully warmed back up to the stock after management cut its payout in 2020.

The share price levitated for a while, as you can see in the chart below. But the “Dividend Magnet”—or the tendency of a stock to follow its payout (higher or lower)—eventually kicked in here.

Dominion’s “Lagging” Stock Sets It Up for Gains

Now, with the stock now falling behind the payout growth, it looks ripe for more upside.

Why the 2020 dividend cut? Too much debt, of course. Dominion had embarked on an acquisition binge in the name of growth. Which, ironically, backfired.

The result was a rare payout slash from a utility—an income investor’s worst nightmare. That’s why first-level investors are still a little hesitant around “Big D,” even with the favorable rate setup we have materializing before us.

“Safest Dividend Is Often the One Recently Cut”

With dividend cuts, it’s key to bear in mind that chief financial officers are like carpenters. It’s best if they measure twice and cut only once. As a result, the safest dividend is often the one recently cut. Unless management is a complete clown show (which Dominion’s is certainly not), the last thing they want is to be forced back into that particular dentist’s chair!

A final boost for the bottom line: Lower rates will cut D’s borrowing costs, too.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, "7 Great Dividend Growth Stocks for a Secure Retirement."