By Jesse Colombo

U.S. inflation expectations have surged over the past few months, and this has been a bullish driver for gold and silver.

Yesterday, the U.S. Consumer Price Index came in hotter than expected, reinforcing those inflation concerns and raising the specter of stagflation as economic growth slows and layoffs increase.

While these developments are troubling for the broader economy, they create a highly favorable environment for precious metals, which I will explore in this article.

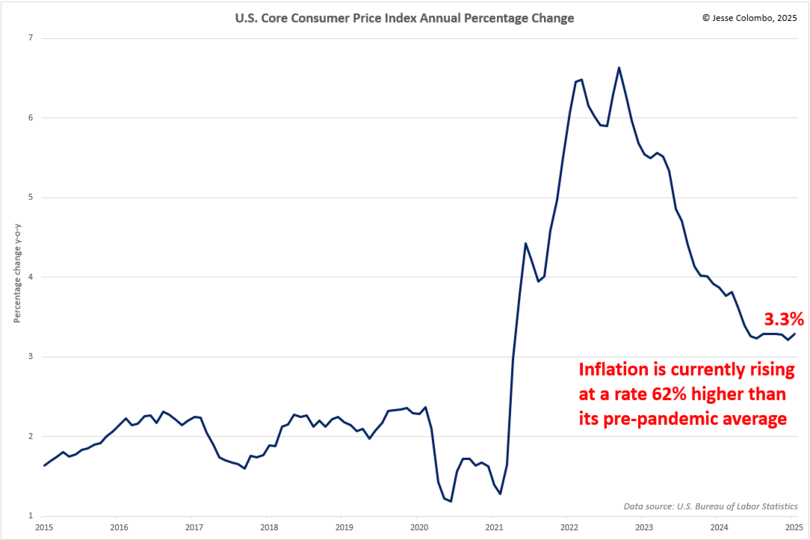

Yesterday's report showed that the Consumer Price Index (CPI) rose at an annual rate of 3.0% in January, surpassing the expected 2.9%. Meanwhile, the core CPI, which excludes volatile food and energy prices, climbed 3.3% annually—higher than the anticipated 3.1%.

The Federal Reserve generally targets a 2% inflation rate, yet as the chart below illustrates, core CPI annual growth rate remains persistently elevated, standing 62% above its pre-pandemic average.

Adding to concerns, January’s data was recorded before President Trump’s tariffs took effect, suggesting inflationary pressures could intensify in the coming months.

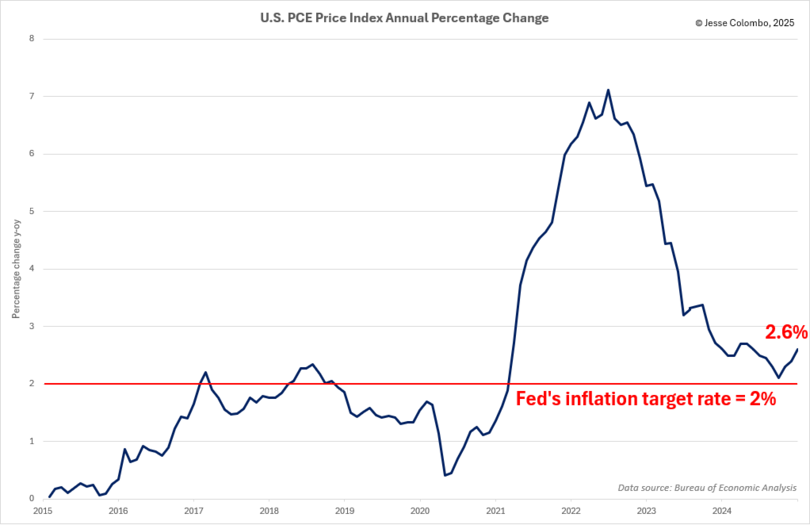

While the Consumer Price Index (CPI) is the most widely recognized measure of inflation, the Federal Reserve’s preferred gauge is the Personal Consumption Expenditures (PCE) price index.

In December, the PCE rose at an annual rate of 2.6%, reinforcing the same message as the CPI—inflation remains persistently high and has been trending in the wrong direction in recent months.

The increase in the inflation rate was anticipated by several inflation expectation indicators, including the 5-year inflation breakeven rate, as shown in the chart below.

This rate, calculated as the difference between the yield on a nominal 5-year U.S. Treasury note and a 5-year Treasury Inflation-Protected Security (TIPS), reflects the market’s forecast for average annual inflation over the next five years.

What’s especially concerning is the spike since late January, reflecting the market’s anticipation of the inflationary impact of the upcoming tariffs.

