Stocks are climbing a wall of worry, which is a hallmark of bull markets. Higher equity prices really do require fear!

Today we’ll highlight the least-liked stocks on Wall Street. Why? Because each analyst has nothing to do but upgrade these plays from here. As always, we’ll focus on big dividends—I’m talking about yields starting at 6% and going all the way up to 24%.

Let’s recap our profitable sources of fear. First, the broader market per one of our preferred “vanilla gauges”:

Source: CNN Fear & Greed Index

While retail investors are fearful, analysts at large are quite bullish. At least on paper.

Professional stock analysts are optimistic by default. They know exactly who butters their bread, so it’s hard to make a living by unabashedly slamming most of their coverage universe.

How optimistic are we talking? As I write this, nearly 400 of the S&P 500’s companies have consensus Buy ratings. And virtually all of the rest are merely considered Holds. In fact, right now, only a single S&P 500 component is considered a Sell by Wall Street’s brightest minds.

One Hated Blue Chip. One.

We contrarians prefer stocks with Sell ratings. When this happens, there are nothing but upgrades to follow!

Let’s begin with Franklin Resources (NYSE:BEN) (BEN, 6.1% yield). Better known for its operating business, Franklin Templeton, this isn’t just one of the world’s largest investment managers—it’s a Dividend Aristocrat with 44 years of payout hikes under its belt, including a raise just a couple of months ago. While BEN has a lot more Hold calls than Sell calls, it doesn’t have a single Buy rating to its name, and that’s still extremely bearish for the analyst set.

Why did Franklin Resources draw my attention? Because it was a little less than five years ago that I lumped it in with a few other “zombie dividends” that were “probably dead money at best.”

And In Fact, It Was.

The problem back then? Net outflows. The problem today? Net outflows. But the story has changed – today, outflows are being heavily driven by Franklin-owned fixed-income manager Western Asset Management Co. (WAMCO) unit, whose star bond manager, Ken Leech, has been charged with fraud. WAMCO has suffered massive redemptions from the likes of the California State Teachers’ Retirement System, Ohio’s Bureau of Workers’ Compensation and the Chicago Teachers’ Pension Fund.

Franklin is working on expense reductions. It actually has a promising, growing alternative business. And it still saw fit to upgrade its dividend at the end of 2024. There’s not nothing here. But given the low visibility into when exactly the WAMCO-related bleeding will stop, it’s no surprise the pros have little appetite for this Aristocrat right now.

Less scandal-plagued is Suburban Propane Partners LP (NYSE:SPH) (SPH, 5.9% yield), a national propane supplier that serves more than 700 communities in 42 states. The view from 10,000 feet isn’t exactly attractive—this master limited partnership’s (MLP) units have been cut by 60% since 2011 amid a volatile longer-term downtrend in the price of propane. The stock is not heavily covered by Wall Street, but it’s a polarizing play that sports twice as many Sell calls as Buy ratings and not a single Hold.

The pros might be spurred into action. I last discussed SPH in the back half of 2023, saying that a return to colder weather and a heightened interest in yield should drive interest in the propane stock, and indeed it did. Shares have delivered a total return of 60% since then, including a big pop to start 2025 on the back of cold snaps across the U.S. and resurgent propane prices.

Propane Has Peaked a Little Higher in Each of the Past Two Years

But the risk/reward picture has gotten blurrier—SPH’s yield is much less than it was in 2023 (~9% then vs. ~6% now) and coverage is tighter, at about 70%-85% across a range of expected earnings for this year.

