When the market drops sharply, as it did last week, investors get the chance to buy great companies at a discount. This company has an unprecedented history of growth and profitability, along with a well-deserved reputation as one of the most advanced and innovative companies in the world. Alphabet (NASDAQ:GOOGL: $1,070/share) is this week’s Long Idea.

GOOGL Stands Alone

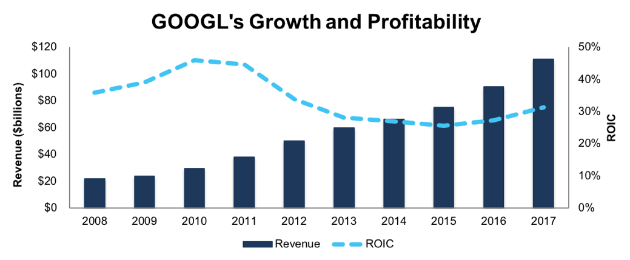

We’ve written before that the distinctions between growth and value investment styles are irrelevant. The best investments offer both growth – in the form of steadily increasing revenue –and value – in the form of a high return on invested capital (ROIC). No company combines these two factors better than GOOGL, as shown in Figure 1.

Figure 1: GOOGL’s Revenue and ROIC since 2008

Sources: New Constructs, LLC and company filings

Those numbers are simply incredible when you consider GOOGL has never earned an ROIC below 25% (the median S&P 500 stock earns an ROIC of 8%). The last time the firm grew revenue by less than 10% annually was in the depths of a recession in 2009.

Only two other S&P 500 companies can match GOOGL’s record of 25% or higher ROIC and double-digit revenue growth for each of the past five years. These two companies, Align Technology Inc (NASDAQ:ALGN) and Regeneron Pharmaceuticals Inc (NASDAQ:REGN), both face looming patent cliffs. When it comes to sustainable growth and profitability, GOOGL has no equal.

GOOGL Has Little Competition In its Core Markets

In its core businesses, GOOGL has a market share that few other companies can match. In search, Google controls ~75% of the market. In video, YouTube has a nearly 80% market share.

GOOGL’s dominance compares favorably to the other highly touted FANG stocks. Facebook (NASDAQ:FB) has an estimated 42% market share in social media. Amazon (NASDAQ:AMZN) controls 44% of the e-commerce market. Netflix (NASDAQ:NFLX) has a comparable 75% share of streaming households, but many consumers use Netflix along with competitors such as Prime Video, HBO Go, or Hulu. By comparison, few people are toggling back and forth between Google and Bing.

Google’s dominance is also self-reinforcing. Because it has the most users, websites have to optimize for its platform, which in turn makes its search results more useful than competitors’. In addition, the larger volume of searches gives Google more data it can use to further refine its algorithm.

At this point, Google is fundamentally ingrained in the process of using the internet. As long as internet usage continues to grow at a rapid pace, which it should for the foreseeable future, GOOGL’s profits will grow with it.

Continually Investing in the Future

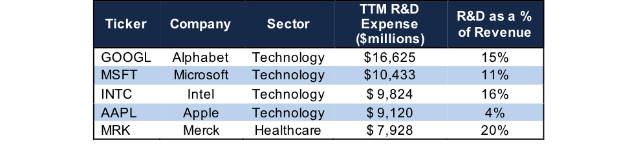

GOOGL’s profitability is all the more remarkable when one considers how much money the company spends on projects that may not earn profits for years to come. As shown in Figure 2, GOOGL spends more on research and development than other American company.

Figure 2: GOOGL’s R&D Spending Dwarfs the Competition

Sources: New Constructs, LLC and company filings

The difference in R&D spending between GOOGL and Microsoft (NASDAQ:MSFT) in second is larger than the difference between MSFT and IBM (NYSE:IBM), the company with the 13th largest R&D budget. No company is devoting more resources to innovation and future technologies than GOOGL.

