Despite the Nasdaq 100’s earlier single-day loss of -3% on 27 January inflicted by Chinese Artificial Intelligence (AI) start-up DeepSeek’s cutting-edge capabilities with lower operational costs, the price actions of Nasdaq 100 have remained resilient in the entire month of February.

It continued its upward climb but in a choppy fashion to recoup its January losses and printed a fresh all-time closing high of 22,176 on 19 February.

However, stagflation fears have resurfaced last week. Firstly, several US Federal Reserve officials as expressed in their respective discussions, noted in the latest FOMC minutes have flagged concerns of heightened inflationary pressures in the US if the White House follows through with its hawkish trade tariffs policy.

Secondly, the S&P Global flash US Services PMI data for February fell sharply unexpectedly to a contractionary level of 49.7 from 52.9 in the previous month, its first contraction in the services sector activity in the US over two years.

Given that the services sector contributes to almost three-quarters of US economic growth, the latest contractionary reading of the S&P Global flash US Services PMI, a leading economic growth indicator has triggered a “growth scare infused with sticky inflation” feedback loop into the US stock market that torpedoed all the four major US benchmark stock indices on last Friday. The Nasdaq 100 declined by almost 2%, its worst single-day decline in two months.

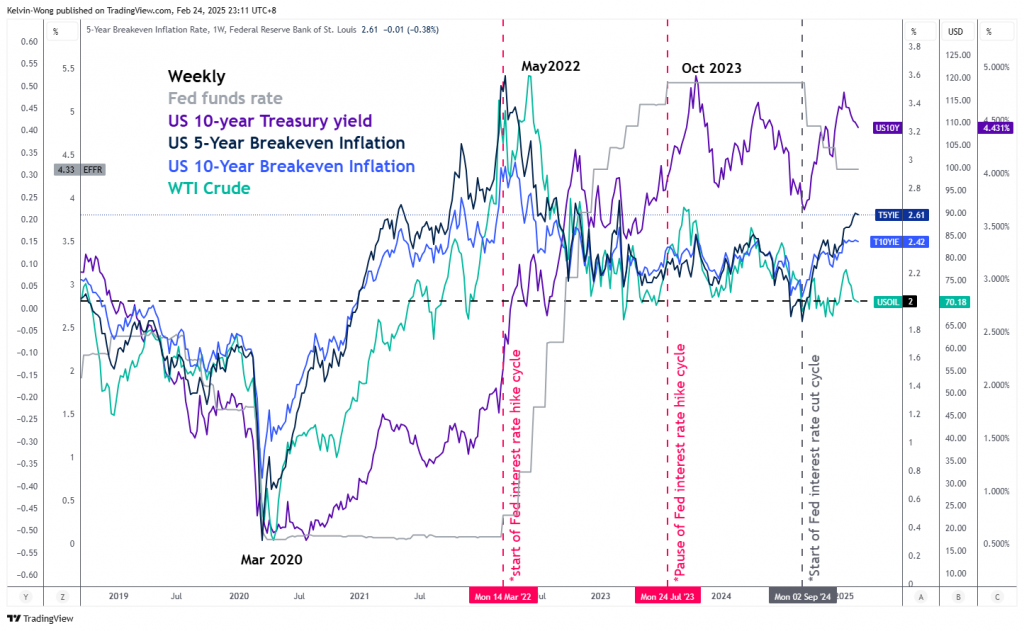

Inflationary expectations continued to divert further away from the Fed’s 2% target

Market-transacted inflationary expectations (breakeven inflation rates) in the US as inferred from the prices of Treasury Inflation-Protected Securities (TIPS) have surged significantly since December 2024.

The 5-year breakeven inflation rate has climbed to 2.61% as of last Friday, 21 February, its highest level in almost two years (see Fig 1).

Hence, the Fed is likely to adopt a less dovish monetary policy guidance in 2025 which may lead to a liquidity-tightening condition that is likely to be detrimental to US stock indices due to a higher cost of funding environment that can dampen earnings growth.

Bearish technical elements surfaced on the Nasdaq 100 ahead of Nvidia’s earnings results

US AI juggernaut Nvidia (NASDAQ:NVDA), also the second biggest market cap component stock in the Nasdaq 100 will report its fourth-quarter earnings results for calendar year 2024 on Wednesday, 26 February after the close of the US cash stock market session.

Interestingly, the trend condition and market breadth elements of the Nasdaq 100 are not so rosy at this juncture.

The daily MACD trend indicator flashed out an earlier bearish divergence on its histogram on 18 February coupled with a recent MACD signal line bearish crossover last Friday, 21 February. These observations suggest the bullish momentum of the medium-term uptrend phase of the Nasdaq 100 from the 5 August 2024 low may be exhausted, and a trend change towards a potential corrective decline sequence may be imminent.

In addition, the number of Nasdaq 100 component stocks that are making new 52-week highs (smoothed by a 5-day moving average) are lesser since 11 February while the Nasdaq 100 scaled to a fresh all-time closing high on 19 February which represents a weak market breadth condition at this juncture.

Watch the key 20,790 intermediate support on the Nasdaq 100 CFD Index (a proxy of Nasdaq 100 E-mini futures), and a daily close below it may trigger a multi-week corrective decline sequence to expose the medium-term supports of 19,840 and 18,310 (see Fig 2).

On the other hand, clearance above the 22,470/980 medium-term pivotal resistance zone invalidates the bearish scenario for the continuation of its impulsive upmove sequence for the next medium-term resistance zone to come in at 23,980/24,440 in the first step.