- Escalating conflict in Ukraine ravages risk assets as stocks sink, Russian rouble tumbles

- Oil and metal prices soar on supply fears but gold stumbles

- FX markets relatively steady as Fed policy uncertainty holds dollar in tight range

Equities tank as Russia, Ukraine on the brink of war

Global stock markets sank deep into the red on Tuesday, extending Monday’s losses, with US equities likely joining the selloff today when Wall Street traders return from a long holiday weekend. US, UK and European leaders are set to announce fresh sanctions on Russia after Moscow said it will recognize the independence of the two breakaway regions of Donetsk and Luhansk in eastern Ukraine.

But the escalation didn’t stop there as President Putin swiftly followed the decision by ordering Russian troops to enter the separatist regions for ‘peacekeeping’. While hopes for a diplomatic solution have not been completely dashed, it’s difficult to see how Russia could step back from the brink of war with Ukraine following the developments of the last 24 hours.

The big question now is whether Moscow will simply settle on tightening its grip on eastern Ukraine or if this was just phase one of a full-scale invasion.

Russian equities lead selloff

The intensifying crisis has sent Russian stocks spinning lower, with the country’s main indices plummeting more than 10% yesterday and trading down by more than 5% on Tuesday. The Russian rouble has also gone into freefall, plunging to a near 16-month low of 80.93 to the dollar.

In the rest of Europe, the major indices opened more than 2% lower but then started to pare some of their losses by mid-morning, signalling a slight easing of the panic.

Stocks in Asia fell across the board too, with worries about a new wave of regulatory crackdown by Chinese authorities on the tech sector additionally weighing on Hong Kong’s Hang Seng index.

US stock futures were pointing to a third straight session of losses for Wall Street’s leading indices, with Nasdaq futures down the most (-1.7%).

Oil targets $100 a barrel, gold unable to overcome $1,900 resistance

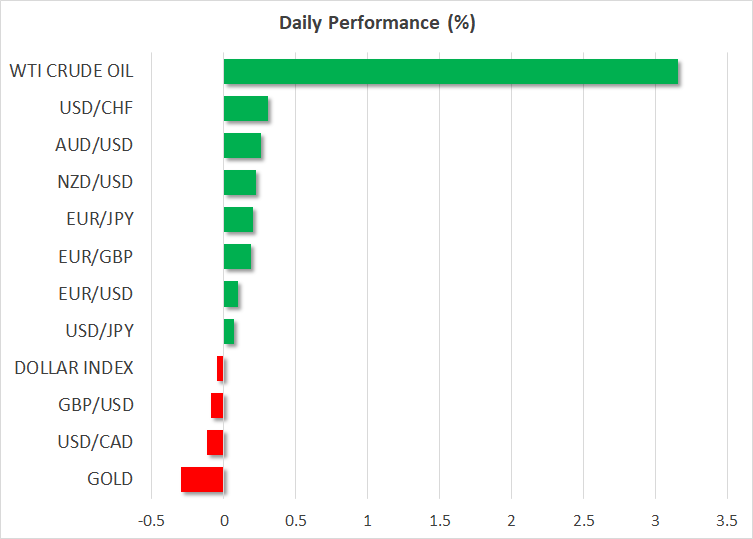

Energy was the only stock market sector in the green on Tuesday, which unsurprisingly, came on the back of the surge in oil prices. Fears that a full-scale military conflict could disrupt oil and gas exports from Russia are driving the rally in energy prices.

Brent crude futures are on the verge of hitting the $100 per barrel mark, while WTI futures have surpassed $95 a barrel.

But it wasn’t just energy commodities being boosted from the heightened geopolitical tensions as some metal prices like aluminium and nickel also climbed strongly on concerns about Russian supply.

Gold, however, was struggling to make a clear break above $1,900, pulling back after brushing a nine-month peak of $1,913.89.

US Treasury yields are bouncing back from overnight lows, so that could be weighing on the precious metal. But traders might also be waiting to see how tough Western sanctions against Russia will be before pushing higher.

Commodity dollars edge up as US dollar flatlines

The gains in commodities markets bolstered the commodity-linked Australian, Canadian and New Zealand dollars. The aussie was headed for a second day of gains, though the loonie’s boost from the oil rally was very meagre.

The kiwi, meanwhile, was eyeing yesterday’s one-month high of $0.6733 ahead of the RBNZ’s policy decision early on Wednesday.

All three were also up against the Japanese yen, as the safe haven currency retreated from earlier session highs as the tense mood abated somewhat over the course of the day.

The US dollar, however, was mostly flat as the euro and pound also mostly kept within their recent ranges.

The crisis in Ukraine has sparked a scaling back of some of the more aggressive Fed rate hike bets by market participants, undermining the greenback. Senior Fed officials have also cast doubt on the possibility of a double rate hike in March, though Fed Governor Michelle Bowman yesterday hinted that 50 basis points was not off the table.

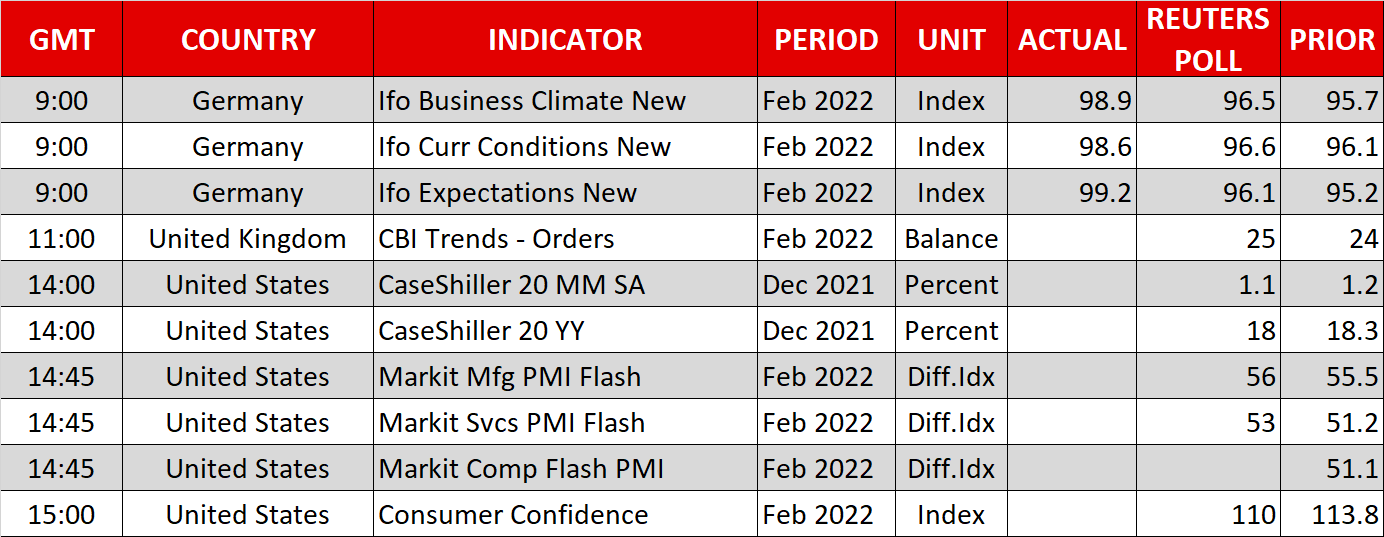

Atlanta Fed President Raphael Bostic will be the next to give his views when he speaks later today, while the latest consumer confidence index and the flash Markit PMIs for February out of the US will also be watched.