Torchmark Corporation (NYSE:TMK) remains poised for growth, given its niche market focus, strategic acquisitions, strong operating fundamentals and the ability to generate decent cash flows. The Zacks Rank #3 (Hold) life insurer looks promising, banking on a number of growth drivers.

Growth Projections: The Zacks Consensus Estimate for earnings per share is $4.75 on revenues of $4.1 billion for 2017. While the bottom line reflects 4.1% growth, the top line shows a year-over-year increase of 4.7%. For 2018, the Zacks Consensus Estimate for earnings per share is pegged at $5.08 on revenues of $4.3 billion. The bottom line reflects 6.9% growth, while the top line represents a 4.0% year-over-year rise.

Torchmark has long-term expected earnings per share growth of 7.2%.

Northbound Estimates: The Zacks Consensus Estimate for 2017 has inched up 1.1% in the last 60 days, while the same for 2018 has nudged up 1.0% over the same time frame.

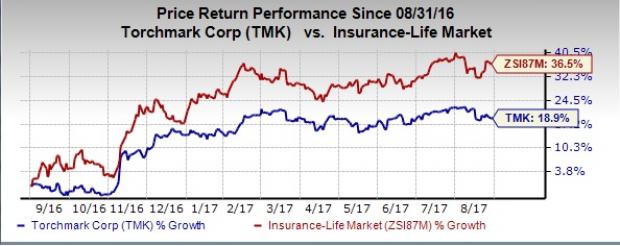

Price Performance: Although Torchmark’s shares have rallied 18.9% in a year, it substantially underperformed the industry’s surge of 36.5%. The shares however have outperformed the S&P 500, increasing 12.5% over the same time frame.

Positive Earnings Surprise History: Torchmark has surpassed the Zacks Consensus Estimate in the last four quarters. The company’s average four-quarter surprise is 2.21%.

Growth Drivers in Place

Torchmark’s most important distribution channel — American Income Exclusive Agency — has been largely contributing to the company’s life premium and net sales. The company projects life sales growth in the range of 6-10% in 2017.

The company is focusing on expanding margins rather than improving sales or sales levels or margins as a percentage of premiums. Health sales are expected to grow 7-11% in 2017.

Torchmark now expects net operating income between $4.70 per share and $4.80 per share in 2017, on the back of better-than-expected underwriting income and an increase in investment income.

A strong capital position should further help the company return value to shareholders. It has also been consistent in generating free cash flow and estimates the same between $325 million and $330 million in 2017. The company has also generated 83% returns for investors over the past 10 years, thanks to a judicious capital management strategy.

Stocks to Consider

Some better-ranked insurance stocks are Manulife Financial Corp. (NYSE:MFC) , Sun Life Financial Inc. (TO:SLF) and Health Insurance Innovations, Inc. (NASDAQ:HIIQ) .

Sun Life is the third largest insurer in Canada providing protection and wealth management products and services to individual and group customers worldwide. The company flaunts a Zacks Rank #1 (Strong Buy). It delivered positive surprises in all the trailing four quarters with the average beat being 10.53%. You can see the complete list of today’s Zacks #1 Rank stocks here..

Health Insurance Innovations develops, distributes and administers cloud-based individual health and family insurance plans, plus supplemental products in the United States. The stock sports a Zacks Rank #1. The company delivered a four-quarter average positive surprise of 87.49%.

Manulife is one of the three dominant life insurers within Canada, providing financial advice, insurance, and wealth and asset management solutions to individuals, groups and institutions in Asia, Canada and the United States. The company carries a Zacks Rank #2 (Buy) and delivered a four-quarter average positive surprise of 11.08%.

One Simple Trading Idea

Since 1988, the Zacks system has more than doubled the S&P 500 with an average gain of +25% per year. With compounding, rebalancing and exclusive of fees, it can turn thousands into millions of dollars. This proven stock-picking system is grounded on a single big idea that can be fortune shaping and life changing. You can apply it to your portfolio starting today. Learn more >>

Torchmark Corporation (TMK): Free Stock Analysis Report

Manulife Financial Corp (MFC): Free Stock Analysis Report

Health Insurance Innovations, Inc. (HIIQ): Free Stock Analysis Report

Sun Life Financial Inc. (SLF): Free Stock Analysis Report

Original post

Zacks Investment Research