The Federal Reserve's recent decision to slash interest rates by an unexpected 0.5% has sent shockwaves through global financial markets. This bold move, larger than the modest cuts many analysts anticipated, has heightened volatility across stocks, currencies, and commodities. Initial reactions saw a sharp uptick in stock prices, followed by an equally swift decline, reflecting investor uncertainty about the economic outlook. Such a significant rate cut raises critical questions about the catalysts behind the decision, its historical parallels, and its potential impact on currency pairs, gold, and stock indices. This article delves into the causes of the Fed's substantial rate reduction, compares it to previous monetary actions, explores future policy directions, and analyzes the repercussions on key financial markets.

Breakdown of the 0.5% rate cut

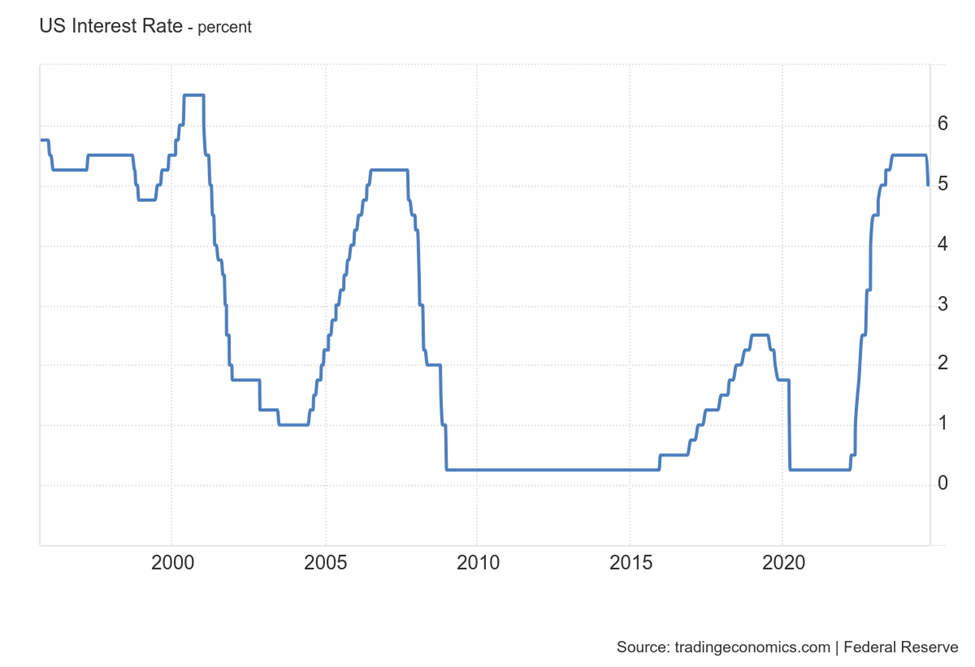

On September 18, 2024, the Federal Reserve took a bold step by cutting interest rates by 0.5%, a decision that surprised markets and analysts alike. This move lowered the federal funds rate from 5.25% – 5.50% to 4.75% – 5.00%, marking the most significant reduction in over four years and setting a new course for US monetary policy after a year of holding rates steady. The Fed cited growing concerns over slower economic growth, inflationary pressures nearing control, and slight labor market softening as the key reasons behind this aggressive action.

Catalysts behind the cut

The backdrop to this rate cut includes both domestic and global factors. US economic growth has been gradually weakening, with real GDP growth projections lowered to 2.7% for the year, up from the earlier estimate of 2.4%. Additionally, despite inflation trending toward the Fed's 2% target, the core inflation rate remains elevated, with the Fed revising its projection for 2024 to 3.4%, compared to 3.6% in June. Labor market conditions are also shifting, with unemployment expected to increase to 4.1% in 2024, slightly above the previous projections of 4.0%.

Globally, factors such as ongoing trade tensions with China, reduced European demand, and persistent supply chain disruptions have added further pressure on the US economy. Domestically, the housing market remains strained, with home affordability challenges due to high prices. While mortgage rates are expected to decline following the rate cut, affordability remains a concern.

Immediate market reactions

The market’s response was volatile and mixed. Initially, US stocks surged, with indices like the S&P 500 and NASDAQ hitting all-time highs as investors anticipated cheaper borrowing costs and potential support for corporate profits. However, the rally was short-lived, as fears of deeper economic problems, particularly the potential for an economic slowdown, quickly surfaced. By the end of the day, significant indices had declined, reflecting the uncertainty surrounding the broader economic outlook.

