- S&P 500 plunges below 4,000, Nasdaq crashes 4%, but futures turn positive today

- Dollar edges down as yields cool off slightly ahead of Fed speakers, US CPI

- Oil remains under pressure as EU waters downs Russian oil embargo

Stock market rout deepens

Equity markets have steadied on Tuesday as investors licked their wounds following the heavy losses at the start of the week that extended the post-Fed meeting selloff. Growth and mega-cap tech stocks led the carnage on Wall Street on Monday, pulling the S&P 500 (-3.2%) below the 4,000 level for the first time since April 2021. The tech-heavy Nasdaq Composite (-4.3%) slid even more, while the Dow Jones (-2.0%) fared slightly better.

Fears about a slowdown in growth are intensifying as central banks around the world step up their fight to tackle soaring inflation. The global growth outlook has turned even gloomier after China imposed tough lockdown restrictions in Shanghai and Beijing, with authorities doubling down on their zero-Covid strategy in recent days.

Nevertheless, the calmer mood helped Chinese stocks to notch up gains of about 1% and European markets opened in positive territory, while US futures were also higher.

Fed speakers on watchlist ahead of US CPI

Atlanta Fed President Raphael Bostic yesterday reinforced expectations that the Fed will likely hike rates by another 50 basis points in at least the next two meetings. But he only assigned a “low probability” to the idea that policymakers might opt for a more aggressive 75-bps hike, providing some relief to jittery markets.

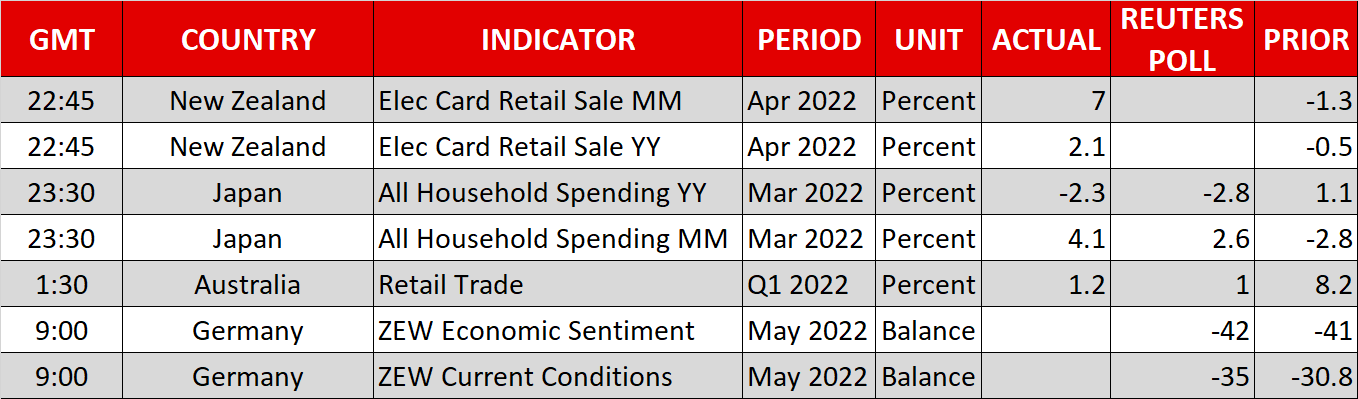

More Fed officials will be on the roster today, including Governor Waller and the Cleveland Fed’s Mester. However, this week’s main focal point is the April CPI report coming up on Wednesday as the forecasts suggest inflation may be peaking in America.

A softer-than-expected CPI print could put the wind back in Wall Street’s sails, especially if it sparks a further retreat in Treasury yields. The 10-year yield reversed sharply lower yesterday, pulling back from a 3½-year high of 3.2% to around 3%.

Dollar off highs, pound crawls higher despite ongoing woes

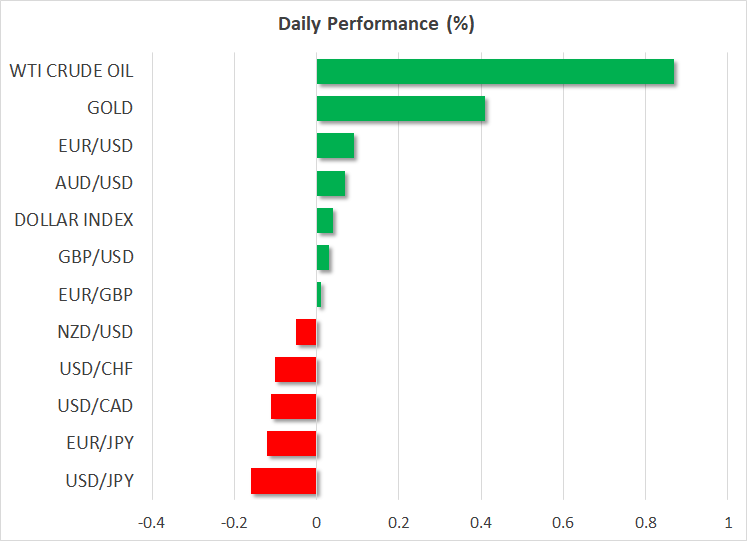

Lower yields as well as the somewhat more positive market tone appear to be weighing slightly on the US dollar on Tuesday. The dollar index has stepped back from yesterday’s 20-year high of 104.19, though only marginally. Still, beaten-down currencies like the pound managed to regain some footing today.

Sterling has slumped over the past month, hitting a near two-year low of $1.2258 on Monday. Aside from the Bank of England’s pessimistic forecasts for the UK economy at last week’s meeting, Brexit tensions have resurfaced, raising fears of a fresh standoff between London and Brussels. UK Foreign Secretary Liz Truss is reportedly readying plans to ditch parts of the Northern Ireland protocol following months of talks with the EU that have led to no progress.

The euro was flat around $1.0560, and the commodity-linked currencies also steadied after recovering from their early session dips.

Oil rebounds but downside risks persist

Higher commodity prices are likely aiding the aussie, kiwi and loonie. Oil prices erased earlier losses, with WTI and Brent futures turning modestly positive at the start of European trading. However, concerns about demand continue to be a drag in the short term as the lockdowns in China could last a few more weeks, while the recent boost from the EU’s move to ban Russian oil imports is also waning.

The European Commission is struggling to get the backing it needs from all member states for its proposed sanctions on Russian oil and is having to make concessions, one of which is to allow EU tankers to continue to transport Russian crude, meaning there will be less disruption to supply to non-EU destinations.