Second quarter earnings season is almost over for the Medical sector with 94.5% of companies belonging to this segment having reported results. A look at the scorecard for Q2 shows that the Medical sector recorded earnings growth of 6.7% on revenue growth of 4.3%. While the earnings beat ratio was 82.7%, the revenue beat ratio was 67.3%. Biotech stocks, in particular, did pretty well this quarter with quite a few companies raising their guidance for the year. Pharmaceutical companies also fared reasonably well. Generic companies, on the other hand, had a tough quarter, and are facing a bleak outlook for the remainder of the year.

While several major biotech stocks did well in the second quarter, here is look at how two major names in this sector - Alexion Pharmaceuticals, Inc. (NASDAQ:ALXN) and Regeneron Pharmaceuticals, Inc. (NASDAQ:REGN) - fared in the second quarter and which one looks better-positioned for the second half of the year.

An In-Depth Look at 2Q17 Results: Both Regeneron and Alexion surpassed earnings as well as revenue expectations in the second quarter. Regeneron’s earnings results were driven by strong Eylea sales as well as a lower tax rate. Flagship drug, Eylea, continued to perform well though PCSK9 inhibitor, Praluent, continues to lag. The company is in discussions with payers with respect to improvement in utilization management criteria. Meanwhile, CVS announced that it would provide co-preferred access to Praluent through its CVS Caremark commercial formularies, which cover approximately 25 million lives (Also read: Regeneron Beats on Q2 Earnings & Sales, Raises View). Focus was also on new product launches – Dupixent (eczema) and Kevzara (rheumatoid arthritis).

Alexion’s results were driven by the performance of flagship drug, Soliris, and continued momentum of Strensiq. The company, however, noted that revenues benefited by $35 million reflecting the favorable timing of orders (Also read: Alexion Tops Q2 Earnings & Revenues, Ups 2017 View).

2017 Outlook: Regeneron raised its U.S. sales growth outlook for Eylea to approximately 10% (old guidance: single digit percentage). The company also lowered its expected tax rate for the year.

Alexion also raised its outlook for the year. The company expects earnings of $5.40 - $5.55 per share on revenues of $3,450 - $3,525 million (old guidance: $5.10 - $5.30 per share on revenues of $3,400 - $3,500 million).

Pipeline Catalysts: For any pharmaceutical or biotech company, the pipeline is of utmost importance and plays an important role in investment decisions. So, it always makes sense to take a look at a company’s pipeline and upcoming catalysts.

Regeneron, which has 17 candidates in its pipeline, has an eventful second half of the year coming up with key mid-to-late stage pipeline catalysts lined up. Top-line phase III data on Dupixent for asthma are due later this quarter – positive data would allow the company to go ahead with a U.S. filing in the fourth quarter. Dupixent should also gain EU approval for the eczema indication in the third quarter. Regeneron is evaluating Dupixent in the pediatric atopic dermatitis setting with a phase III study in children 12 to 17 years of age currently enrolling while two additional studies in younger atopic dermatitis patients (the first in children between the ages of 6 and 11, and the second in children between the ages of six months and five years) expected to commence in the second half of the year.

Another important data readout scheduled for the second half of the year is on the company’s PD-1 antibody REGN2810, for cutaneous squamous cell carcinoma (CSCC), the second most common skin cancer after basal cell carcinoma and the second deadliest skin cancer after melanoma. Positive data would allow the company to file for FDA approval in the first quarter of 2018. REGB2810 is being evaluated for additional indications as well.

Meanwhile, Eylea is being evaluated in combination with nesvacumab. Top-line data from two phase II studies - one in wet age-related macular degeneration and another in diabetic macular edema – are expected in the fourth quarter of the year.

Regeneron also expects to report top-line data in the second half of the year from a late-stage program on REGN2222, which is being evaluated for prophylaxis of respiratory syncytial virus.

