- China ramps up economic stimulus, US confirms student loan relief

- Dollar retreats despite rising yields, commodity currencies recover

- Stocks edge higher too, but caution lingers ahead of Jackson Hole

China steps up

Global markets woke up in a sunny mood on Thursday, taking comfort from signs that China is stepping up its stimulus game. Beijing announced a new round of spending measures overnight, amounting to almost 1% of national output, which will be calibrated towards infrastructure spending to reinforce an economy that is losing power.

The Chinese economy is getting hit from all sides, with a property sector crisis that has started to snowball amid rising global interest rates, zero-covid strategies that have hamstrung growth by making shoppers wary of going out, and an unprecedented drought forcing factory closures. While this stimulus will help mitigate the damage, the sheer size of the measures so far is unlikely to be sufficient to stop the bleeding, especially in the enormous property market.

It wasn’t just China announcing new spending. The White House confirmed it will cancel up to $10,000 in federal student debt for low-earning Americans, easing the debt burden on millions of people and scoring some political points less than three months out from midterm elections. Debt forgiveness can help boost spending and counter growth worries, but it is ultimately inflationary.

Markets cheer

With the world’s two largest economies rolling out new spending, market participants got the green light to load up on riskier assets such as equities and commodity-linked currencies that are sensitive to global growth.

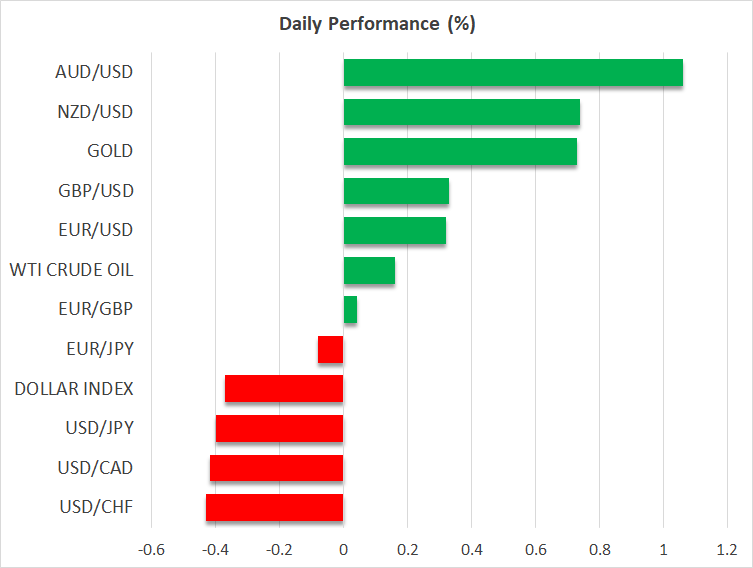

In the FX arena, the Australian and New Zealand dollars benefited the most. The entire business model of these economies relies on Chinese demand to absorb their commodity exports, so their currencies are widely viewed as liquid proxies for China plays. The Canadian dollar joined in the fun, even though Canada doesn’t export much directly to China.

In contrast, the dollar was lower across the board on Thursday as safe-haven demand dried up and capital flowed into riskier endeavors. Euro/dollar remained warped around parity, a region that is acting like a magnet for both buyers and sellers. Sterling continues to trade heavy, unable to capitalize much on the dollar’s pullback or the brighter mood in stock markets, underscoring its newfound preference to place more weight on negative rather than positive news.

Stocks spring higher

Stock markets were a sea of green in every region on Thursday, with Hong Kong’s Hang Seng index leading the charge higher. The major bourses in Europe were on track for a second day of gains, while futures tracking Wall Street pointed to a higher open of around 1%, despite a set of disappointing earnings from leading chip designer Nvidia (NASDAQ:NVDA).

Even though investors are still wary that the Fed might use the Jackson Hole symposium to put its foot down, especially with inflation expectations grinding higher, it seems that the promise of more fiscal juice was enough to eclipse those concerns for now.

Overall, the risk/reward profile for stocks doesn’t seem particularly attractive at this stage. Valuations are likely to compress again now that yields on government bonds have started to regain their former might, ‘real’ earnings growth for the S&P 500 is negative once adjusted for inflation, while demand from energy-squeezed Europe and property-troubled China could struggle.

As for today, the spotlight will fall on the minutes of the latest ECB meeting and the second reading of US GDP for Q2.