Readers may notice one glaring omission from Figure 2. Amazon does not report its R&D spending and instead bundles it into a line item called “Technology and Content.” AMZN spent $22.6 billion on technology and content last year, but we know that about $4.5 billion of that went to the content budget, and AWS-related costs also make up a substantial portion. It’s hard to know just how much AMZN spends on R&D, but it’s clearly less than GOOGL.

All that R&D spending has GOOGL positioned to control key industries in the future. We’re just finishing up a series on the growing importance of artificial intelligence, and GOOGL is one of the unquestioned leaders in the field of AI.

GOOGL’s AI research is already paying off in numerous ways beyond just improving the core search experience. The company is using its technology to help customers build and train their own machine learning systems, which adds more value to a rapidly growing cloud business. It will also start renting out its AI chips soon for another avenue of monetization.

Self-driving cars represent another promising technology, and the company’s Waymo division is acknowledged as a leader in the field. The commercial potential for advanced self-driving technology is enormous, as GOOGL could license its software to automakers or partner with ride-hailing companies to provide an autonomous transportation fleet. GOOGL could even use its technology the same way it does Android, as a way to control the user experience and expand its market share as cars become more interconnected.

Beyond these technologies, the umbrella structure of Alphabet allows the company’s subsidiaries to pursue many more speculative projects, such as research into extending the human lifespan, that could end up being enormously valuable if they can make real breakthroughs.

Essentially, GOOGL’s dominance in search and video gives it an abundant funding stream to pursue technological breakthroughs while still earning fantastic profits for investors.

Bear Case: Rising Traffic Acquisition Costs and Antitrust Suits

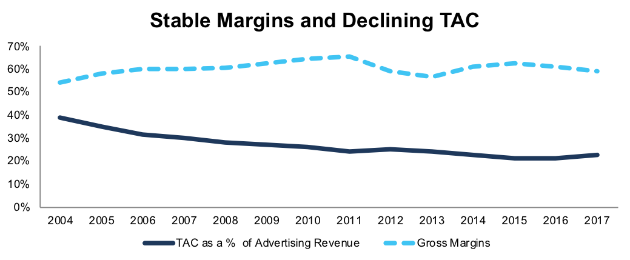

The market has two primary concerns when it comes to GOOGL. The first is the company’s rising traffic acquisition costs (TAC), which is the money it pays to third-parties to promote its search engine. Most notably, TAC paid to Apple (NASDAQ:AAPL) seems to be rising significantly as mobile searches take up a larger share of global search activity. As a result, the company’s gross margins have been in decline.

However, Figure 3 shows that the long-term trend for TAC and gross margins still looks strong. TAC as a percent of revenue has experienced a momentary spike in prior years and then continued its long-term downtrend. At the same time, gross margins have fluctuated, but stayed around 60%.

Figure 3: GOOGL’s Gross Margins and TAC as a % of Revenue Since 2004

Sources: New Constructs, LLC and company filings

Analysts believe the recent spike in TAC is attributable to a renegotiation of GOOGL’s deal with Apple, and CFO Ruth Porat says these costs should stabilize in the coming quarters.

Even if TAC continues to rise and gross margins fall, the company can offset this margin compression with revenue growth and increasing economies of scale. Since 2014, GOOGL’s SG&A as a percent of revenue has fallen from 21% to 18%. This trend should continue as the company continues to grow.

The longer-term threat to GOOGL comes in the form of antitrust pressures. The company was fined $2.7 billion by the EU last year for favoring some of its own shopping services over rivals. Investors and analysts worry that regulatory pressure could pose an existential threat to the company’s core search business.

While it seems plausible that GOOGL could face more fines in the future, it’s hard to imagine regulators posing such a big threat to the company. There’s just not the political pressure for regulators to crack down harshly on a free service that is widely admired by consumers. It seems much more likely that GOOGL will face occasional fines for specific actions than it will have its entire business model undermined.