Another key indicator I closely monitor is theProShares Inflation Expectations ETF (NYSE:RINF). As shown, it has surged over the past four trading sessions, building on its steady rise since August.

The persistent and rising inflation, coupled with a likely impending recession is setting the stage for “ stagflation ”—a condition marked by high inflation, stagnant economic growth, and elevated unemployment.

The U.S., UK, and other countries experienced stagflation in the 1970s, driven by rapid money supply expansion and energy crises.

If stagflation returns—which seems increasingly likely—the Federal Reserve will find itself in a difficult predicament, as its ability to implement monetary stimulus will be constrained by persistently high inflation.

The current inflationary pressures stem largely from the trillions of dollars injected into the economy through COVID stimulus programs, making inflation particularly stubborn. In the end, the Fed will likely prioritize economic support over inflation control, leading to high rates of inflation reminiscent of the 1970s.

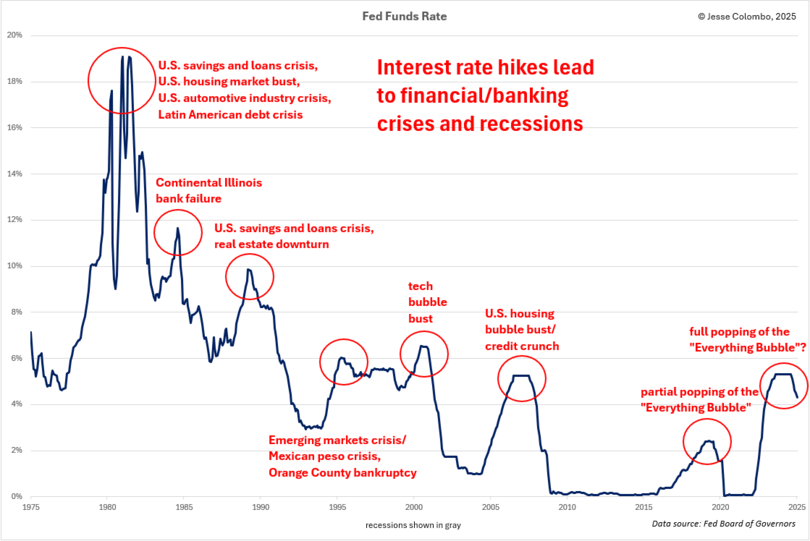

Recessions almost always follow rate hike cycles, and the latest cycle has been the most aggressive since the early 1980s. In just a year and a half, the Federal Reserve raised the fed funds rate from near zero to 5.33%, surpassing even the mid-2000s rate hikes that contributed to the housing bubble collapse and the Great Recession.

While many economists and investors remain optimistic about a soft landing, history suggests that such outcomes are rare—especially after a tightening cycle of this magnitude.

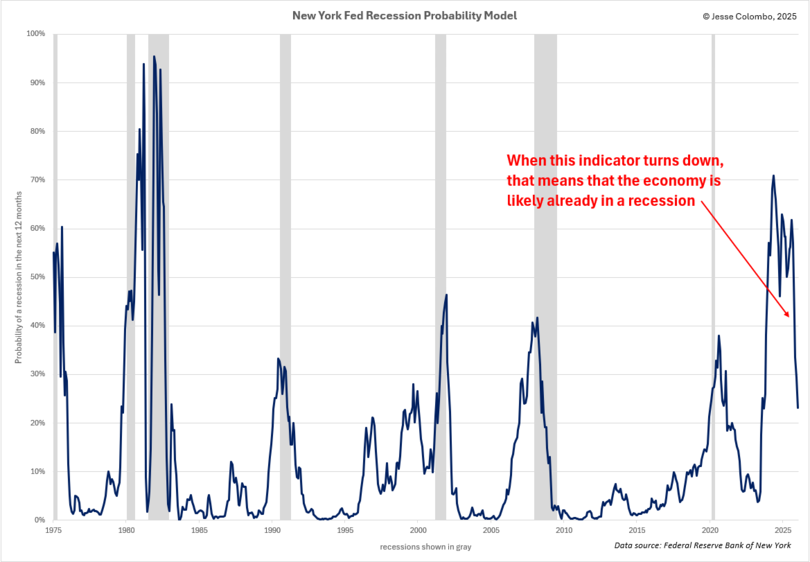

Several recession indicators are flashing warning signs, and one of the most reliable is the New York Fed Recession Probability Model, which assesses the likelihood of a recession within the next 12 months.

Historically, as this indicator rises, so does the probability of an economic downturn. However, once it begins to decline, it often signals that a recession has already begun.

Over the past year, this model has started to trend downward, indicating that the U.S. economy may already be in a recession or on the verge of entering one.