In bond markets, yields on US Treasuries fell sharply as investors sought the safety of government debt. The yield on the 10-year Treasury, for example, dropped to 4.1%. The US dollar also weakened against major currencies, including the euro and the yen, as lower interest rates made dollar-denominated assets less attractive to foreign investors. This decline in the dollar has broad implications for global trade, potentially making US exports more competitive but raising the cost of imports.

The Federal Reserve's decision to cut interest rates by 0.5% in September 2024 echoes significant monetary policy actions from the past, notably those in 2001 and 2007. By examining these historical instances, we can glean insights into potential outcomes and market reactions associated with such aggressive rate reductions.

Echoes from the past

2001 rate cut

In response to the bursting of the dot-com bubble and the ensuing economic slowdown, the Federal Reserve embarked on a rate-cutting cycle starting in January 2001. The Fed reduced the federal funds rate from 6.5% to 1.75% by the end of the year, totaling a 4.75% decrease. This aggressive stance aimed to stimulate investment and consumer spending amidst declining corporate profits and rising unemployment, which peaked at 5.8% by the end of 2001.

Despite these efforts, the S&P 500 experienced a downturn, declining approximately 10% in the three months following the initial rate cut. The aggressive cuts were unable to fully counteract the negative sentiment caused by the tech sector collapse, leading to prolonged market stagnation and contributing to the early 2000s recession.

2007 rate cut

Facing the emerging subprime mortgage crisis, the Fed initiated a rate-cutting cycle in September 2007, reducing rates by 0.5% from 5.25% to 4.75%. Over the next year, the Fed continued to lower rates, culminating in a near-zero rate environment by the end of 2008.

Market Impact: While the initial rate cuts provided temporary relief, the depth of the financial crisis that unfolded in 2008 overwhelmed these measures. The S&P 500 plummeted by 57% from its peak in October 2007 to its trough in March 2009.

Comparative analysis with 2024

Unlike the pre-recession periods of 2001 and 2007, the US economy 2024 is not formally in a recession. As of September 2024, GDP growth stands at 2.7%, unemployment is slightly elevated at 4.1%, and inflation has been brought closer to the Fed's target, with core inflation projected at 3.4%.

These indicators suggest a more nuanced economic environment than the clear downturns preceding the 2001 and 2007 rate cuts.

Post-2008 regulatory reforms have fortified the banking sector, reducing systemic risks. Banks now maintain higher capital reserves, and stress-testing procedures are more rigorous, potentially mitigating the fallout from aggressive rate cuts.

The Fed possesses a broader arsenal of monetary policy tools, including quantitative easing and forward guidance, which were less developed during the previous rate-cut cycles. These tools can provide more targeted support to specific sectors without broadly impacting the entire economy.

The 2024 rate cut occurs in a highly interconnected global economy, where coordinated policy responses from other major central banks can influence outcomes. In 2001 and 2007, global policy coordination was less robust, exacerbating economic downturns.

If the Fed can leverage its enhanced policy toolkit and the economy remains resilient, the 2024 rate cut may avoid the severe market downturns seen in 2001 and 2007. However, persistent global economic uncertainties, such as trade tensions and geopolitical risks, could still pose significant challenges.

Will the Fed continue to cut rates?

The Fed's rate cut marks the beginning of a long easing cycle. As inflation has slowed to 2.9%, the Fed's focus has shifted from fighting inflation to addressing slowing economic growth and softening the labor market. The big question remains: will the Fed continue to cut rates, and if so, how aggressively?

Several key factors will drive the Fed’s decisions in the coming months:

● Inflation: With inflation nearing the Fed’s 2% target, the immediate pressure to continue rate hikes has eased. However, core inflation, which excludes volatile energy and food prices, still remains slightly higher at 2.7%. Continued moderation in inflation could give the Fed room to lower rates further, particularly if other economic indicators weaken.

● Labor Market: The unemployment rate has risen to 4.2%, up from 3.6% earlier in 2023, as job openings have declined and wage growth has slowed. If the labor market continues to soften, the Fed may feel compelled to cut rates further to stimulate employment. The rate is expected to rise to 4.5% by the end of 2025.

● Global economic slowdown: Weaker growth in major economies like China and Europe, combined with persistent geopolitical tensions, is also exerting pressure on the US economy. Despite China's extreme stimulus measures, European industry continues to shrink, with average unemployment rates rising, especially in Germany. If global demand shrinks, the Fed may need to cut rates to support domestic growth.