Opportunity to Buy the Dip

After a 10% drop from its peak, GOOGL’s share price of $1,070 gives it a price to economic book value (PEBV) of 1.6, which implies that the company’s after-tax profit (NOPAT) will never grow more than 60% above its current level. By comparison, the Software and IT Services industry as a whole has a PEBV of 2.8. One would think a company with GOOGL’s track record would be valued at a premium to its peers, not a discount.

If GOOGL’s NOPAT margin expands to 23% (based on Cowen’s estimate of tax reform’s impact) and the company can grow after-tax profit by 14% compounded annually for the next decade, the stock is worth $1,520/share today, a 41% upside from the current price. Those expectations may seem high, but they pale in comparison to the company’s 20% compounded annual NOPAT growth rate over the past decade.

GOOGL is more expensive than the companies we usually recommend, which tend to have a PEBV of 1.2 or below. Still, as Warren Buffett once wrote, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” GOOGL is a wonderful company, and its current price is more than fair.

Tax Reform and Capital Return Provide a Catalyst

In addition to the lower tax rate mentioned above, the new tax law gives GOOGL the opportunity to repatriate some of its $100+ billion in excess cash at a lower 15.5% rate. The company already took a $10.2 billion “transitional tax” charge in 2017 to prepare for this repatriation.

Since the company’s R&D and investments are well-funded out of current cash flows, we suspect a large portion of the repatriated cash will go to capital return. The company recently announced an $8.6 billion (1% of market cap) stock buyback program, and it would not be surprising to see that number increase significantly in the near future.

Longer-term, the company’s steadily growing cash flow should serve to propel the stock higher.

Executive Compensation Should be More Transparent

GOOGL does not specify what metrics it uses to determine executive compensation, instead including a long list of metrics that can be used. The company notes that equity awards are granted on a biennial basis and vest quarterly over a four-year period.

We’re encouraged by the fact the list of possible metrics includes ROIC, but we’d like to see more transparency from GOOGL so that investors can better understand executive incentives. However, GOOGL’s current exec comp plan has not led to executives getting paid while destroying shareholder value. The company has generated positive economic earnings in every year since 1998, and has grown economic earnings from $3.1 billion in 2007 to $18.8 billion in 2017.

Insider Trading and Short Interest Trends

Insiders have acquired 235 thousand shares and sold 664 thousand shares over the past twelve months, for a net sale of 429 thousand shares. The total volume of insider trading represents less than 1% of shares outstanding. Minimal insider trading activity gives little insight to the stock.

There are currently 3.2 million shares sold short, which equates to 1% of shares outstanding and two days to cover. The market doesn’t seem to have much interest in betting against such a profitable and fast-growing company.

Auditable Impact of Footnotes & Forensic Accounting Adjustments

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Alphabet’s 2017 10-K:

Income Statement: we made $11.4 billion of adjustments, with a net effect of removing $11.4 billion in non-operating expense (10% of revenue). Our most significant adjustment was the $10.2 billion non-operating tax charge referenced above. You can see all the adjustments made to GOOGL’s income statement here.

Balance Sheet: we made $120 billion of adjustments to calculate invested capital with a net decrease of $94 billion. Excess cash accounted for the vast majority of these adjustments. You can see all the adjustments made to GOOGL’s balance sheet here.

Valuation: we made $117 billion of adjustments with a net effect of increasing shareholder value by $95 billion. The largest adjustment to shareholder value, despite the excess cash noted above, was $10.9 billion in total debt. This debt adjustment represents 1% of GOOGL’s market cap.

Attractive Funds That Hold GOOGL

The following ETFs and mutual funds allocate significantly to GOOGL and earn our Attractive or Very Attractive rating:

- Fidelity Select Software & IT Svcs Port: 8.6% allocation and Attractive rating

- Lazard US Equity Concentrated Instl: 6.8% allocation and Attractive rating

- Nuveen Growth Fund (NSAGX): 6.7% allocation and Attractive rating

- Advisor’s Inner Circle Fund: FMC Select Fund (FMSLX): 6.6% allocation and Very Attractive rating

Disclosure: David Trainer, Sam McBride, and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.