Meanwhile, Alexion is redefining its R&D strategy with a focus on its key expertise areas. The company will continue to grow its rare diseases business which includes growing Soliris, Strensiq and Kanuma. To increase productivity, Alexion will focus its internal research efforts on its complement expertise and its development efforts on its core therapeutic areas of hematology, nephrology, neurology and metabolic disorders. The company has also decided to de-prioritize certain pipeline candidates and is discontinuing its preclinical programs with mRNA therapies as well as other preclinical programs that do not fall within the complement franchise.

Alexion has a key regulatory event coming up with the FDA expected to give a decision by Oct 23 regarding the label expansion of Soliris for refractory generalized myasthenia gravis (gMG). A decision in the EU should also come out in the third quarter. Moreover, enrolment for a phase III study on Soliris for relapsing neuromyelitis optica spectrum disorder (NMOSD) is expected to finish this year.

Estimate Revisions: Both companies have been witnessing upward revisions in earnings estimates for 2017. While Regeneron has seen the Zacks Consensus Estimate for current-year earnings being revised 31.3% upward over the last 30 days, Alexion has seen the Zacks Consensus Estimate for current-year earnings being revised 4.8% upward during this period.

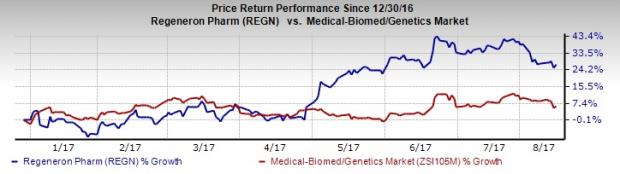

Price and Valuation Perspective: A look at Regeneron’s year-to-date (YTD) price performance shows that its shares have gained 27.1% year to date, significantly outperforming the industry’s 6.2% rally.

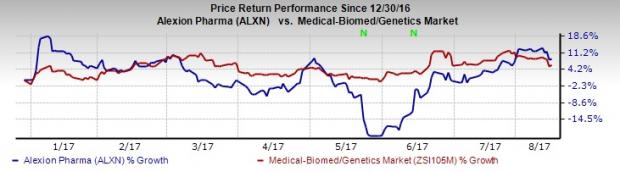

Alexion has also performed better than the industry with shares gaining 8.7 % YTD.

Going by the current price-to-earnings multiple, which is often used to value profitable biotech stocks, Regeneron is trading at a P/E multiple of 41.4, well above the S&P 500 P/E multiple of 17.8. Alexion looks slightly cheaper given its P/E multiple of 25.7.

Bottom Line

At present, Regeneron looks like the better pick to us. Eylea continues to show strength and we are encouraged by the company’s progress with its pipeline. Regeneron has a deep and promising pipeline and has some important pipeline events this year which could act as positive catalysts.

As far as Alexion is concerned, we are impressed by the new management’s efforts to turn things around. Alexion had a rough 2016 with the company facing several challenges including a probe into improper sales practices, the departure of key executives and pipeline setbacks. We are encouraged by the company’s decision to re-prioritize its efforts toward core areas. However, it could take a while before things fall into place. Soliris sales are expected to be lower in the second half of the year taking into account the favorable order timing in Q2 as well as the accelerating impact of the ALXN1210 studies.

Regeneron and Alexion are both Zacks Rank #1 (Strong Buy) stocks. You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Trades Could Profit "Big-League" from Trump Policies

If the stocks above spark your interest, wait until you look into companies primed to make substantial gains from Washington's changing course.

Today Zacks reveals 5 tickers that could benefit from new trends like streamlined drug approvals, tariffs, lower taxes, higher interest rates, and spending surges in defense and infrastructure. See these buy recommendations now >>

Alexion Pharmaceuticals, Inc. (ALXN): Free Stock Analysis Report

Regeneron Pharmaceuticals, Inc. (REGN): Free Stock Analysis Report

Original post

Zacks Investment Research