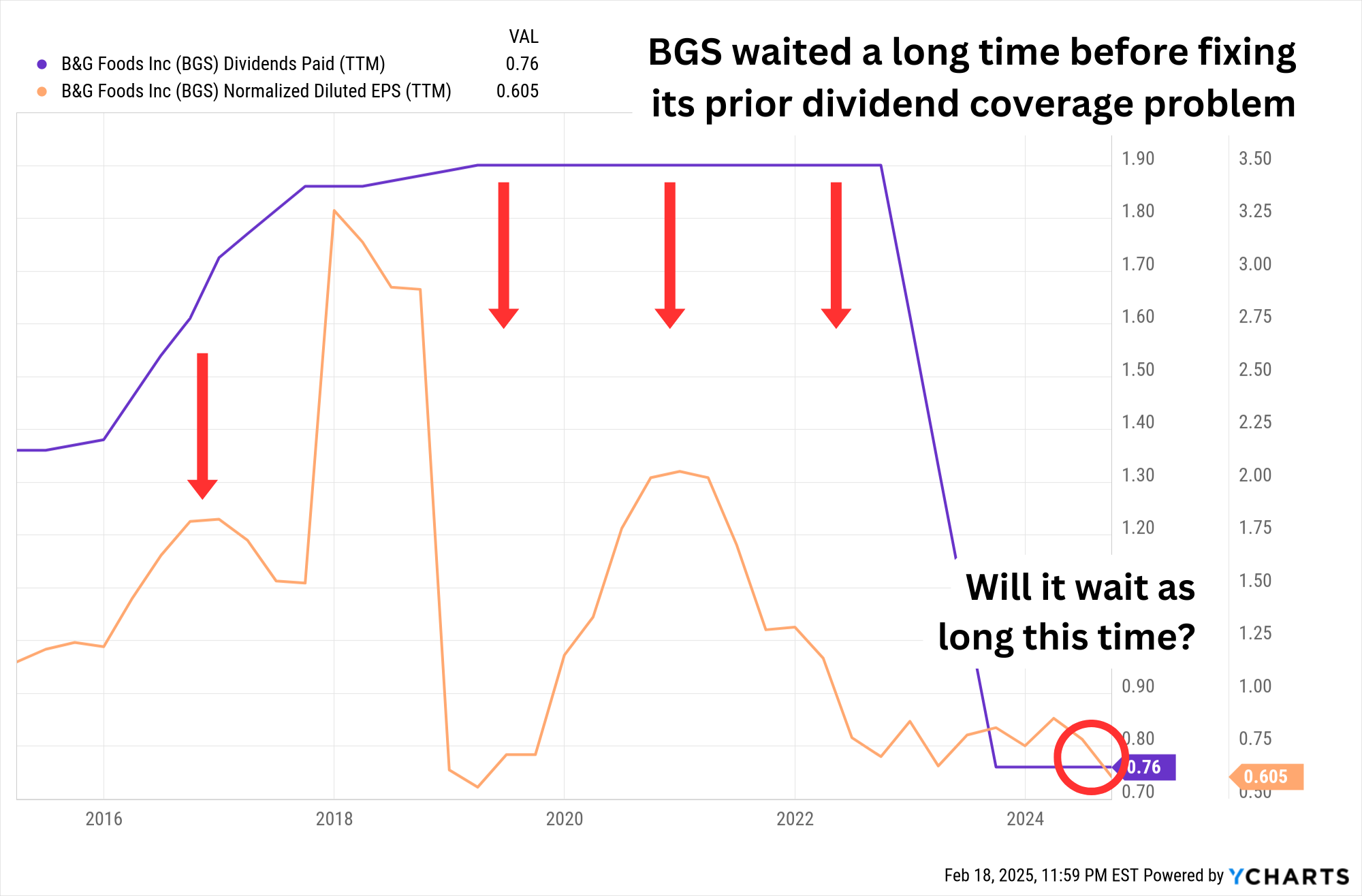

B&G Foods (NYSE:BGS) (BGS, 12.1% yield) is a smallish consumer-staples name with a few well-known brands that include Crisco, Cream of Wheat, Ortega, and Bear Creek. And it’s an example of how to get a bigger yield the wrong way.

BGS’s yield has rocketed from below 9% in early November to north of 12% right now—without a dividend hike. Instead, we can chalk it up to a 33% stock drop triggered by a dreadful Q3 earnings report and guidance cut.

Analysts are more cautious than outright hostile toward BGS, but five Holds and two Sells against no Buys is still a plenty-bearish consensus. The pros expect 2024 to end with a thud (profits down 30% to an adjusted 69 cents per share), followed by a flat-to-down 2025 (67 cents).

This could be a real problem for the dividend, given that at current levels, BGS pays out 76 cents.

And There’s Precedent—BGS Cut Its Dividend by 60% in 2022

I’m going to briefly mention Prospect Capital (NASDAQ:PSEC) (PSEC, 12.1% yield) because it needs saying: We have repeatedly warned about PSEC here, including in October 2024—just a couple of weeks before it announced yet another dividend cut. This time, it hacked away 25% of its monthly payout, bringing it from 6 cents to 4.5 cents per share.

Prospect Capital comes up on a lot of investor screens because it’s perpetually cheap (57% of NAV right now!) and, despite all the cuts, it almost always sports an eye-popping yield (12%+ right now). I wouldn’t directly bet against it—I think the administration could be favorable for business development companies (BDCs) like PSEC—but I agree with Wall Street, which has the stock as a consensus Sell.

I couldn’t pass up the chance to talk about a 20%-yielder, which is what we have in ZIM Integrated Shipping Services (NYSE:ZIM) (ZIM, 24.2% yield). Israel-based ZIM is a global container liner shipping company that serves more than 32,000 customers across 300 ports in 90 countries. It’s also a relatively young public issue—the company launched its IPO roughly four years ago.

And on a Total-Return Basis, ZIM Has Beat the Pants Off the Market

But Wall Street thinks that’s just about enough. Five Sells against two Holds and no Buys? That’s about as bearish as they get. It’s not for nothing: Container spot rates are falling, and the outlook remains negative, in part because tariffs could depress international cargo demand. Also worrisome? ZIM has been ramping up capital investments, which has resulted in net debt spiking from a little more than $1 billion in 2022 to $3.5 billion today. ZIM is only worth $2.4 billion by market cap!

Shipping stocks are extremely cyclical, too—it’s not unusual for stocks in this space to collapse by 50% or more before bouncing back. So while the pros see a massive downturn coming for ZIM, that could just be par for the course before the next cycle whisks the stock higher again. This is why would-be dividend dip buyers should know exactly what they’re in for.

This Dividend Is Just as Volatile as the Stock!

ZIM technically has a quarterly dividend policy, in which it will distribute “on a quarterly basis at a rate of 30% of the net quarterly income of each of the first three fiscal quarters of the year, while the cumulative annual dividend amount to be distributed by the Company (including the interim dividends paid during the first three fiscal quarters of the year) will total 30-50% of the annual net income.”

But ZIM paid three dividends in 2024, including a special and regular distribution in December. It paid just once in 2023. And as the chart shows, how much it pays is all over the place.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, "7 Great Dividend Growth Stocks for a Secure Retirement."