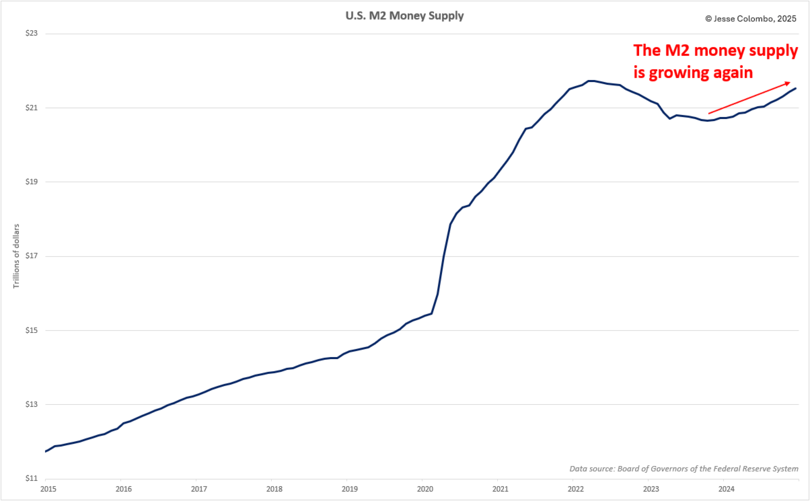

Further reinforcing the stagflationary outlook is the resurgence of U.S. M2 money supply growth over the past year, following a rare period of decline from early 2022 to late 2023.

Since money supply expansion is the root cause of inflation, this renewed growth helps explain why inflation has remained persistently high and why gold and silver have surged over the past year.

As Nobel Prize-winning economist Milton Friedman famously stated, “Inflation is everywhere and always a monetary phenomenon.”

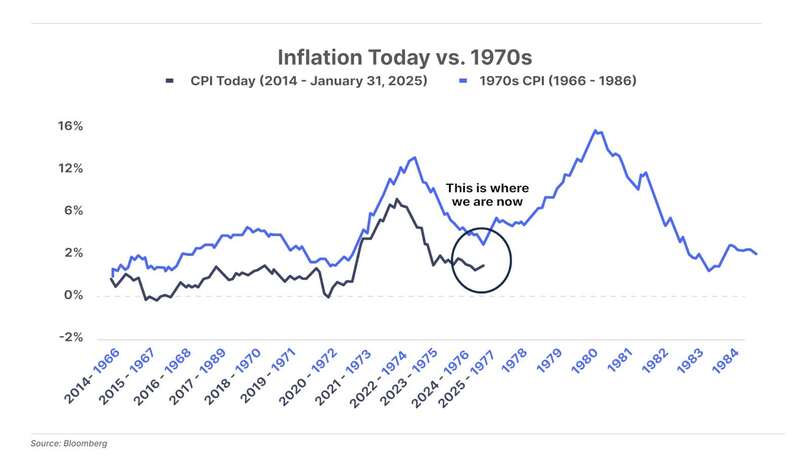

What’s especially concerning is how closely today’s inflation trajectory mirrors that of the 1970s—a parallel highlighted by financial publisher and author Porter Stansberry, who shared this chart on X this morning:

While a stagflationary scenario would be highly detrimental to the overall U.S. economy, precious metals and mining stocks would benefit significantly—much like in the 1970s when gold emerged as one of the top-performing assets, vastly outperforming equities and bonds.

While gold was the stronger performer in the mid-1970s, silver ultimately stole the show as the precious metals bull market matured in the late 1970s.

A similar pattern appears to be unfolding today, with gold currently outpacing silver. However, as this bull market gains momentum, silver is likely to take the lead once again.

While President Trump and the Department of Government Efficiency (DOGE), led by Elon Musk, have made commendable progress in reducing government spending—cutting approximately $88 billion so far—that amount is merely a drop in the bucket compared to the nation’s $36.5 trillion debt and the record $840 billion budget deficit logged over the past four months alone.

Moreover, deeper spending cuts are likely to trigger more layoffs and a broader economic slowdown, given the economy’s heavy dependence on government expenditures.

Ironically, while DOGE’s efforts are fiscally responsible, they may inadvertently hasten a recession that was already in the works long before President Trump took office. Additionally, because President Trump is not addressing the root cause of inflation—the absence of sound money —the problem will not be resolved.

As a result, stagflation remains the most probable outcome, creating a highly bullish environment for gold, silver, and mining stocks.

Originally Published on TheBubbleBubble.

Republished on Money Metals.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

The Growing Risk of Stagflation Bodes Well for Gold and Silver

Published 02/13/2025, 11:37 AM

The Growing Risk of Stagflation Bodes Well for Gold and Silver

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.