The Fed’s “dot plot” projections from the September meeting indicate that more rate cuts are likely before the end of 2024. The current projection points to an additional 50 basis points of cuts, which would bring the federal funds rate down to a range of **4.25% – 4.5%**. This aligns with market expectations, as investors are already pricing in at least two more rate cuts before the year ends.

However, a sudden resurgence of inflation, particularly driven by supply chain issues or rising energy costs, could force the Fed to reconsider its easing strategy, potentially leading to rate hikes in 2025.

Given the current parameters and dynamics, the Federal Reserve will gradually reduce interest rates, reaching the 3.00% range by the end of 2025. The forecast assumes that rate cuts will begin in 2024 to address slowing economic growth, help balance the US economy, curb inflation, and support the labor market.

Market ripples: DXY, gold, and S&P 500

The sharp rate cut has raised a lot of questions and concerns among market participants, as many banks and experts expected only a 0.25% reduction. This significant monetary policy shift has prompted a reevaluation of asset valuations across currencies, commodities, and equities.

US Dollar

Following the rate cut, the US dollar is under increased pressure and is expected to weaken further. Goldman Sachs forecasts a 3-5% decline in the US Dollar Index (DXY) over the next few months. This expected decline is largely due to the narrowing yield differential between the United States and other major economies.

Historically, rate cuts have almost always led to a weaker dollar, and a similar trend is expected this time, especially given the possibility of one or even two more rate cuts on the horizon.

Gold

Gold rose significantly after the US Federal Reserve rate cut, rising to an unprecedented $2,627 per ounce. Goldman Sachs forecasts that gold prices will average around $2,800 by the fourth quarter of 2024 and could reach $3,000 by mid-2025. This optimistic outlook is further supported by escalating geopolitical tensions, with several global conflicts intensifying. However, some banks and experts expect an even more significant rise by the end of 2024. UBS predicts that gold could hit $3,000 an ounce by early 2025, especially if the Federal Reserve continues its aggressive rate-cutting cycle. For example, FBS experts point out that increased central bank purchases and a global shift away from the US dollar are the main factors supporting this upward trajectory. In addition, gold's traditional role as an inflation hedge is being reinforced by ongoing economic uncertainty. Industrial demand further supports gold prices, especially in the electronics and artificial intelligence sectors.

In the Weekly timeframe, XAUUSD is approaching the 261.8 Fibonacci level, indicating a long-term bullish trend. Given the extremely bullish market sentiment, we can expect a rise, although a correction may occur before that.

● If Gold overcomes the resistance at 2800, it will rise to 3000 and then to 3270;

● A rebound from the resistance will drop XAUUSD first to the support area of 2400, and then the price will go up;

S&P 500

The immediate reaction to the US Federal Reserve's rate cut was optimistic: major US stock indices, such as the S&P 500, rose markedly. However, long-term forecasts suggest a more subdued outlook. JP Morgan expects that the S&P 500 could rise by 6.6% over the next 12 months, slightly below the historical average. Lower borrowing costs are expected to partially offset the benefits of slower economic growth.

Sectors that could benefit most from the loose monetary policy include technology and consumer staples, which have historically thrived in a low-interest-rate environment. Technology stocks, especially those involved in artificial intelligence and semiconductor manufacturing, have risen significantly as cheaper financing encourages expansion and innovation. In contrast, cyclical sectors such as industrial and financial companies could face headwinds if economic growth remains weak.

In the Daily timeframe, the US500, in a long-term bullish trend, made an all-time high again at the 161.8 Fibonacci level. Based on the current dynamics, we can expect a minor correction before a prolonged rise.

● If the bulls push the price above the 5700 resistance, the target will be 7000, corresponding to 261.8 Fibonacci;

● A rebound from the resistance will drop the US500 to the trend line, after which further upside growth can be expected;

Conclusion

The Federal Reserve's official rate cut has begun, signaling the potential for further reductions ahead. The decline in the US dollar favored currencies such as the euro and the yen, while gold prices soared to record highs amid lower opportunity costs and inflation concerns. US stock indexes have shown initial volatility, and further performance depends on the Fed's ability to balance rate cuts and economic growth. As the market adjusts to the new monetary policy environment, traders and investors have a unique opportunity to assess risks and make informed trades, given that a clear trajectory has already been established.